If you’ve thought about buying a home in the past few years, you may have run into two frustrations: asking prices that kept climbing and too few homes to choose from.

In many places, both sticking points are letting up this summer, with lower asking prices and more homes for sale. Let’s look at the trends, and what they mean for your search.

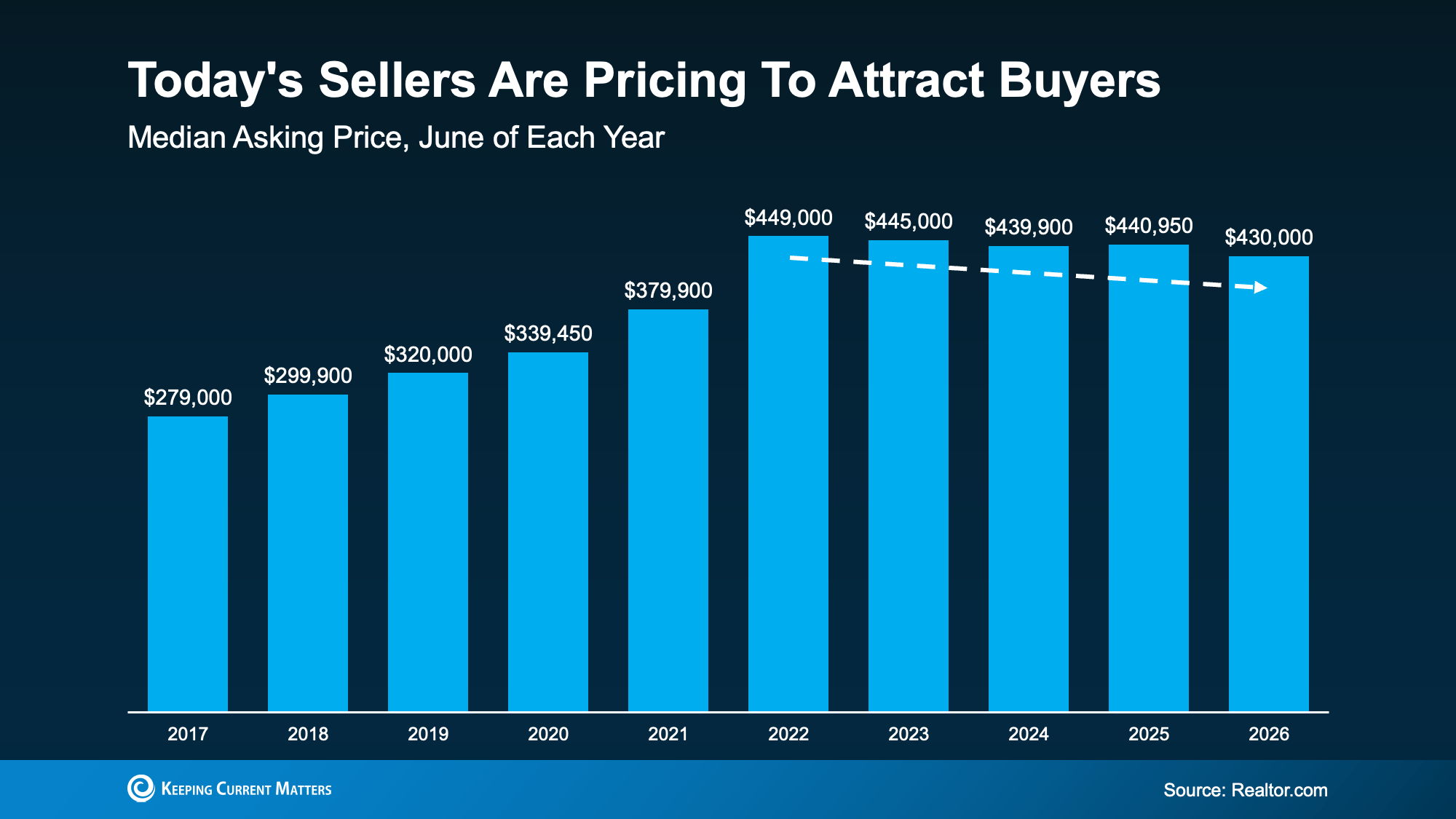

Sellers Are Pricing To Attract Buyers

According to Realtor.com, the national median asking price was $430,000 in June, nearly $11,000 under what it was the year before (see graph below):

That’s the eighth month in a row that the typical asking price has dipped below where they were the previous year, according to the same Realtor.com report.

And while falling prices can sound worrying, this isn’t a sign of an impending crash. We’re talking about asking prices, not sold prices. This is a sign that today’s sellers are meeting the market where it is and pricing to draw buyers. And that’s actually something normal we’d expect from the market. As Danielle Hale, Chief Economist at Realtor.com, puts it:

“Sellers are reading market conditions and are pricing accordingly from the start rather than listing high and cutting later, and buyers are taking note and making bids. This is a welcome sign that we are in a functioning market.”

Asking prices were never going to climb forever – now they're just settling closer to what buyers can actually pay. That signals a healthier market, and sellers re-adjusting their expectations.

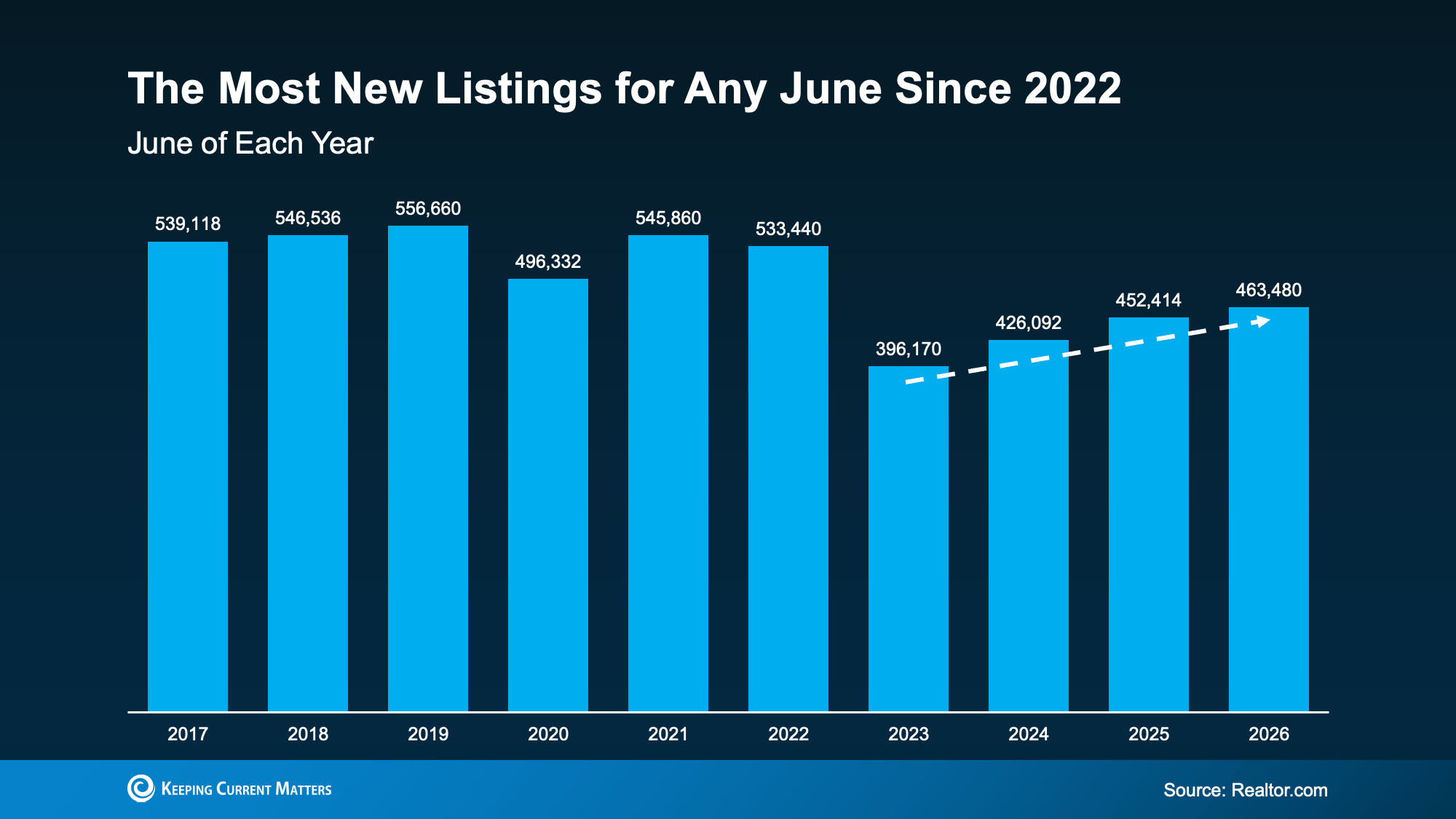

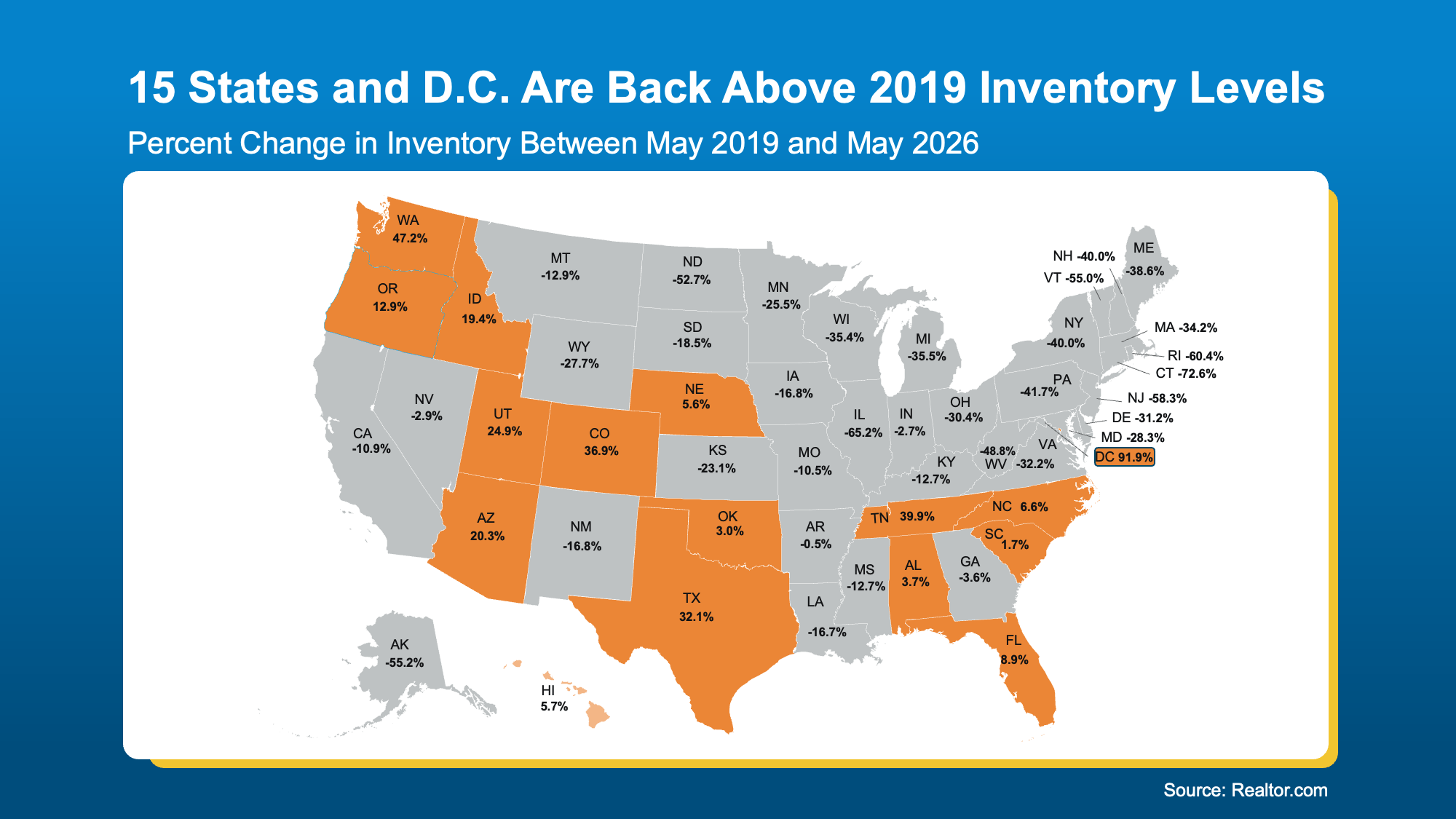

More Homes Are Available Now

If you’ve spent the past few years watching homes disappear before you could even schedule a tour, this is for you.

Supply is starting to catch up. According to Realtor.com, the number of homes listed for sale in June was the highest June number we’ve seen in three years (see graph below):

This means more options for you and less competition for each one.

Now, supply is not back to normal everywhere. As you can see, we’re still down from where we were back in 2017-2019. But in many places, it’s better than it’s been in a while. Here’s how that helps you.

You don’t have to rush an offer just to stay in the running, and you have better odds of finding and landing the right home, not just the one that’s available. Plus, you’ll have more room to negotiate, so you’re searching from a stronger position than buyers had even a year ago.

Why This Is Encouraging if You’re Buying Your First Home

For first-time buyers looking for lower-priced homes, these trends line up especially well. Mischa Fisher, Chief Economist at Zillow, explains:

“The lowest price tiers are exhibiting some softness in terms of price, they also had the most listing-activity growth, the first time since 2022 that’s been the case.”

So, if you’re searching for your first place or your next house, there's a little more to choose from and a little more give on price.

Bottom Line

If a tight budget or a thin selection has kept you from buying a home, now might be the time to restart your search.

Connect with a local real estate agent to see what's available where you're looking.

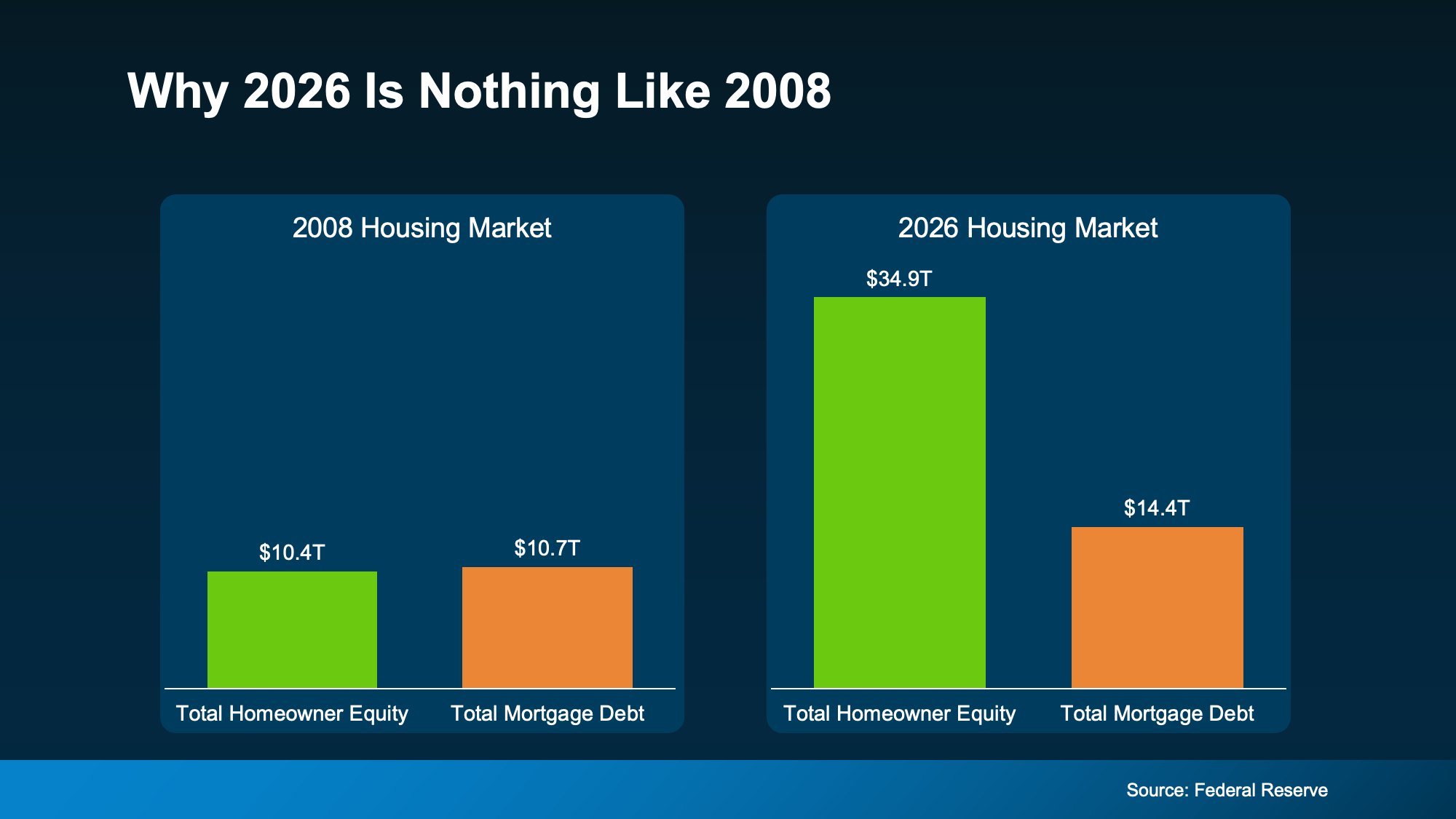

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time.

That gap means most homeowners aren’t stretched thin or one bad month away from trouble. They own a meaningful chunk of their home and that gives them options. If they needed to sell, many could because they have a cushion. And that cushion grows over time. That's a big reason inventory stays tight. Those homeowners aren't in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling.

That's a big reason inventory stays tight. Those homeowners aren't in a rush to trade their rate for a higher one. They’re sitting comfortably in a strong financial position, not scrambling. That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

That slowdown is good news, as Daryl Fairweather, Chief Economist at Redfin, explains:

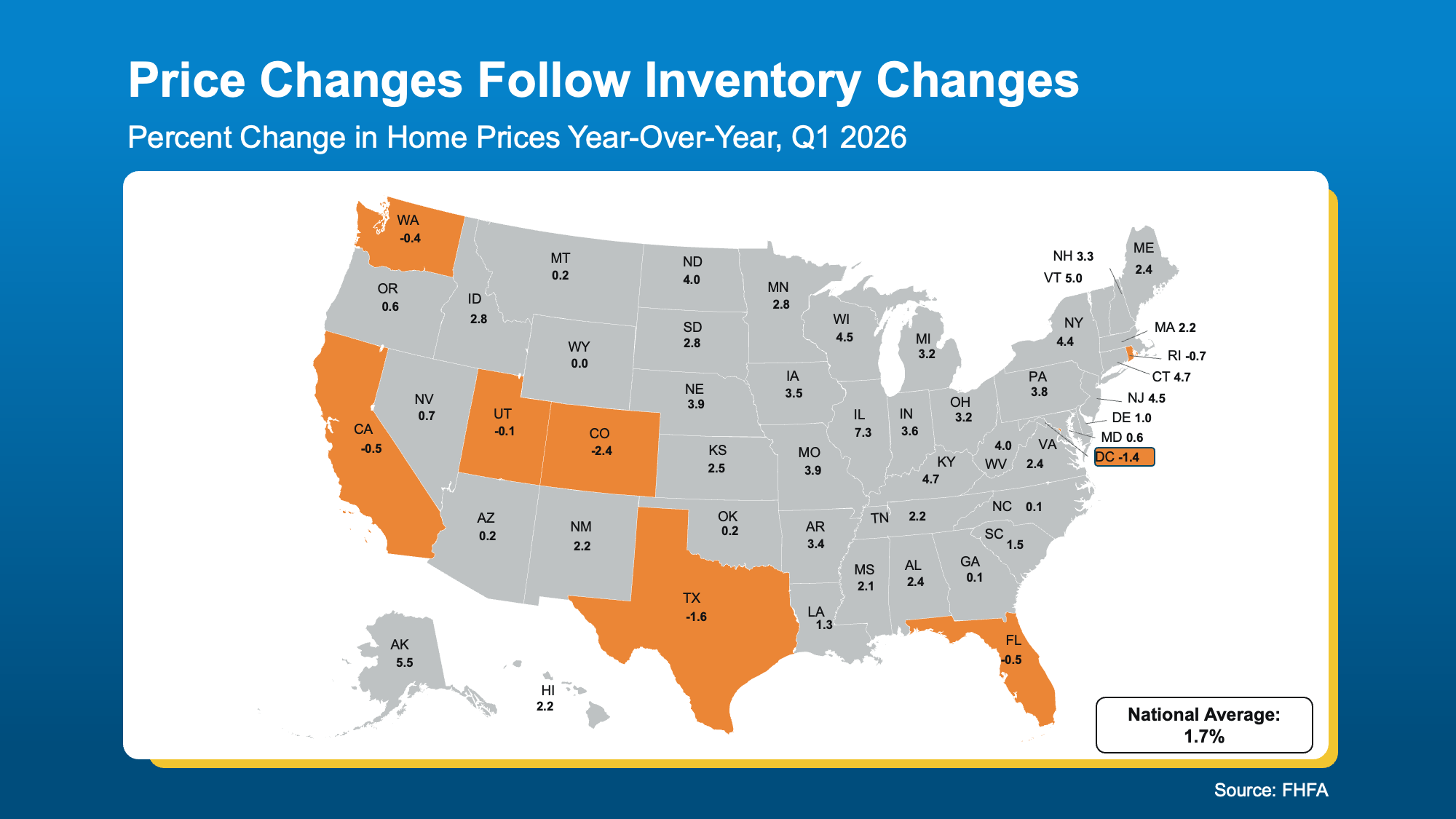

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what's happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).

Now, let’s look at the latest Federal Housing Finance Agency (FHFA) data to see what's happened to home prices in those same states over the past year (again, you’ll want to focus on the orange in the next map).