Whether it’s at a family gathering, your company party, or catching up with friends over the holidays, the housing market always finds its way into the conversation.

Here are the top three questions on a lot of people’s minds this season, and straightforward answers to help you feel more confident about the market.

1. “Will I even be able to find a home if I want to move?”

Yes, more than you could a year or two ago.

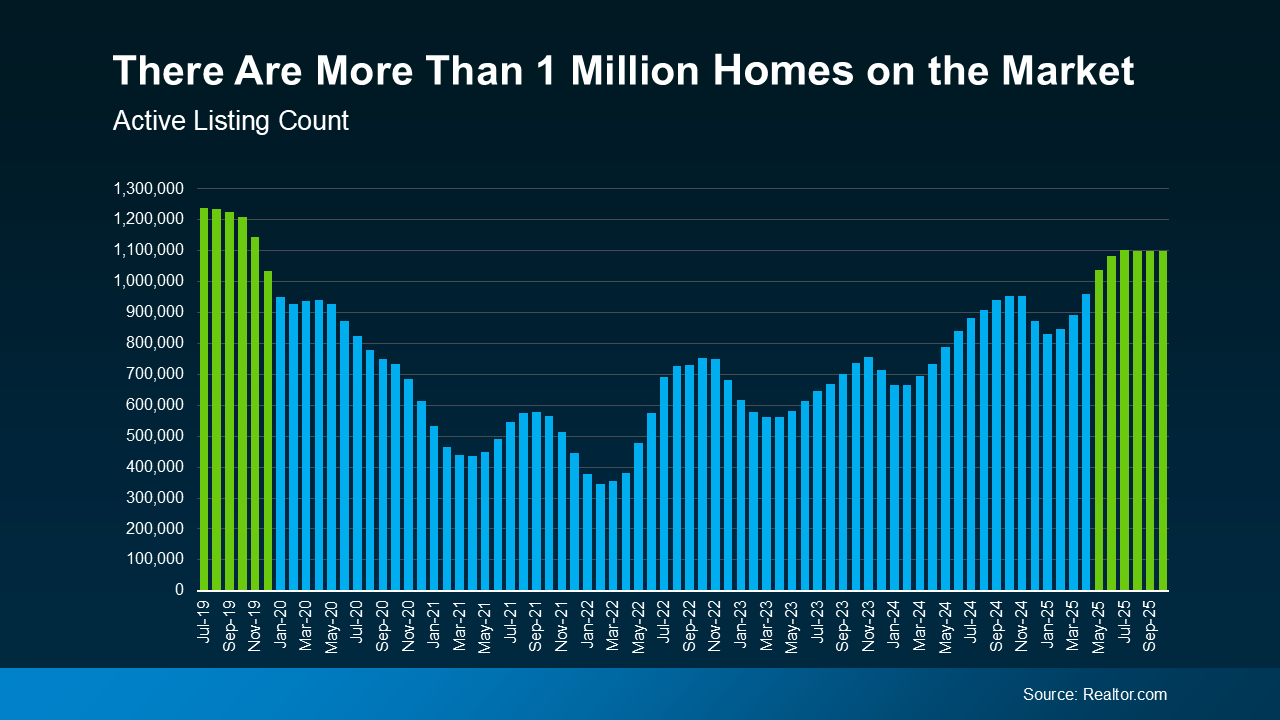

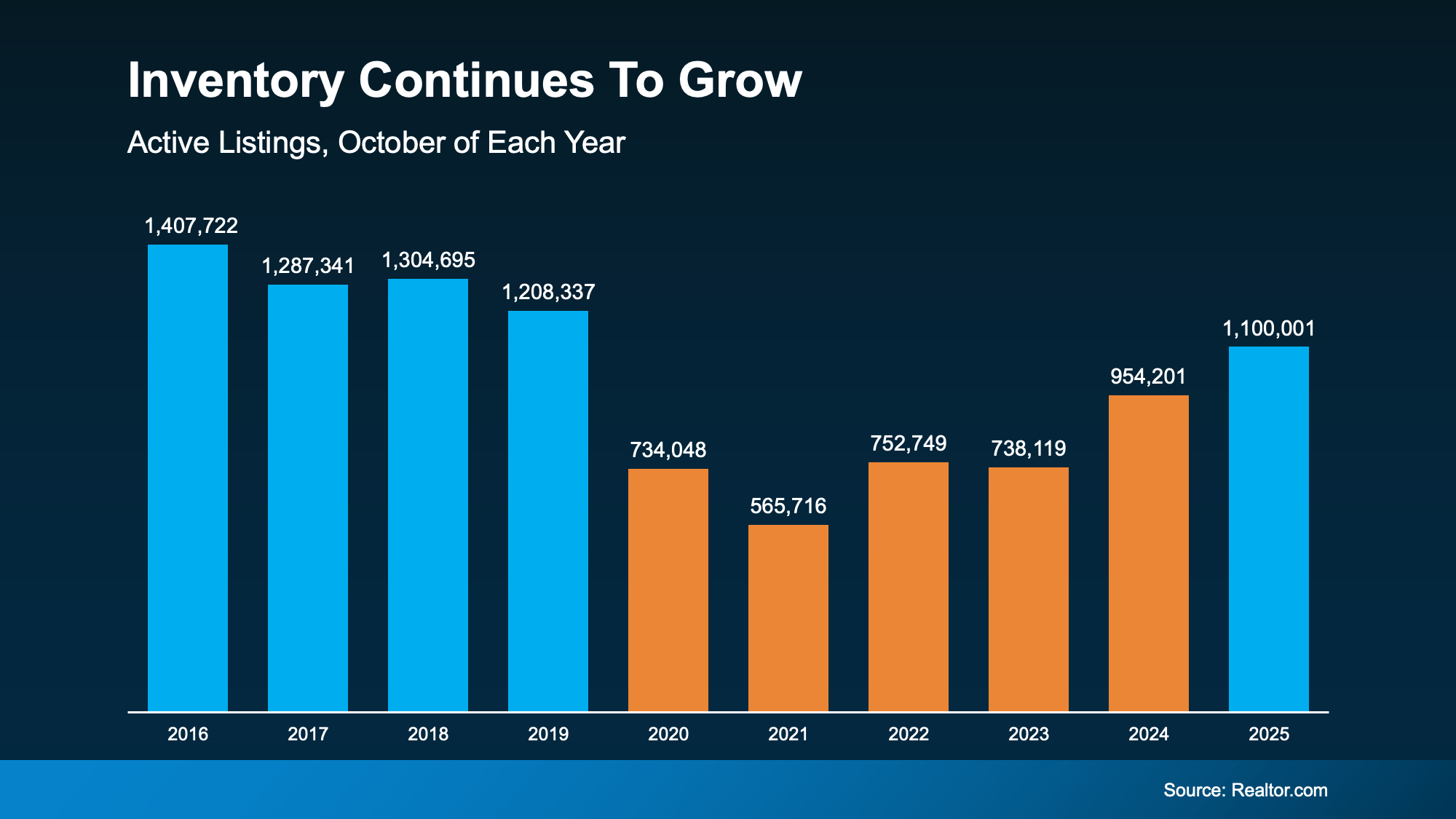

The number of homes for sale has been rising over the past few years. According to data from Realtor.com, there have been more than one million homes on the market for six straight months, something that hasn’t happened since 2019 (see graph below):

That means two things:

That means two things:

- Buyers have more options.

- Sellers have more places they can move to next.

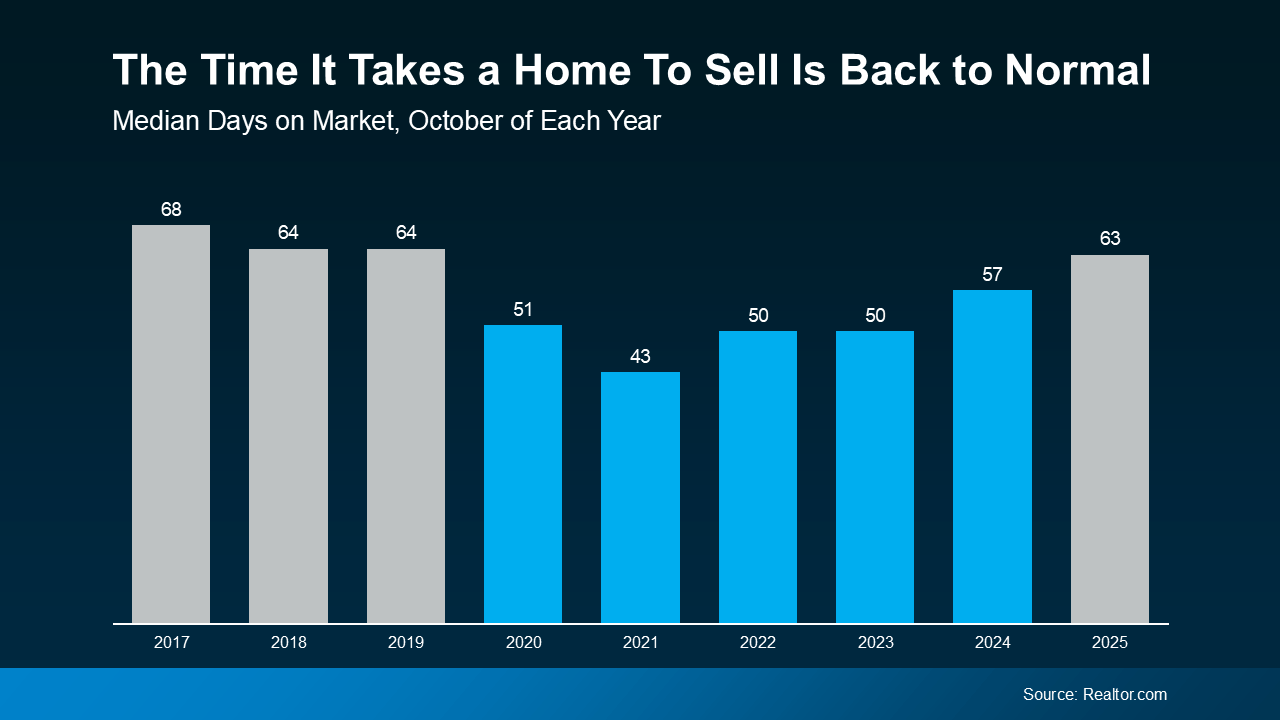

Many homeowners who held off are realizing the shelves aren’t bare anymore. So, if you hit pause on your home search last year because nothing fit your needs, it may be worth another look. With more homes on the market now, you’re not competing for the same handful of listings like you were a couple of years ago.

And because there’s a bit more to choose from, homes aren’t disappearing the minute they hit the market. That gives buyers more space to breathe, more options to compare, and a little more time to make a confident decision.

2. “Will I ever be able to afford a house?”

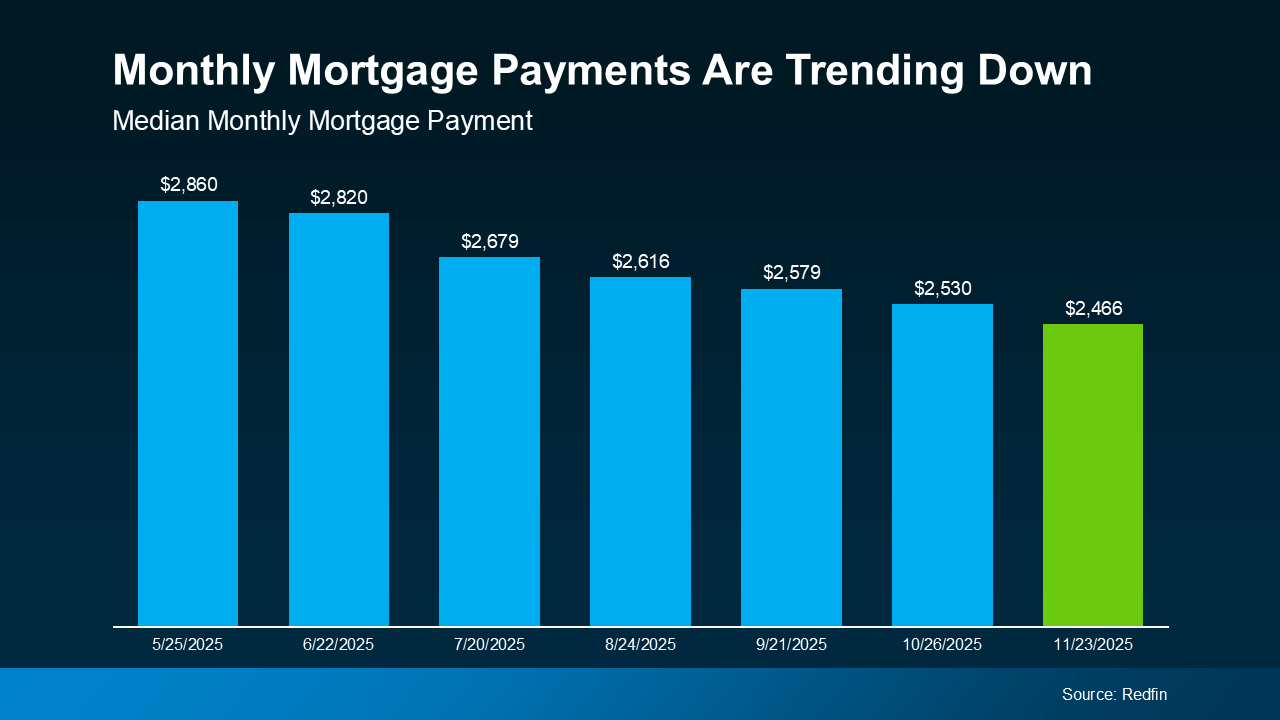

Affordability is starting to improve. Finally.

It’s been a tough few years for buyers. But this year brought some much-needed good news:

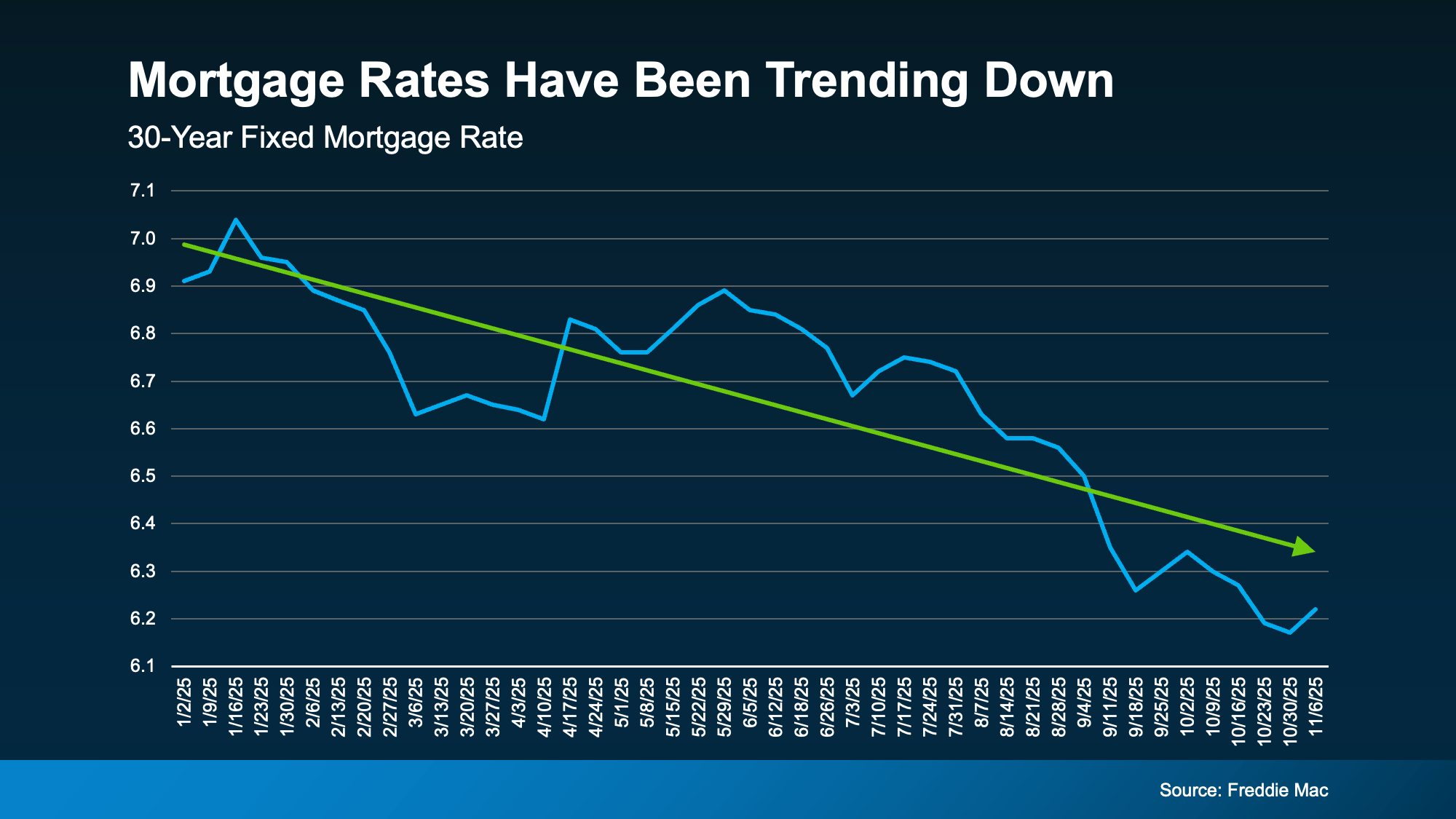

- Mortgage rates have been easing.

- Home price growth has been moderating.

That adds up to a monthly mortgage payment that’s hundreds of dollars lower than it would have been just a few months ago (see graph below):

Buying still isn’t easy, but the numbers are starting to improve. For a lot of people, that means buying a home is becoming a more realistic goal again.

Buying still isn’t easy, but the numbers are starting to improve. For a lot of people, that means buying a home is becoming a more realistic goal again.

3. “Should I wait for prices to come down?”

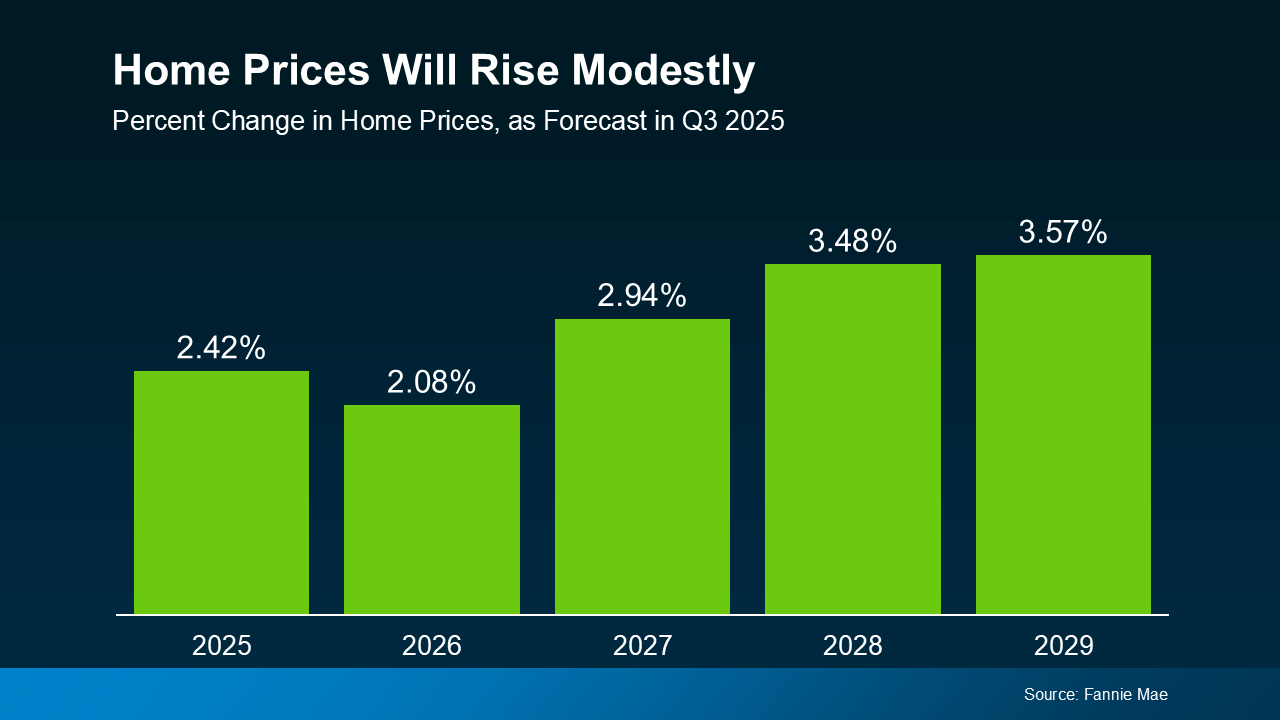

A lot of people worry that the housing market is about to crash, but the data doesn’t point in that direction. Yes, the number of homes for sale has been rising, but it’s still nowhere near the level needed for prices to fall significantly on a national scale. On top of that, homeowners today have a lot of equity and are in a much stronger financial position than they were back in 2008.

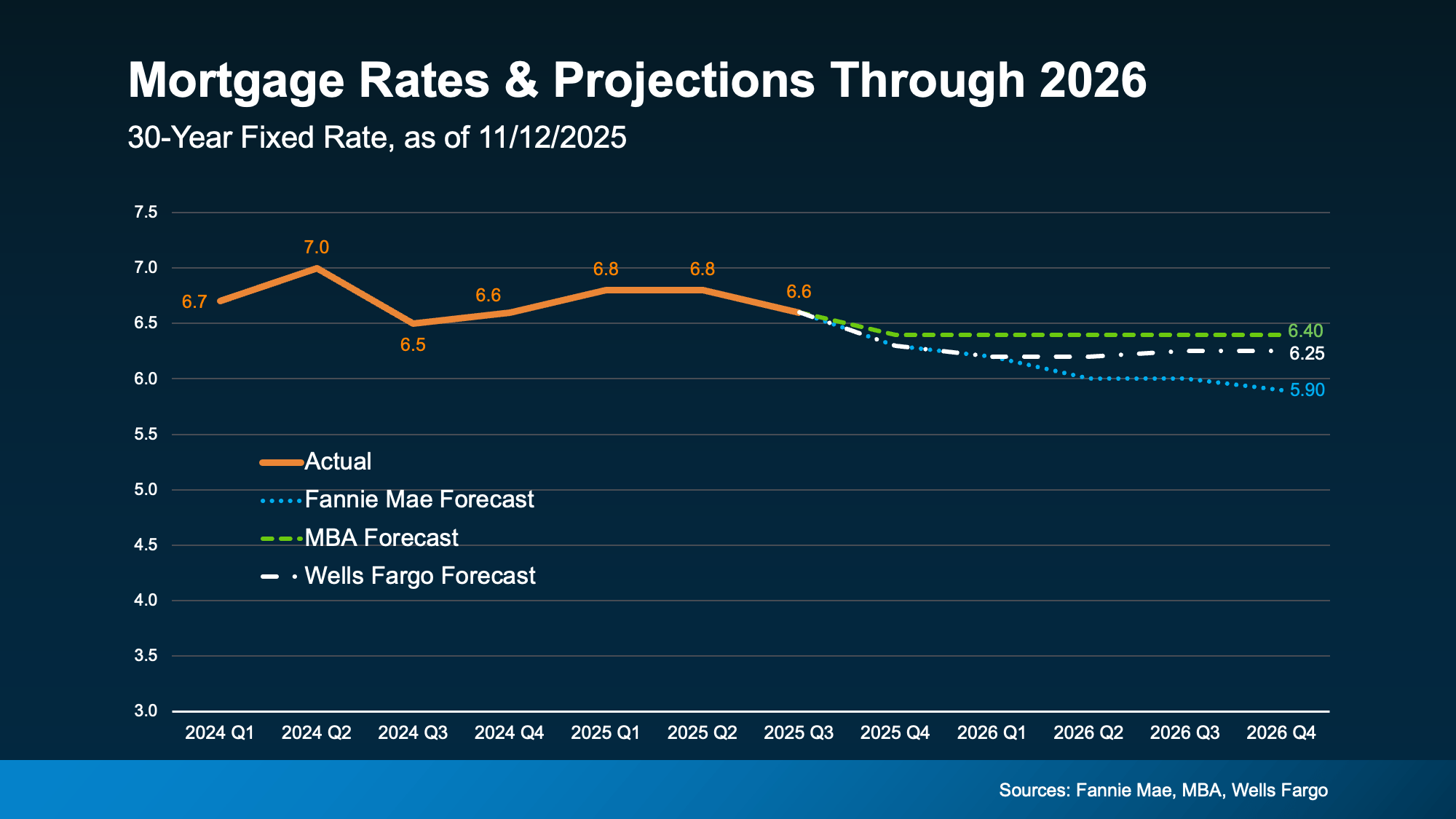

Of course, every local market is a little different. Some areas are still seeing prices climb, while others that saw huge spikes a few years ago are leveling off or seeing small corrections. But overall, the national picture is clear: experts surveyed by Fannie Mae project home prices will keep rising, just at a slower, more normal pace (see graph below):

That’s why waiting for a major price drop to get a deal isn’t a very strategic plan. History shows the same thing over and over: people who spend time in the market tend to build the most long-term wealth, not the people who try to time the market perfectly.

That’s why waiting for a major price drop to get a deal isn’t a very strategic plan. History shows the same thing over and over: people who spend time in the market tend to build the most long-term wealth, not the people who try to time the market perfectly.

Bottom Line

Talk about the housing market can feel loud and confusing, especially when you’re hearing so many different takes. A trusted local agent can help you make sense of the data and understand your options. If you’re thinking about buying or selling, reach out to a local professional.

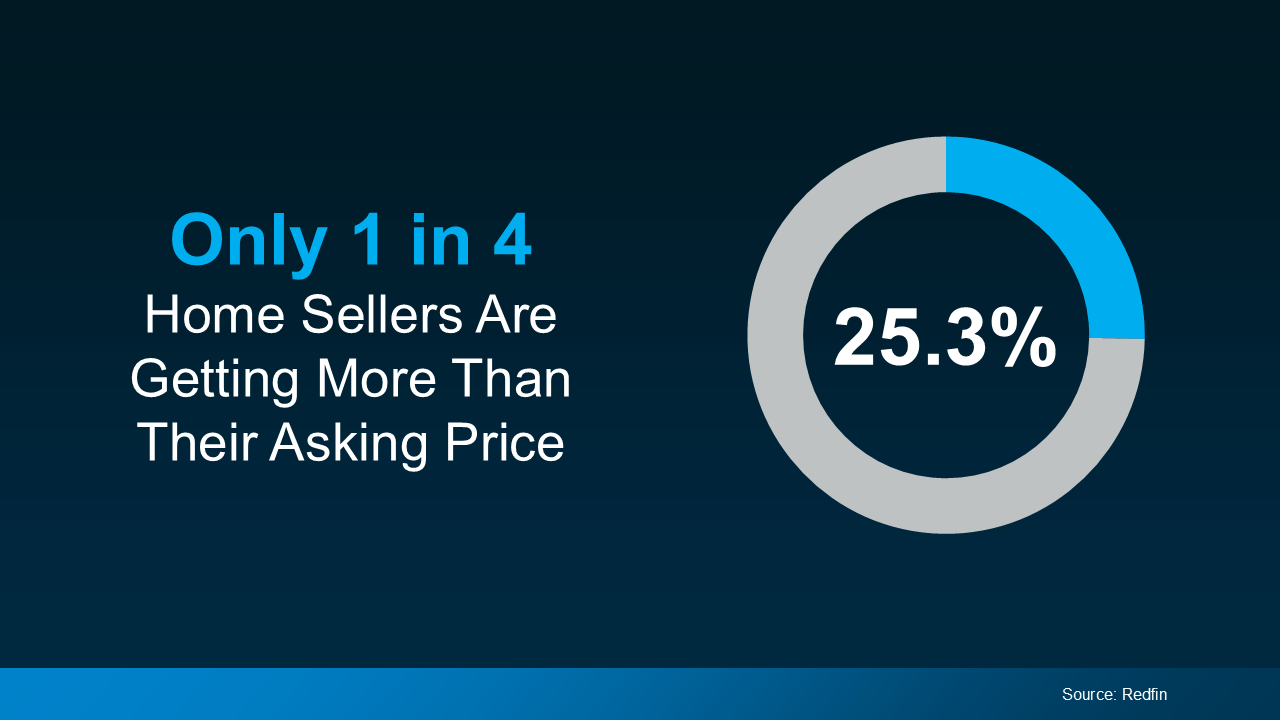

So, if you’re serious about getting as much as you can for your money, focusing on these listings could be your best strategy yet.

So, if you’re serious about getting as much as you can for your money, focusing on these listings could be your best strategy yet. Zillow sums it up best:

Zillow sums it up best:

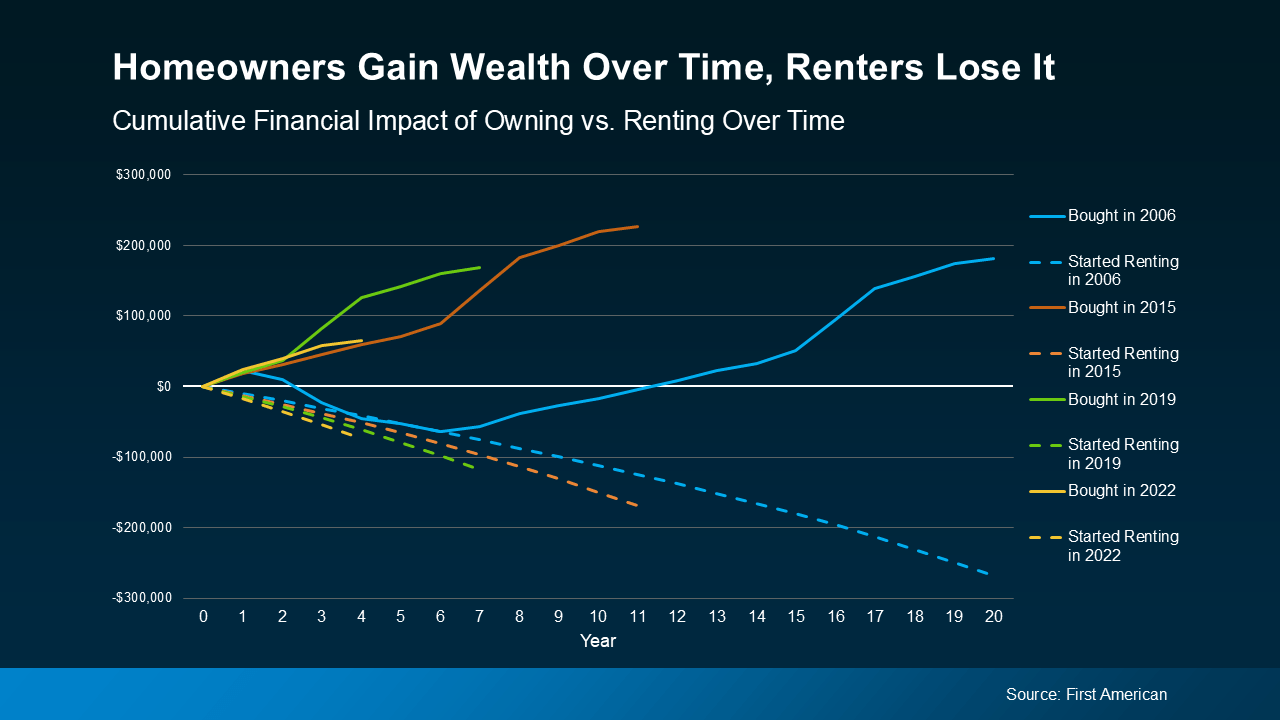

For some, that meant trading an apartment for their very first house – a home they can finally make their own, where they can paint the walls, plant the garden, and build a future.

For some, that meant trading an apartment for their very first house – a home they can finally make their own, where they can paint the walls, plant the garden, and build a future.

The takeaway is simple: time in a home builds wealth. Time renting doesn’t.

The takeaway is simple: time in a home builds wealth. Time renting doesn’t.

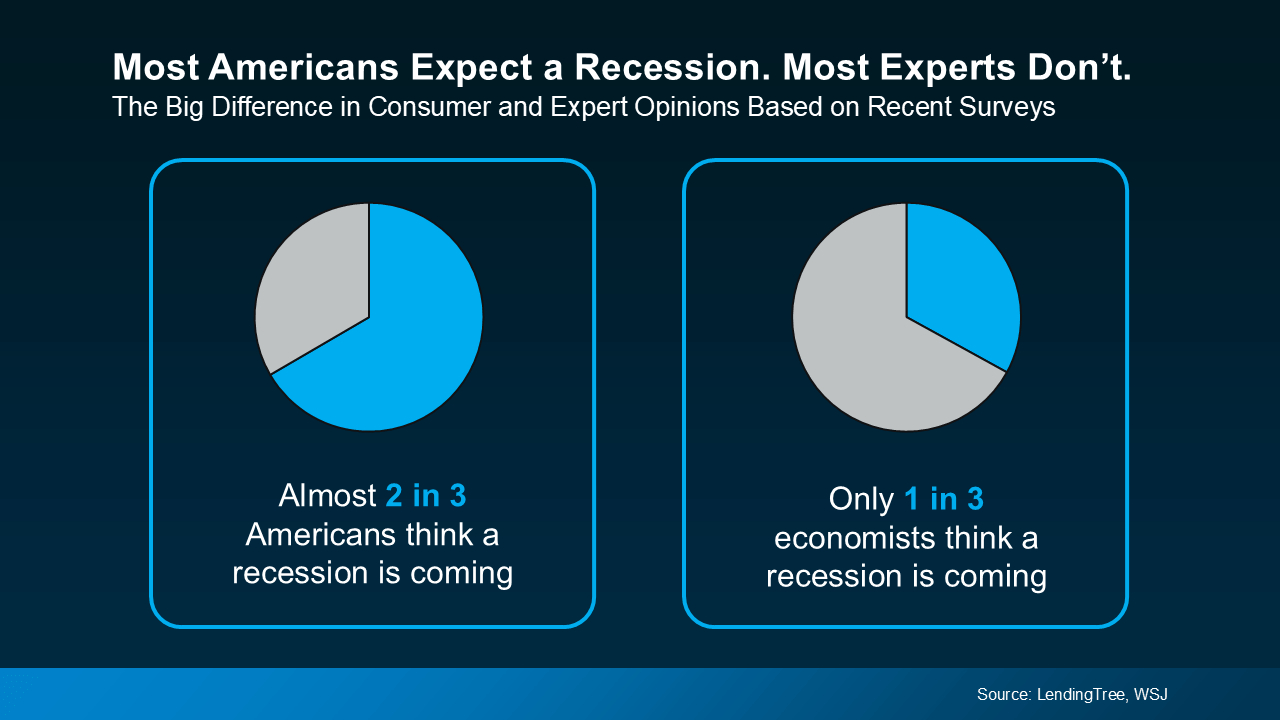

If the expert economists aren’t super worried, should you be? We’re not in a recession right now. And there’s no guarantee we’re heading into one.

If the expert economists aren’t super worried, should you be? We’re not in a recession right now. And there’s no guarantee we’re heading into one.

And here’s where the mismatch is coming from.

And here’s where the mismatch is coming from. It just feels slower because they’re comparing it to the lightning-fast pace of 2020 and 2021.

It just feels slower because they’re comparing it to the lightning-fast pace of 2020 and 2021.

And in just the last few months, we’ve seen the best rates of 2025. According to Sam Khater, Chief Economist at Freddie Mac:

And in just the last few months, we’ve seen the best rates of 2025. According to Sam Khater, Chief Economist at Freddie Mac: That return to more normal inventory levels is a really good thing. It gives buyers more options than they’ve had in years. And it’s helping to bring the market closer to balance.

That return to more normal inventory levels is a really good thing. It gives buyers more options than they’ve had in years. And it’s helping to bring the market closer to balance. And experts think this momentum will continue. Economists from Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR) all forecast moderate sales growth going into 2026.

And experts think this momentum will continue. Economists from Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR) all forecast moderate sales growth going into 2026.

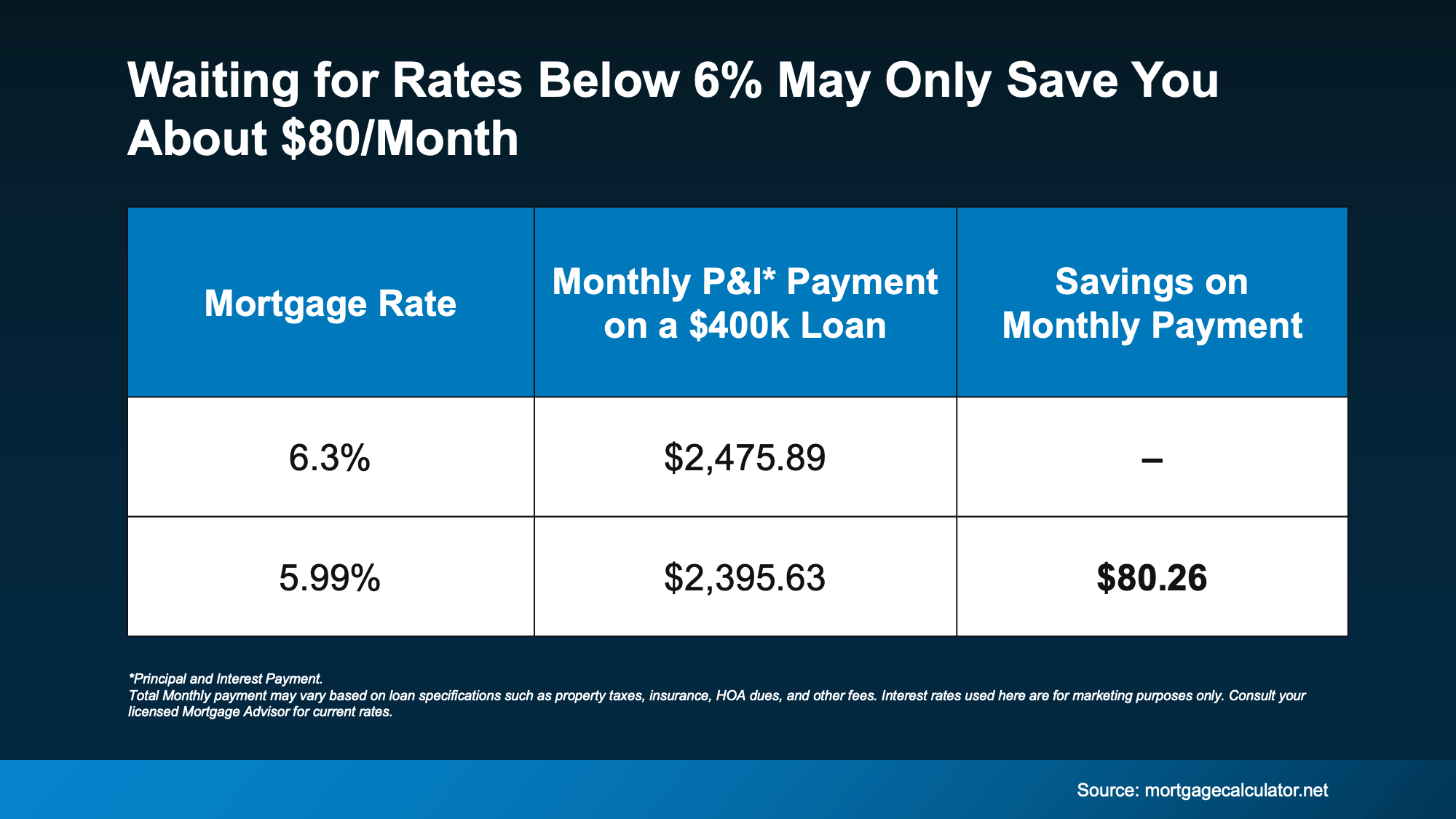

And even if rates do dip below 6%, the extra savings you’re holding out for won’t move the needle as much as you might expect.

And even if rates do dip below 6%, the extra savings you’re holding out for won’t move the needle as much as you might expect. Eighty dollars. That’s it. And for the typical family, that’s about one dinner out (or one dinner in, if you have it delivered). That’s not enough to change the game for most buyers. But the savings of nearly $400 we already have compared to when you paused your search in the spring? That might be.

Eighty dollars. That’s it. And for the typical family, that’s about one dinner out (or one dinner in, if you have it delivered). That’s not enough to change the game for most buyers. But the savings of nearly $400 we already have compared to when you paused your search in the spring? That might be.

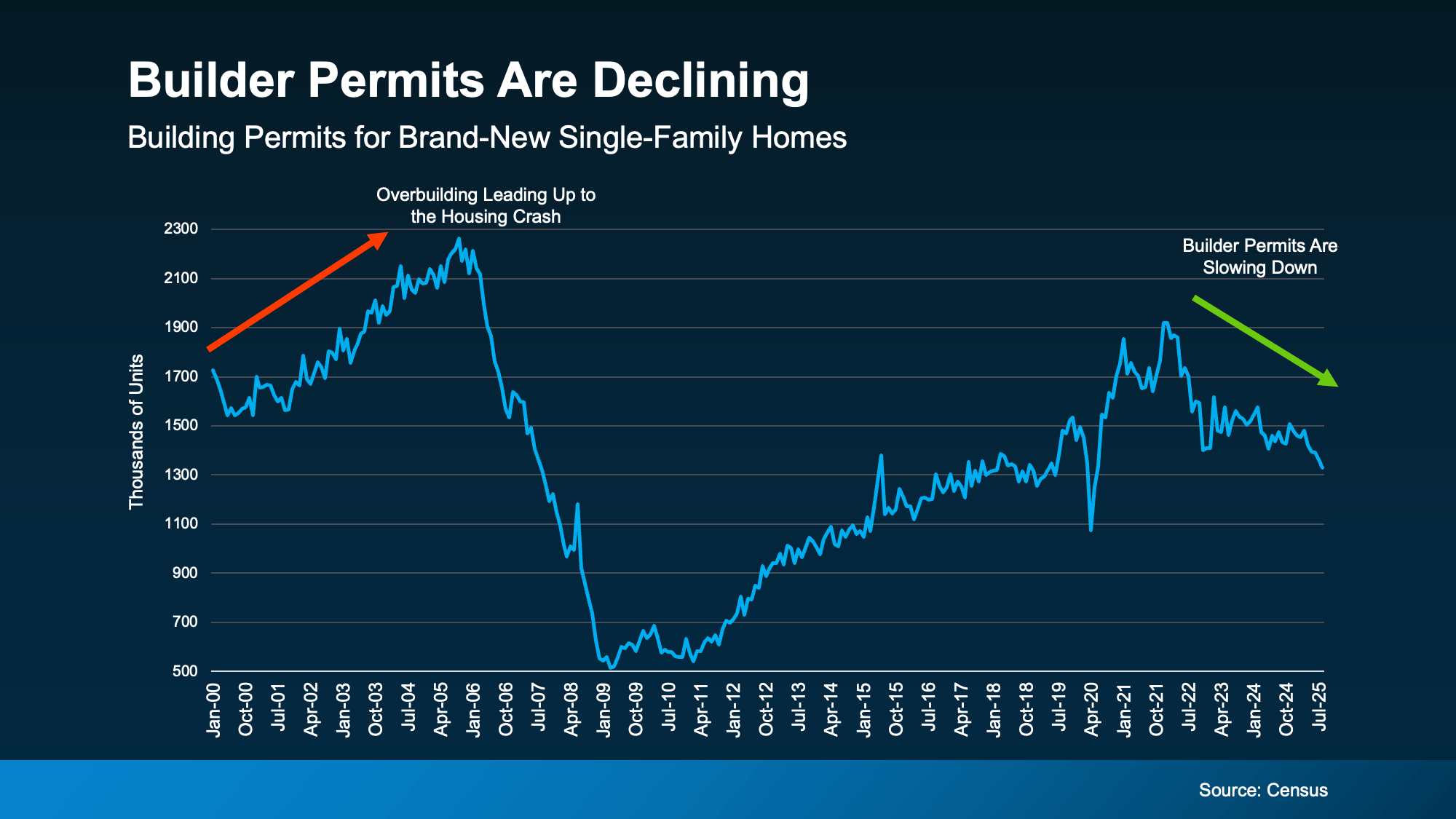

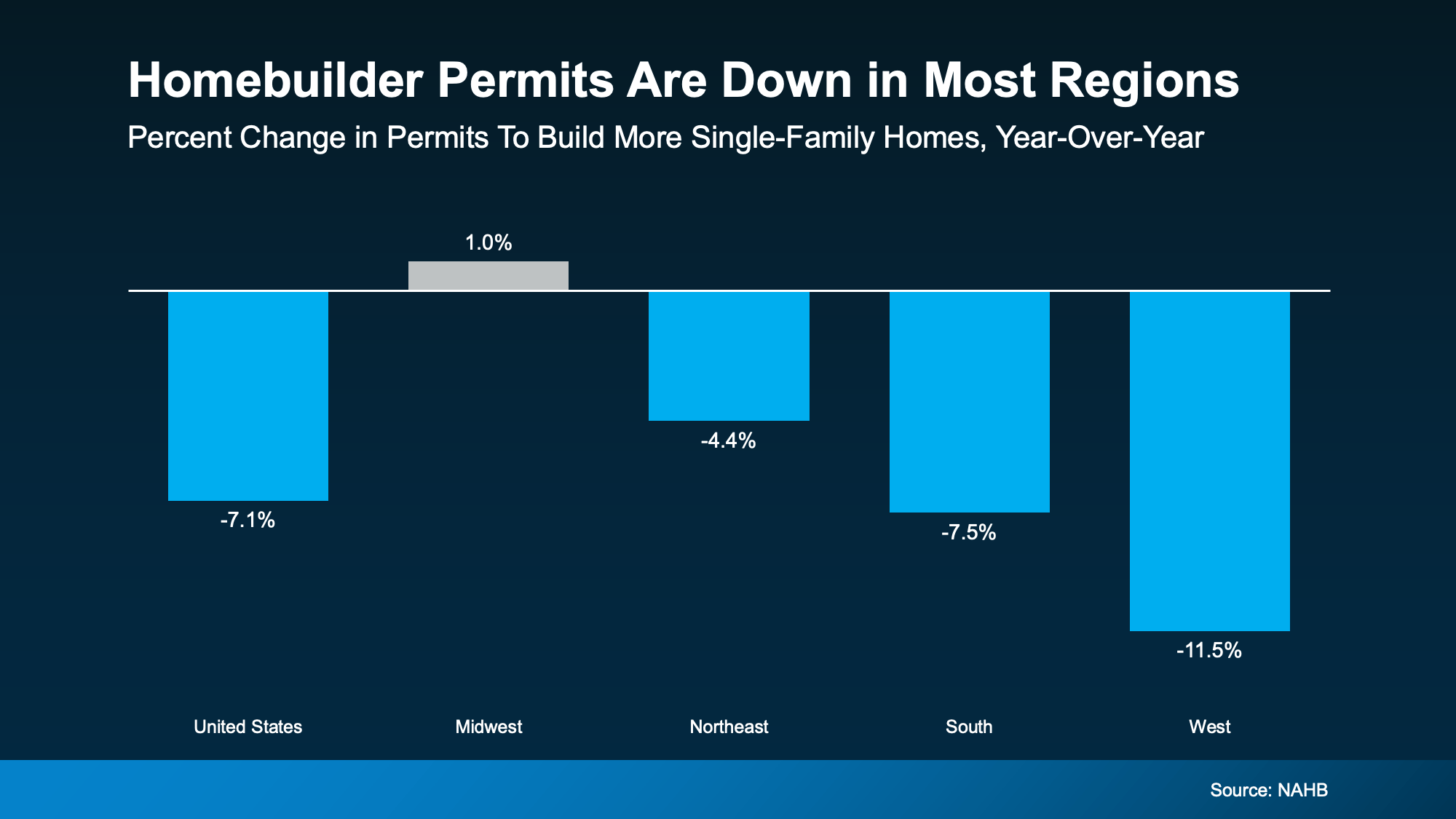

New data from the National Association of Home Builders (NAHB) confirms that trend. It shows that single-family building permits have fallen for eight straight months.

New data from the National Association of Home Builders (NAHB) confirms that trend. It shows that single-family building permits have fallen for eight straight months. NAHB reports single-family permits are down in nearly every part of the country, with just one region showing a slight uptick. And even there, the growth is so small, it’s practically flat.

NAHB reports single-family permits are down in nearly every part of the country, with just one region showing a slight uptick. And even there, the growth is so small, it’s practically flat.