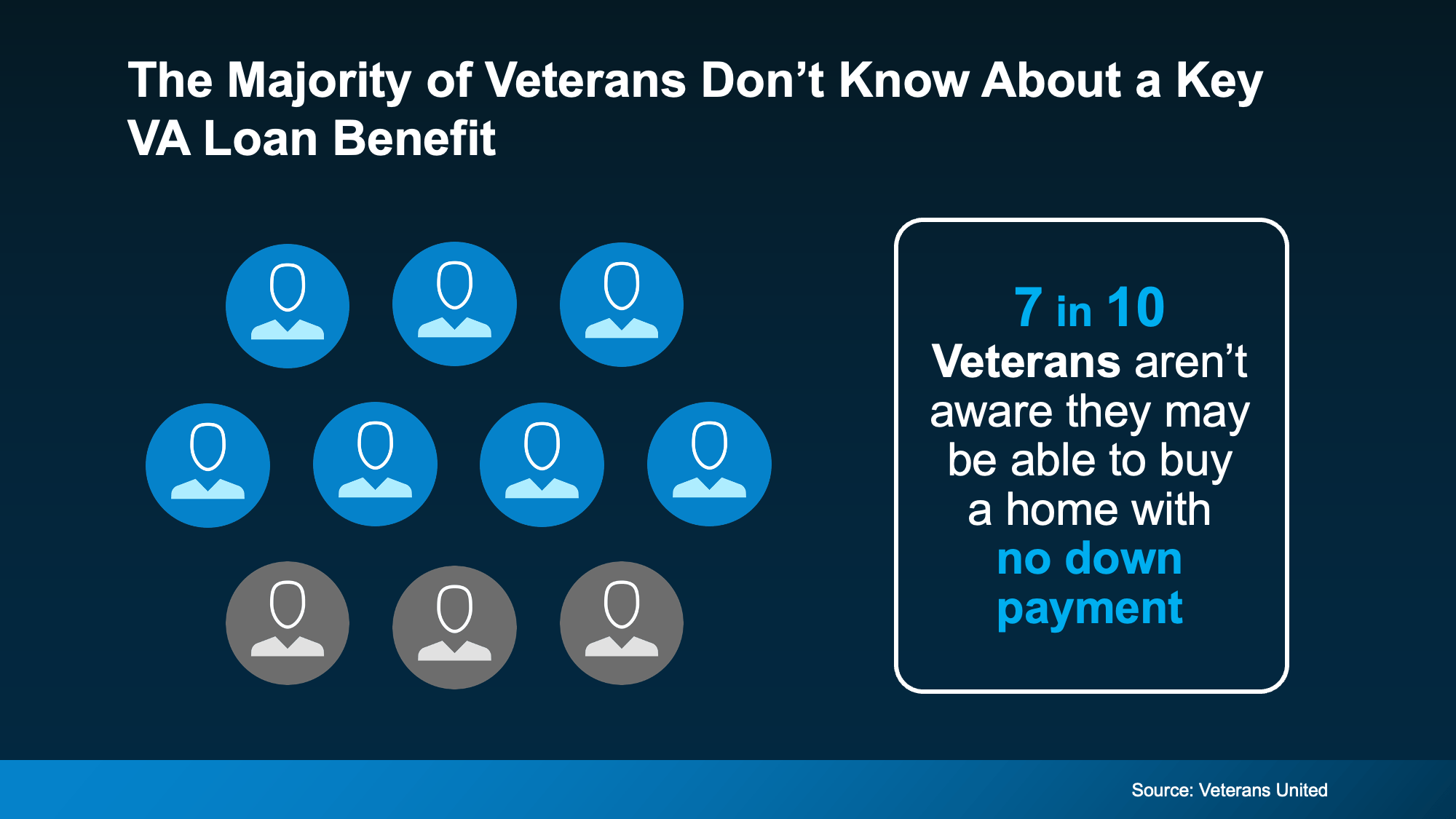

If you’ve served in the military (or if your spouse has), you have access to one of the most powerful homebuying tools out there. The chance to buy a home without having a down payment.

Unfortunately, 70% of Veterans (that's 7 out of every 10) don’t know about this benefit, according to Veterans United.

And that’s a big missed opportunity for those who’ve earned this benefit through service. So, let’s break down what you really need to know about Veterans Affairs (VA) home loans right now.

And that’s a big missed opportunity for those who’ve earned this benefit through service. So, let’s break down what you really need to know about Veterans Affairs (VA) home loans right now.

Why VA Home Loans Can Be a Great Option

For nearly 80 years, VA loans have made homeownership possible for millions of Veterans and active-duty service members. Here are just a few of the top perks according to the Department of Veteran Affairs:

- Options for $0 Down Payment: Many Veterans can buy a home without spending years saving up.

- Fewer Upfront Costs: The VA limits which types of closing costs Veterans have to pay, helping you keep more cash on hand when you’re finalizing your purchase.

- No Private Mortgage Insurance (PMI): Unlike many other loan types, VA loans don’t require PMI, lowering your monthly costs.

These features make VA loans a great way for service members (or their family) to build stability, save money, and start creating long-term wealth through homeownership.

Can You Still Get a VA Loan with the Government Shutdown?

But lately, there’s been some confusion about whether VA loans are still available due to the government shutdown. And that uncertainty has kept some Veterans from taking the next step.

While there may be processing delays, Veterans United explains you can still get a loan:

“There’s been a lot of confusion and uncertainty about how a government shutdown will affect VA home loans . . . The good news is that the shutdown has minimal impacts on VA lending. Lenders are still able to order appraisals, obtain a borrower’s Certificate of Eligibility, submit the VA Funding Fee and more. In short, Veterans are still able to use their home loan benefit to buy a home or refinance an existing mortgage.”

So, despite the headlines, you can still use your VA home loan benefits today. The process is ready when you are. It just may take more time to go through.

Why the Right Agent and Lender Matter

Just remember, using your VA home loan is easier (and smoother) when you have the right team behind you. As VA News puts it:

“Choosing a military-friendly broker or agent who understands the VA home loan application process can make all the difference in the homebuying experience. Finding the right agency or brokerage is just as important as locking in a good VA mortgage lender. Communication is key to getting to the loan closing table.”

A knowledgeable agent and an experienced lender can help you navigate every step, all the way from qualifying to closing. With their help, you can make sure you’re getting the most out of your benefits.

Bottom Line

If you’re a Veteran, a VA home loan is one of the most valuable benefits you’ve earned through your service. It offers options for no down payment, limited closing costs, and more.

Want to learn more? Talk to a lender so you can take full advantage of the benefits you’ve earned.

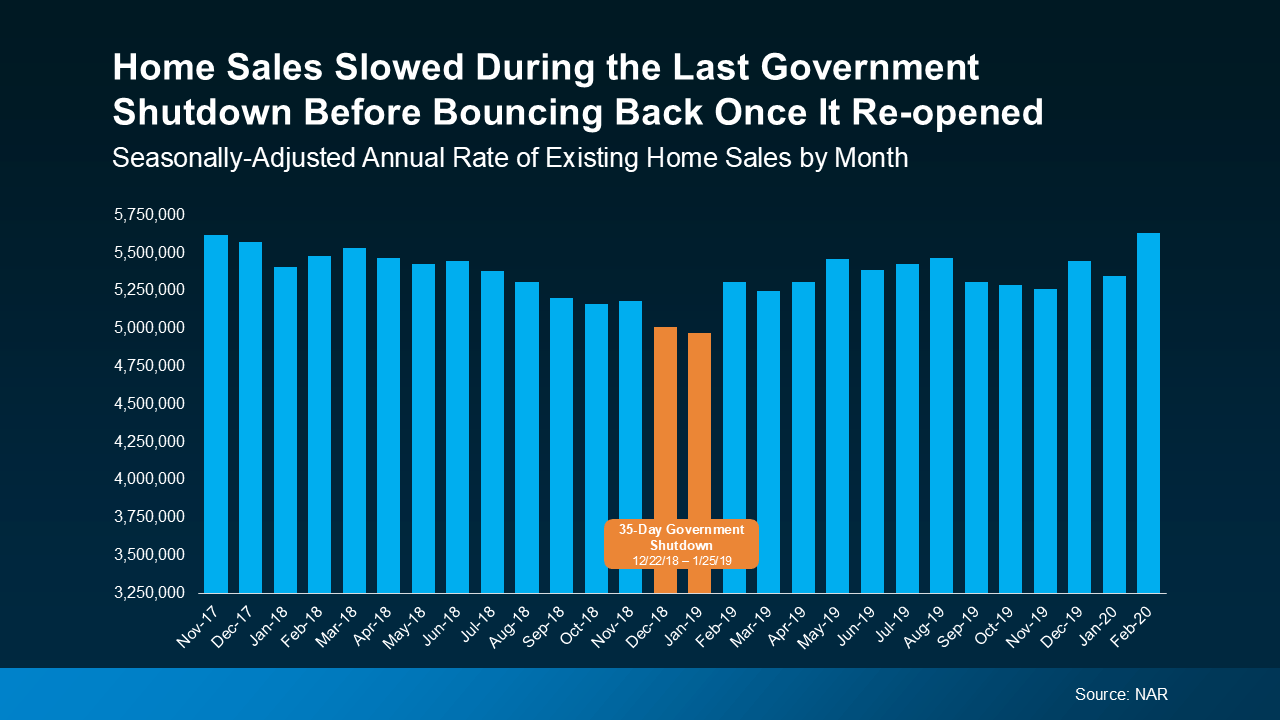

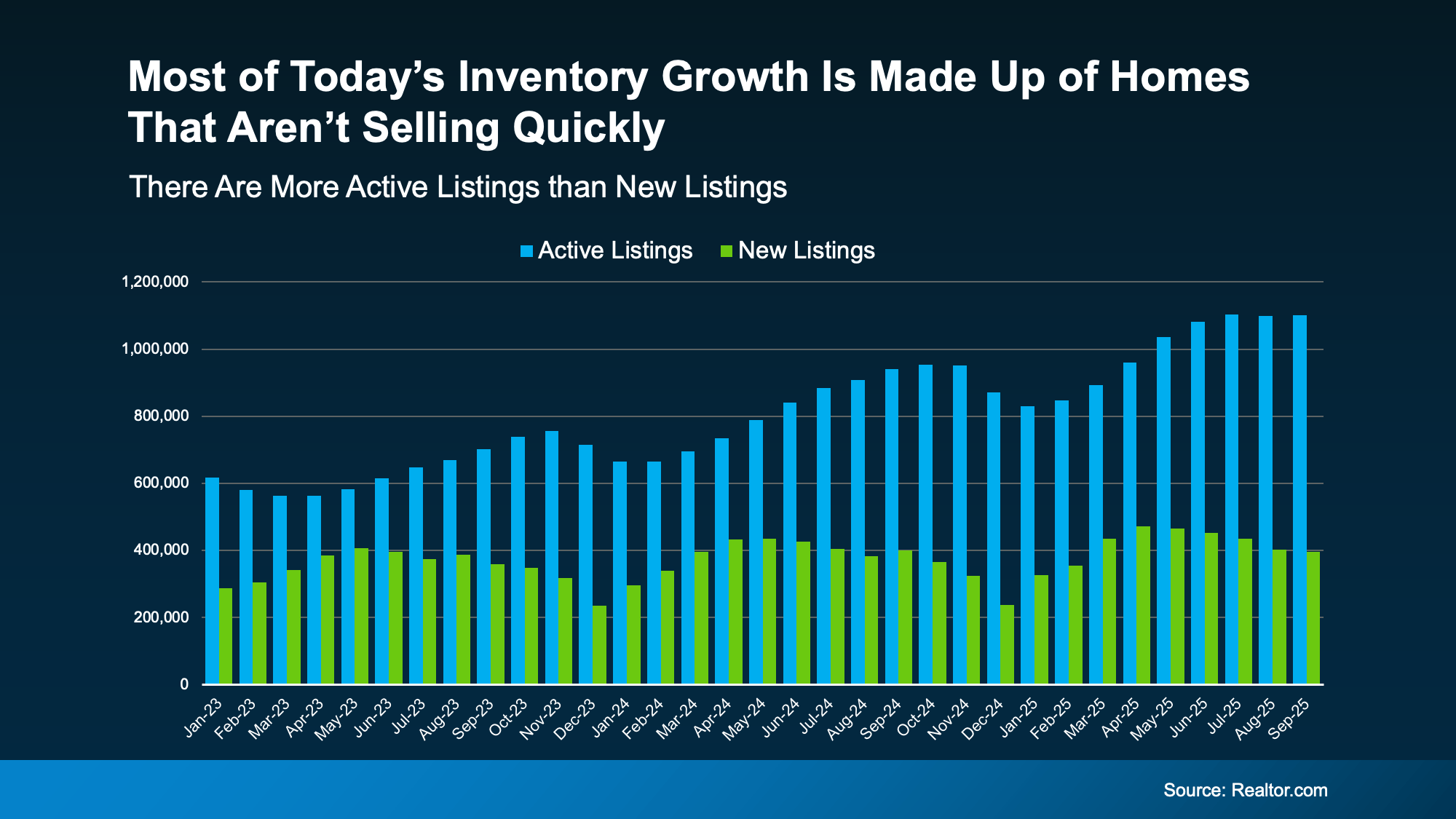

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

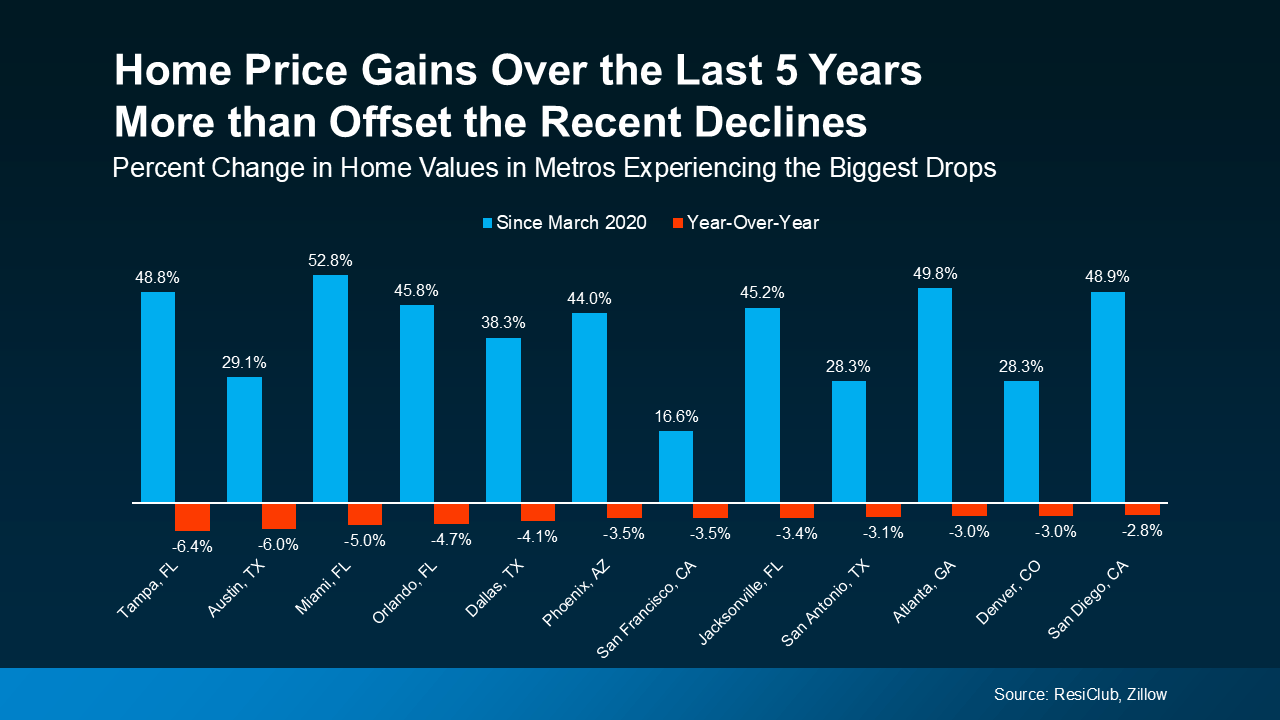

In other words, these modest declines can’t erase years of growth. Homeowners who’ve been in their houses for several years are still way ahead. Big time. And that’s true pretty much everywhere.

In other words, these modest declines can’t erase years of growth. Homeowners who’ve been in their houses for several years are still way ahead. Big time. And that’s true pretty much everywhere. Odds are, in most places, if you’ve owned your home for more than a few years, you’ve already built the kind of equity many people could only dream about before the pandemic. And if you sell, you can use it to help you downsize, or move up.

Odds are, in most places, if you’ve owned your home for more than a few years, you’ve already built the kind of equity many people could only dream about before the pandemic. And if you sell, you can use it to help you downsize, or move up.

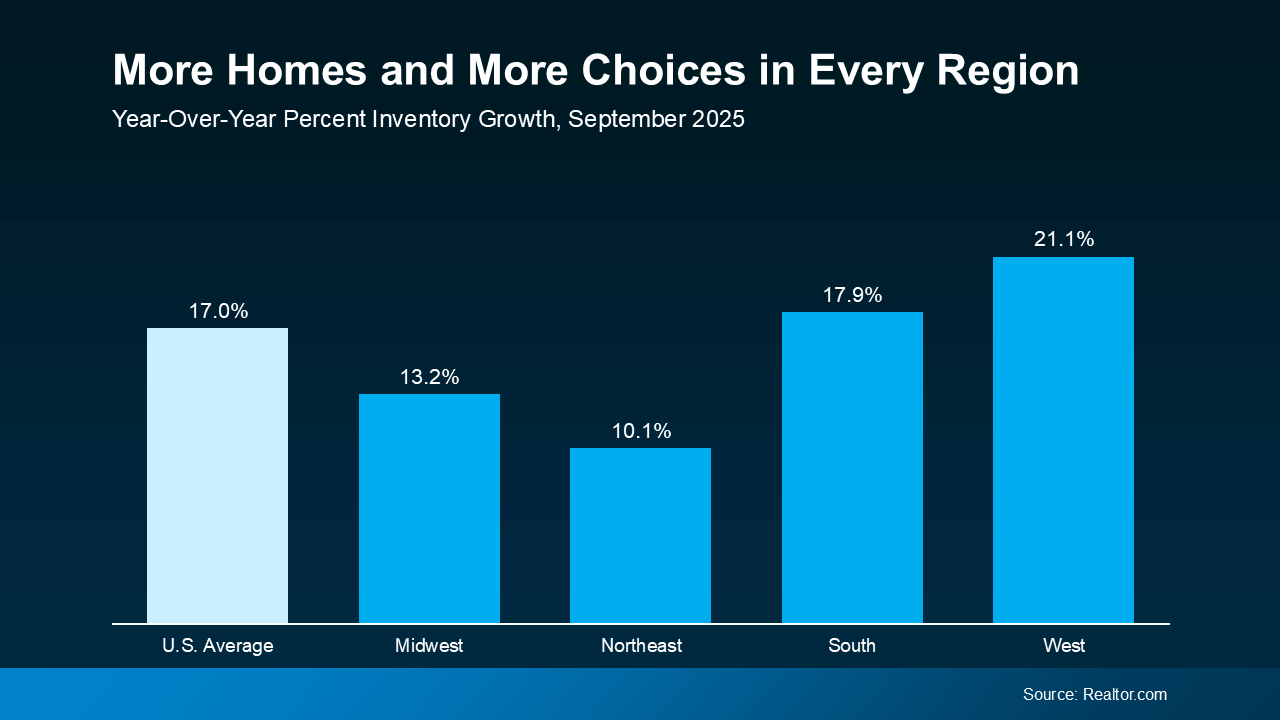

Here’s why that’s a sticking point for buyers right now:

Here’s why that’s a sticking point for buyers right now:

That translates to more homes to choose from, whether you’re looking for a bigger backyard, a shorter commute, or finally ditching your rental.

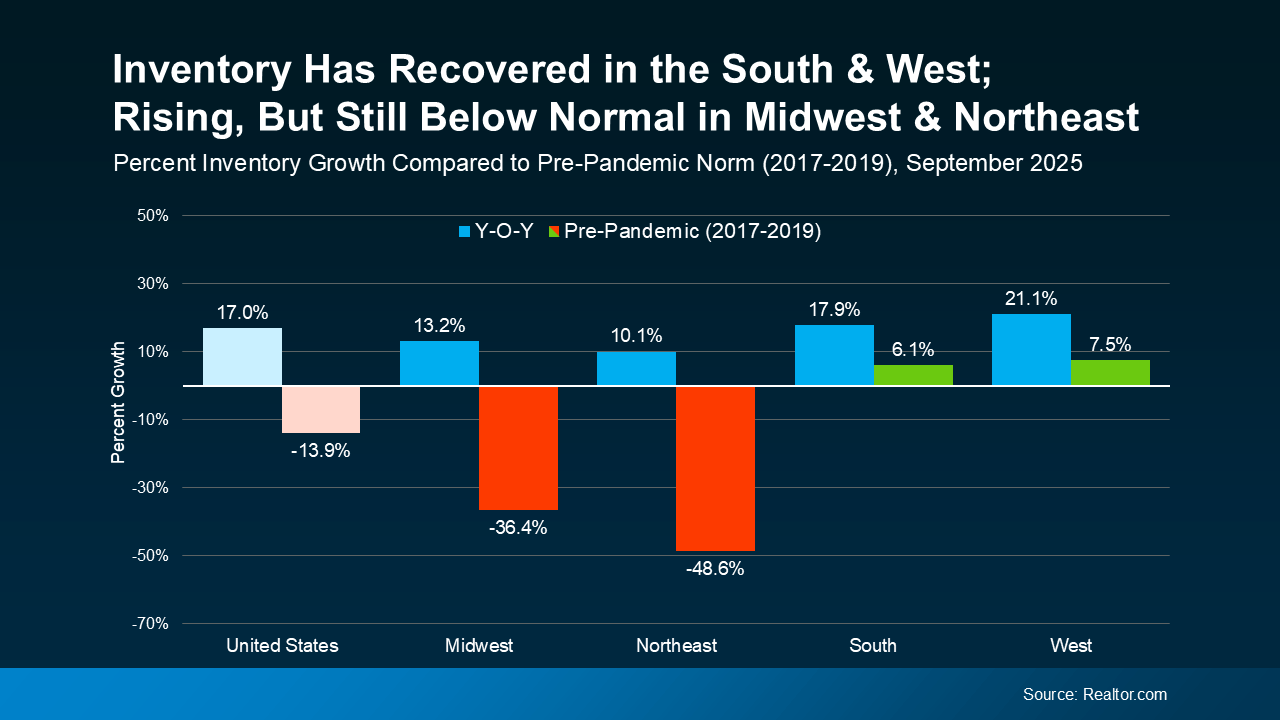

That translates to more homes to choose from, whether you’re looking for a bigger backyard, a shorter commute, or finally ditching your rental. The green bars show where inventory has fully recovered (and even grown above pre-pandemic levels) in the South and the West. Supply, however, is still tighter in the Northeast and Midwest, as shown in the red bars, where inventory is still below normal.

The green bars show where inventory has fully recovered (and even grown above pre-pandemic levels) in the South and the West. Supply, however, is still tighter in the Northeast and Midwest, as shown in the red bars, where inventory is still below normal.

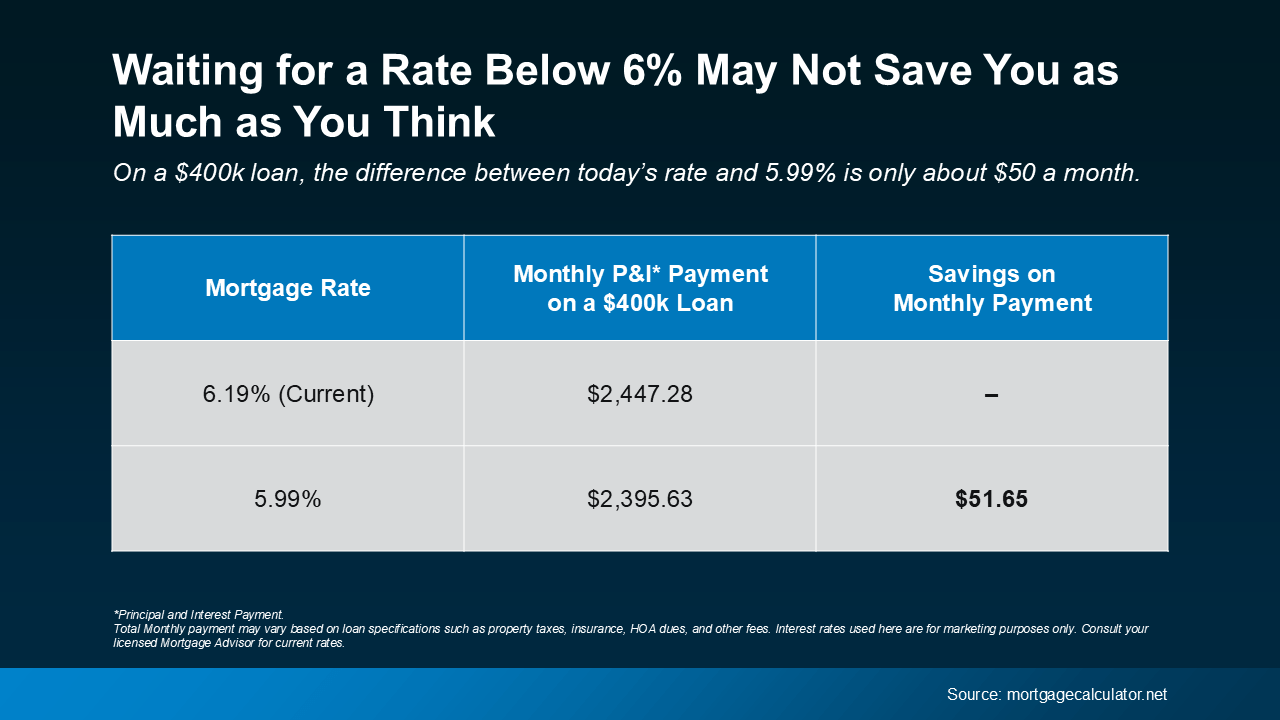

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

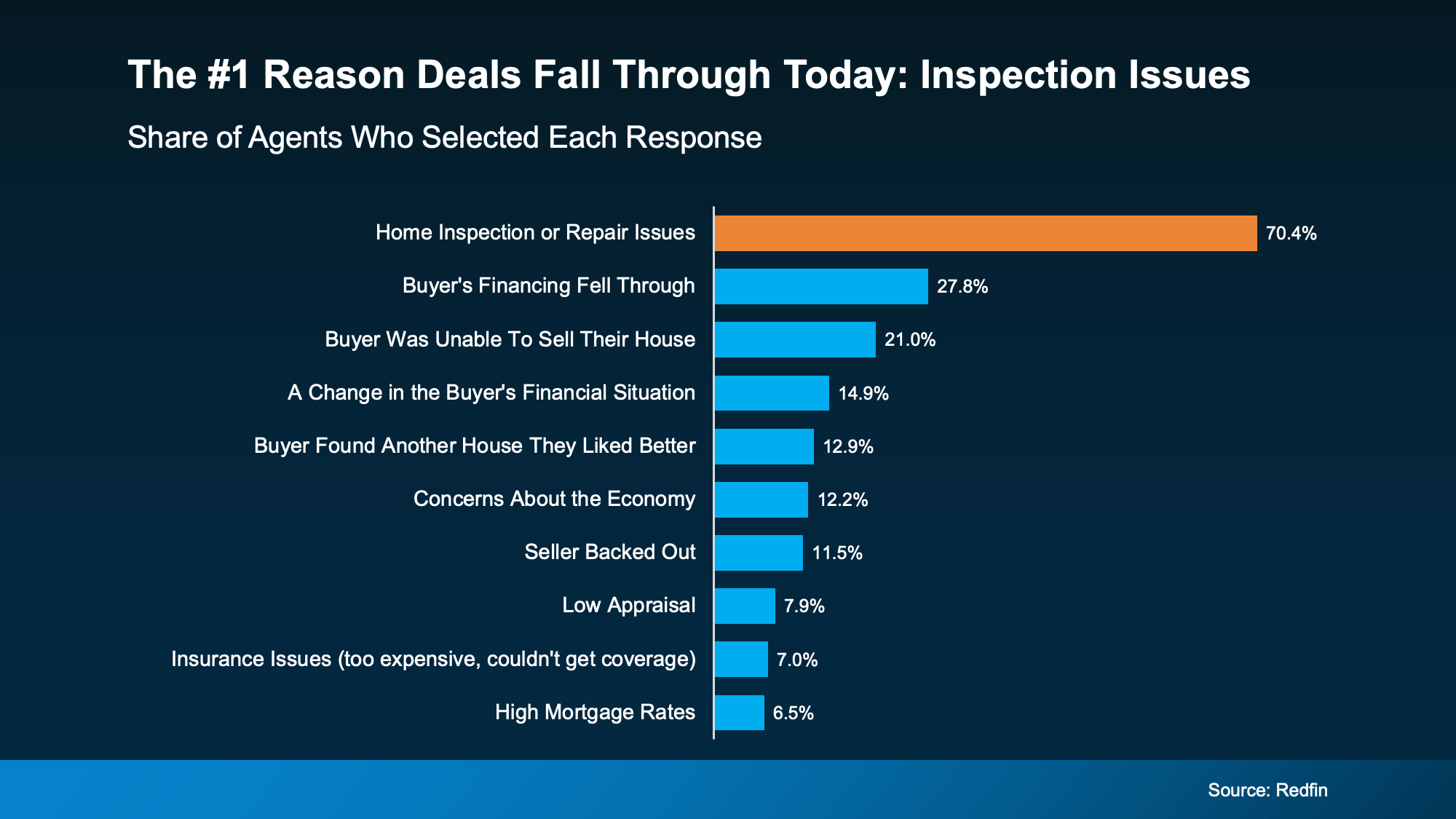

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

But that theory doesn’t actually hold up once you look at the data.

But that theory doesn’t actually hold up once you look at the data.

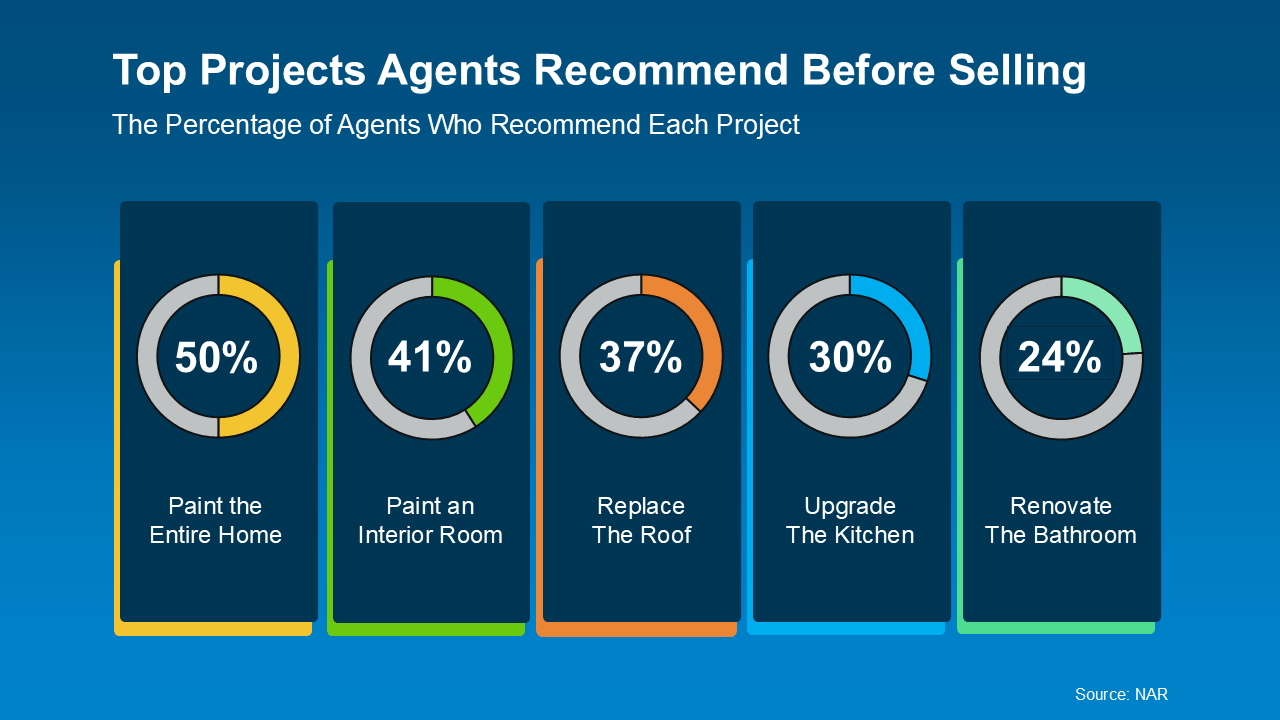

Just remember, what’s worth updating really depends on the homes you’re competing with in your market. Some areas don’t have a ton of inventory, so little updates may be all you need to tackle. In other areas, there are far more homes for sale, so you may need to do a bit more to make your house stand out.

Just remember, what’s worth updating really depends on the homes you’re competing with in your market. Some areas don’t have a ton of inventory, so little updates may be all you need to tackle. In other areas, there are far more homes for sale, so you may need to do a bit more to make your house stand out.

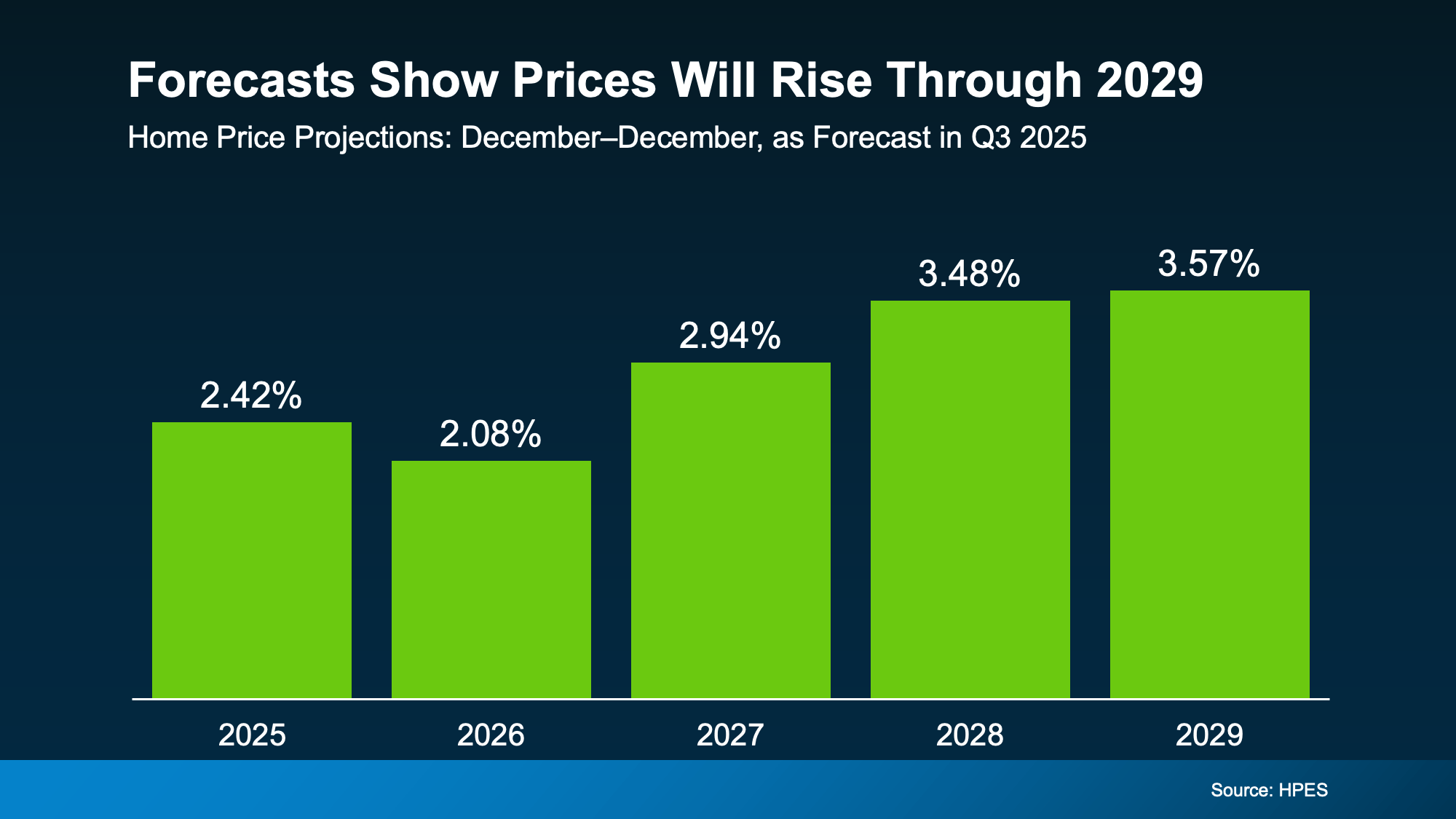

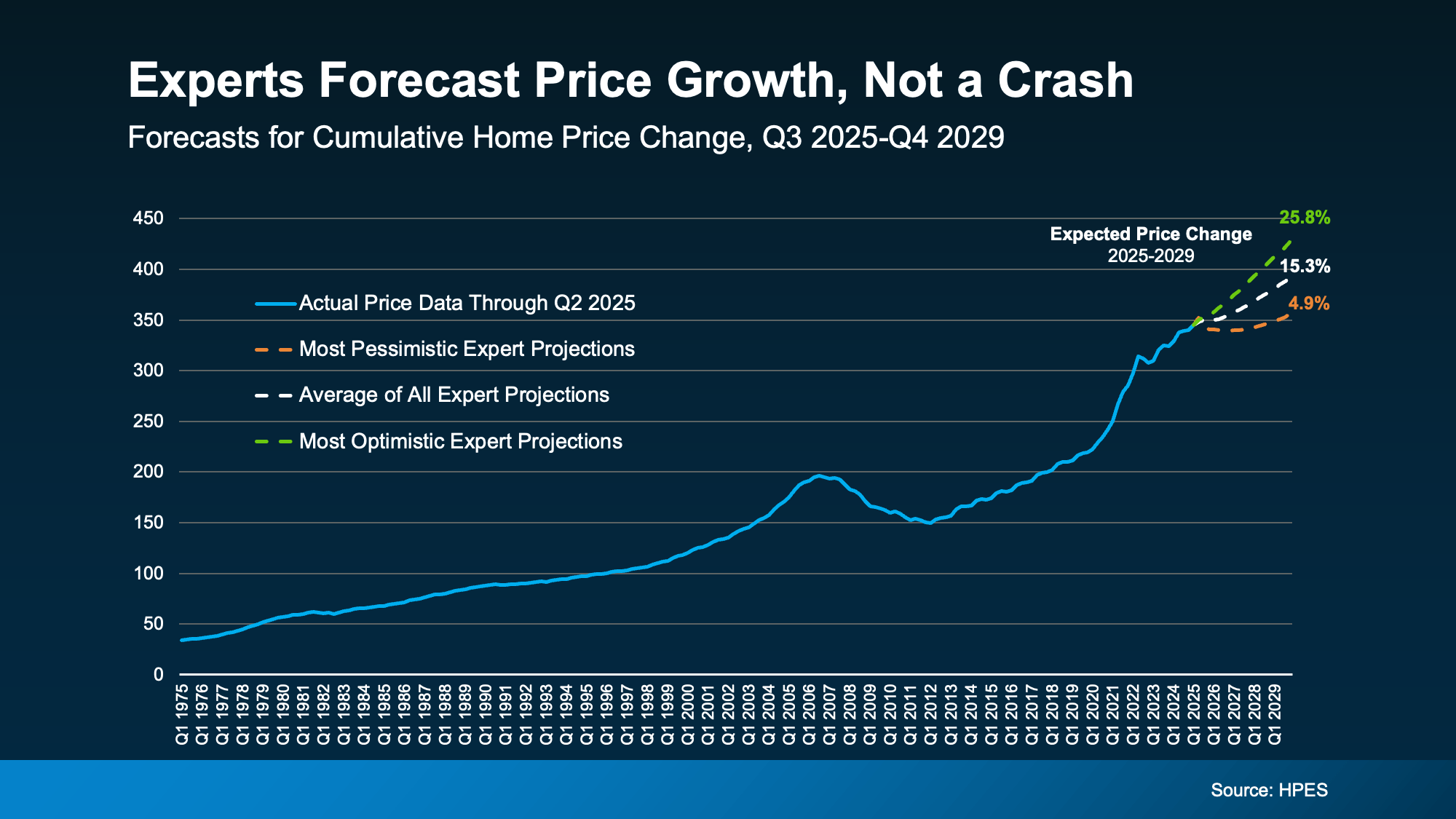

Here’s how to read this visual. Each bar in that graph shows an increase, not a loss. It’s just that the anticipated pace of that appreciation varies year-to-year.

Here’s how to read this visual. Each bar in that graph shows an increase, not a loss. It’s just that the anticipated pace of that appreciation varies year-to-year. Notice how even the most pessimistic forecasters say we’ll see prices rise by almost 5% over the next few years.

Notice how even the most pessimistic forecasters say we’ll see prices rise by almost 5% over the next few years.