Some Highlights

- Affordability is based on three key factors: mortgage rates, home prices, and wages.

- And today, it’s improving quickly as rates come down, prices level off, and wages climb.

- If you put your search on pause because it was too expensive to buy, connect with an agent to talk about why now may be the perfect time to jump back in.

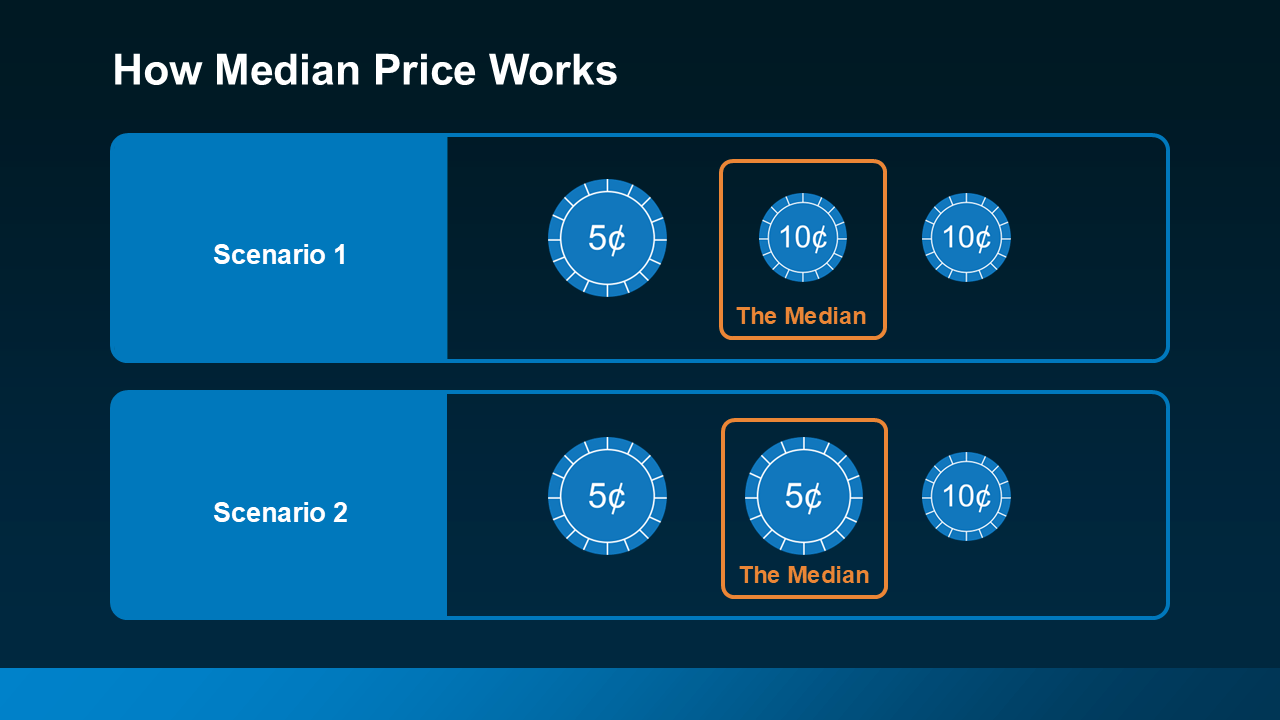

In both cases, a nickel is still worth five cents and a dime is still worth 10 cents. The value of each coin didn’t change. The same is true for housing.

In both cases, a nickel is still worth five cents and a dime is still worth 10 cents. The value of each coin didn’t change. The same is true for housing. As Ralph McLaughlin, Senior Economist at Realtor.com, explains:

As Ralph McLaughlin, Senior Economist at Realtor.com, explains:

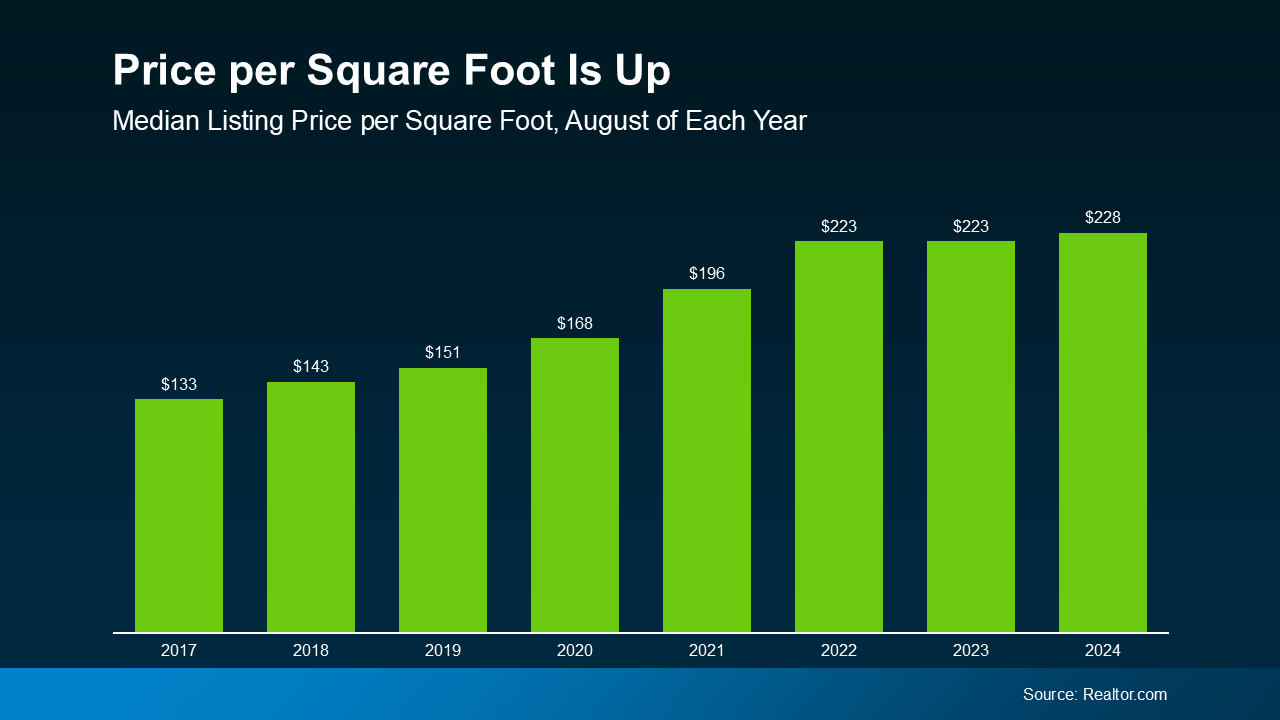

A recent post from Realtor.com notes a similar trend:

A recent post from Realtor.com notes a similar trend:

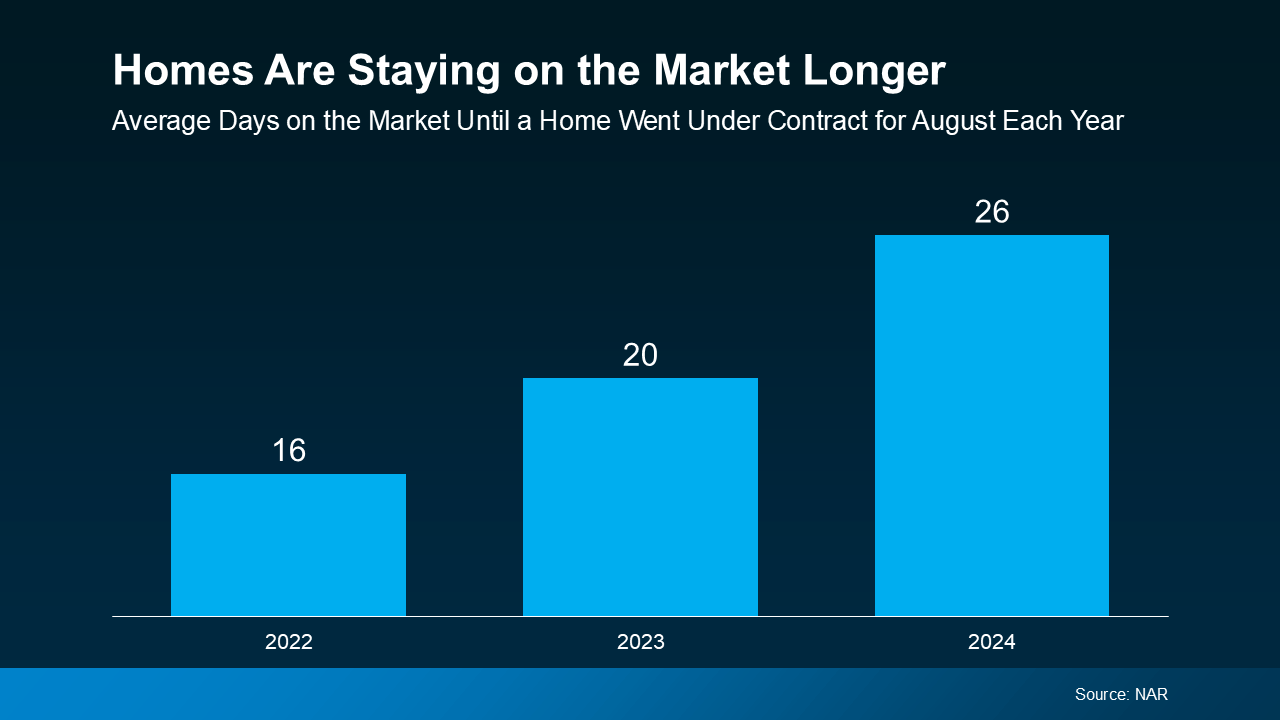

With rates already in the low 6% range, we’re not terribly far off from hitting that threshold. The bottom line is, that when they drop into the 5s, the number of buyers in the market is going to go up – and that means more competition for you.

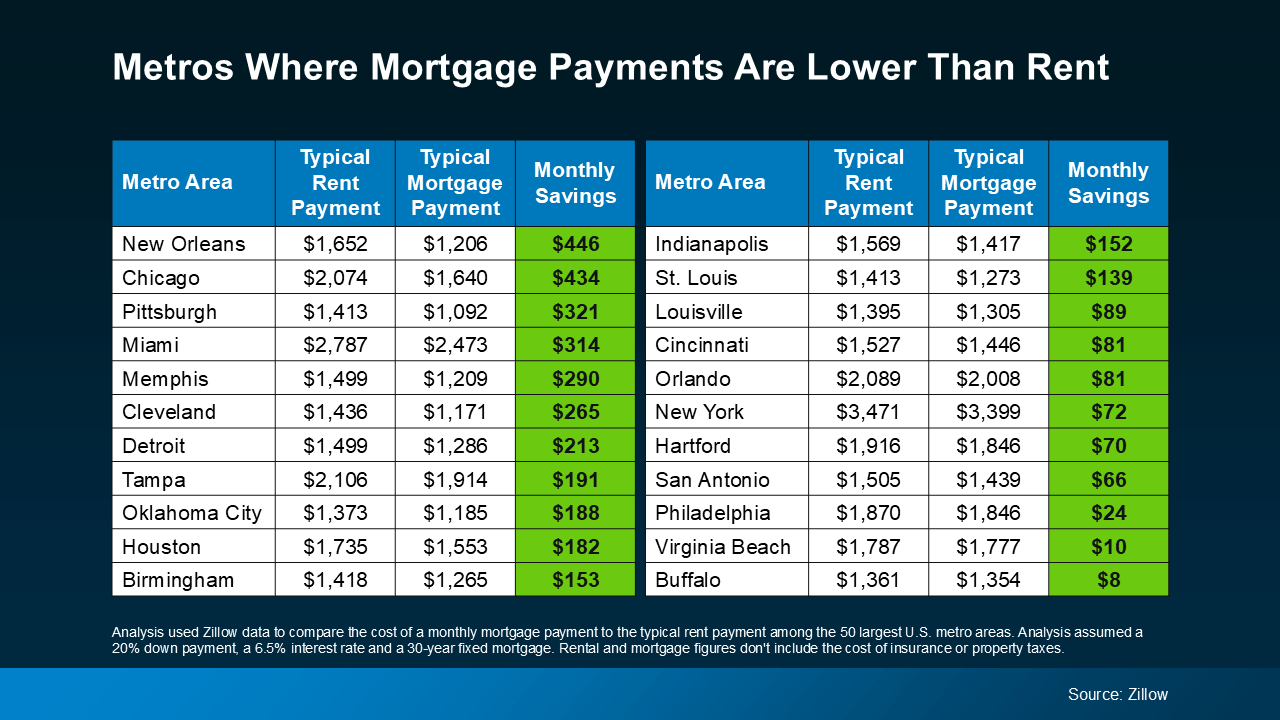

With rates already in the low 6% range, we’re not terribly far off from hitting that threshold. The bottom line is, that when they drop into the 5s, the number of buyers in the market is going to go up – and that means more competition for you. As mortgage rates have eased off their recent peak, home prices have moderated, and inventory has ticked up, affordability has improved significantly. When you add all of that up, it’s getting less expensive to buy a home than to rent one in many parts of the country.

As mortgage rates have eased off their recent peak, home prices have moderated, and inventory has ticked up, affordability has improved significantly. When you add all of that up, it’s getting less expensive to buy a home than to rent one in many parts of the country.

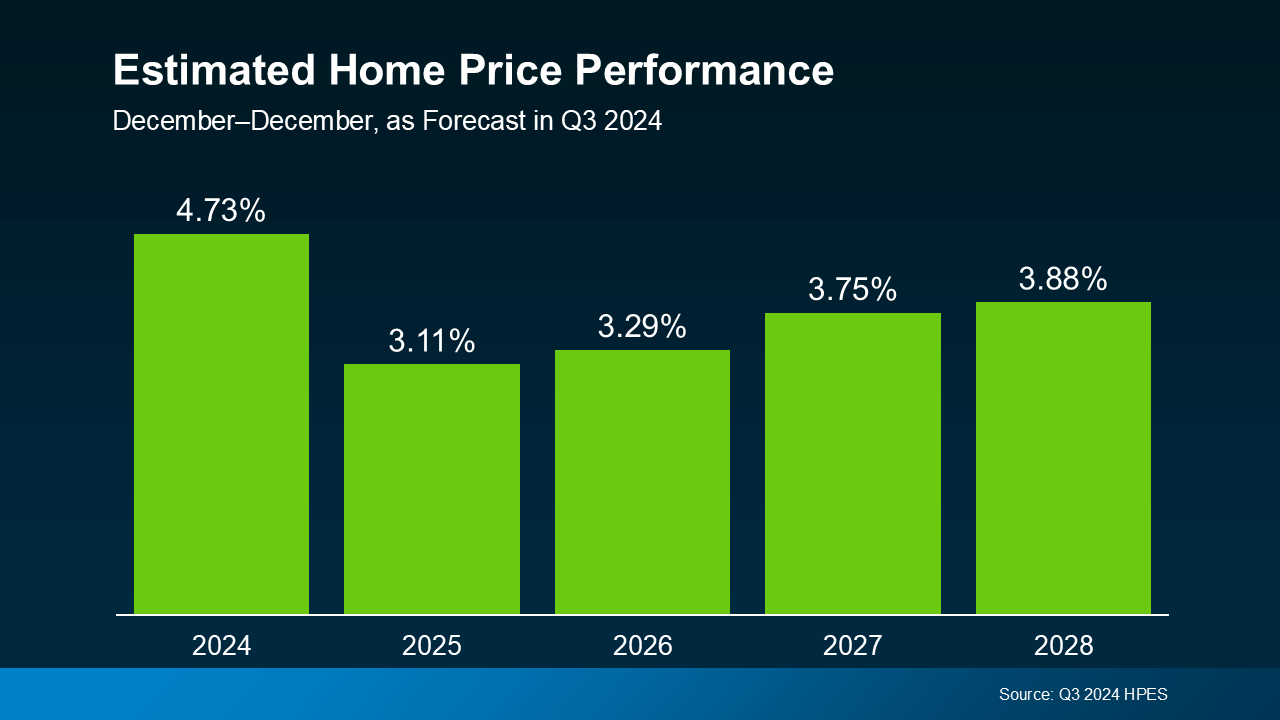

While home prices are going to vary from one local area to the next, this shows they’re expected to keep going up nationally. The size of the increase varies from year-to-year, but the important takeaway is that prices are forecast to rise every single year – just at a moderate pace.

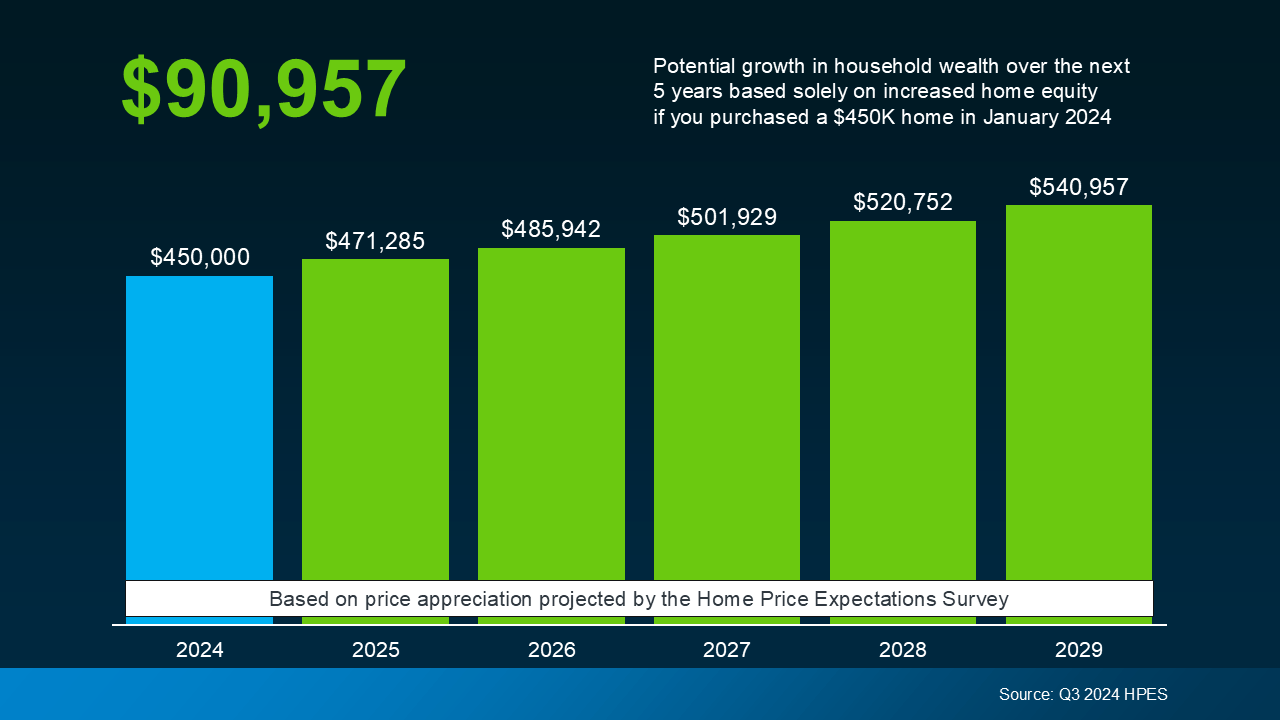

While home prices are going to vary from one local area to the next, this shows they’re expected to keep going up nationally. The size of the increase varies from year-to-year, but the important takeaway is that prices are forecast to rise every single year – just at a moderate pace. If you bought a $450,000 home at the beginning of this year, based on that starting value and the expert forecasts from the HPES, you could gain more than $90,000 in household wealth over the next five years. That’s significant.

If you bought a $450,000 home at the beginning of this year, based on that starting value and the expert forecasts from the HPES, you could gain more than $90,000 in household wealth over the next five years. That’s significant.

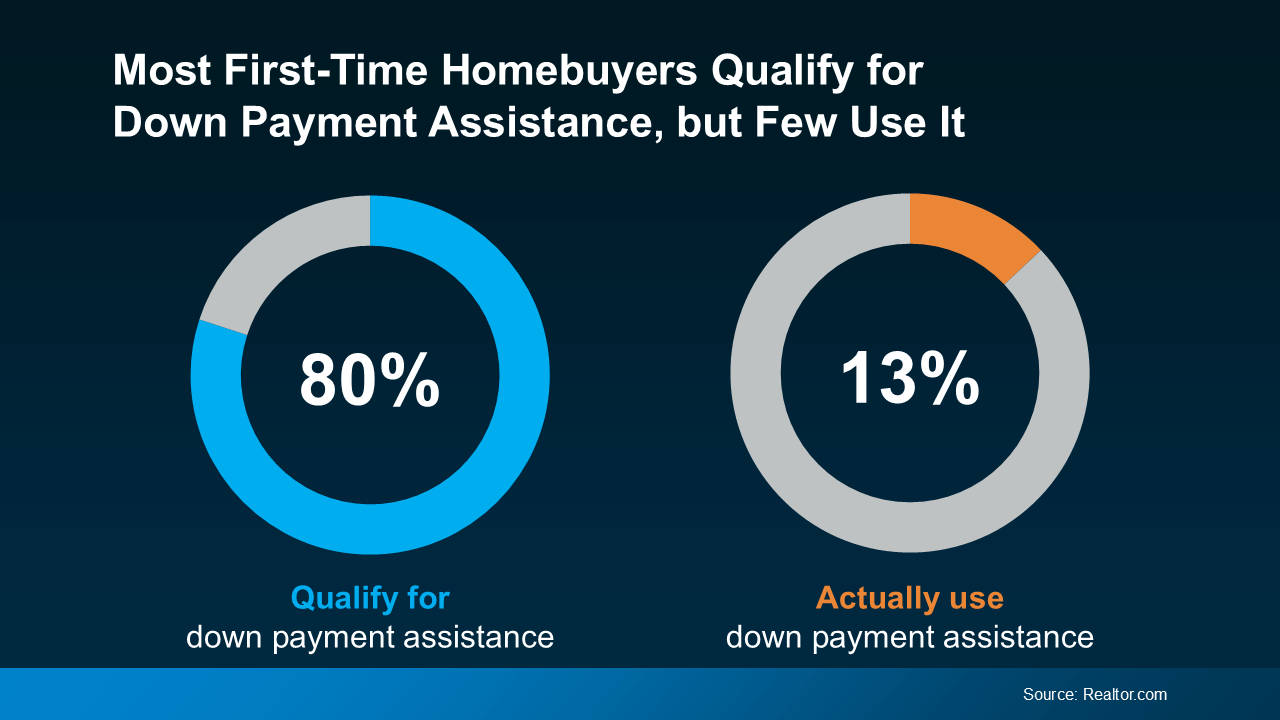

Here’s what you need to know to make the most of your down payment in today’s housing market.

Here’s what you need to know to make the most of your down payment in today’s housing market.