If you paused your plans to move because of high rates or prices, it may finally be time to take a second look at your numbers. Affordability is improving in 39 of the top 50 markets, according to First American. And that’s the 5th straight month where buying a home has started to get a little bit easier.

Let’s break this down into real dollars, so you can see the difference this could make for you (and your move).

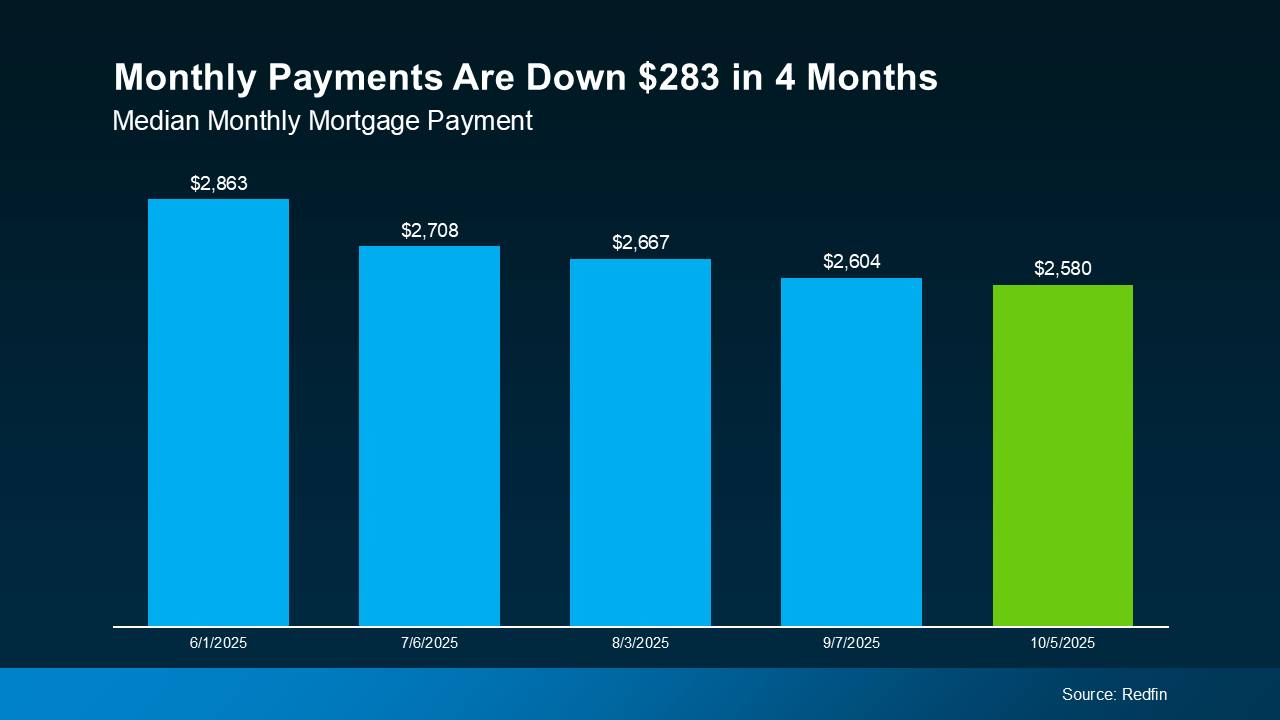

Monthly Payments Are Coming Down

One of the clearest signs of this shift is in monthly payments. The latest data from Redfin shows mortgage payments on a median-priced home are now $283 lower than they were just a few months ago (see graph below):

This kind of monthly savings adds up fast, and totals nearly $3,400 over the course of a year.

This kind of monthly savings adds up fast, and totals nearly $3,400 over the course of a year.

While this isn’t enough to completely change the affordability game overnight, think about it this way. When you’re putting together a homebuying budget, a few hundred dollars could be the difference between being comfortable buying and feeling like money’s a bit tight.

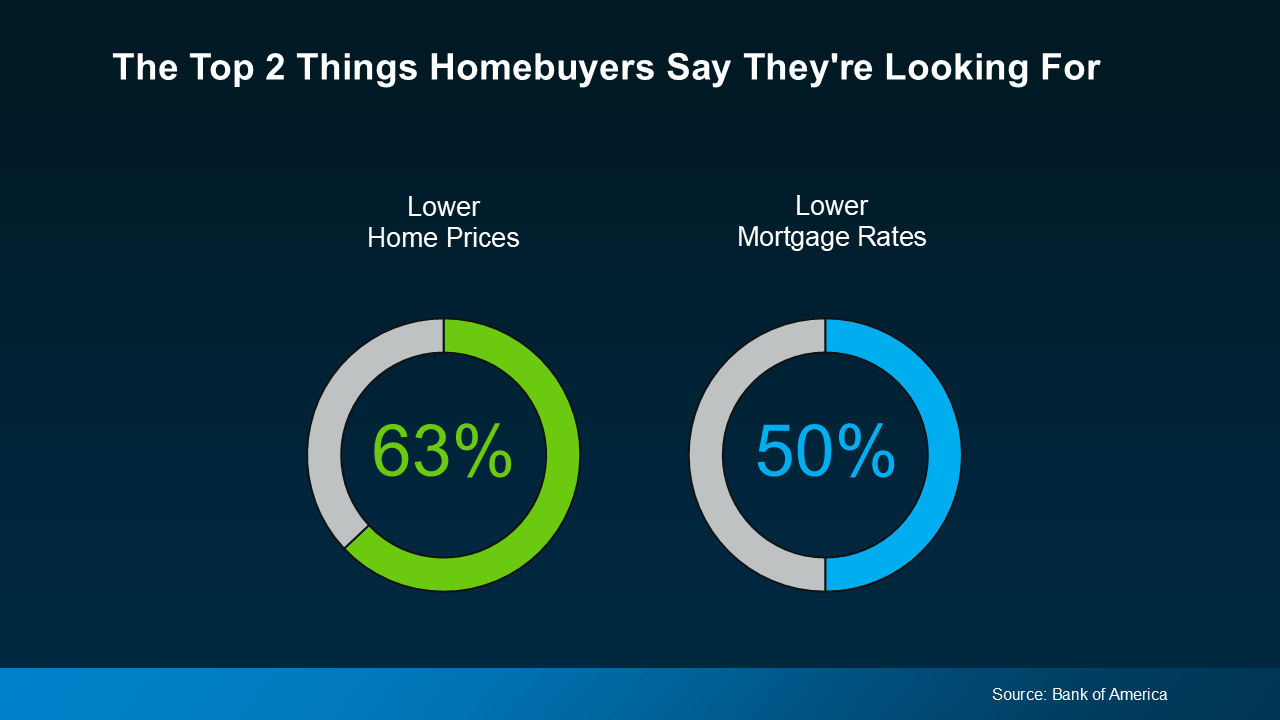

And from a home-search perspective, it could even be enough to change the price point you can look at. According to Redfin:

“A borrower with a $3,000 monthly budget can now afford a $468,000 home, about $22,000 more than in June."

And that’s a big deal if you haven’t found a home you love in your price range yet. It gives you a little more flexibility to find the one that’s right for you.

Either way, that’s a big win.

What’s Behind the Shift?

Two key factors are working in your favor right now:

- Mortgage rates have eased from their high earlier this year

- Home price growth is slowing in many markets

Both of those things help your bottom line and give you a bit of breathing room if you’re buying a home. As Andy Walden, Head of Mortgage and Housing Market Research at ICE Mortgage Technology, says:

“The recent pullback in rates has created a tailwind for both homebuyers and existing borrowers. We’re seeing affordability at a 2.5-year high . . .”

Whether you’re a first-time homebuyer or someone looking to move-up into a bigger house, the shifts happening this year could make your move possible. Connect with a trusted agent or lender to see what your monthly payment would look like at today’s rates.

For you, the savings could be the difference between “not yet” and “let’s go.”

Bottom Line

Affordability is improving in many markets. And that resets the math on your move.

If you’ve been sitting on the sidelines, this is your cue to start looking again. Connect with a local agent or trusted lender to run the numbers together so you can get a rough estimate of how much more buying power you may have than you did just a few months ago.

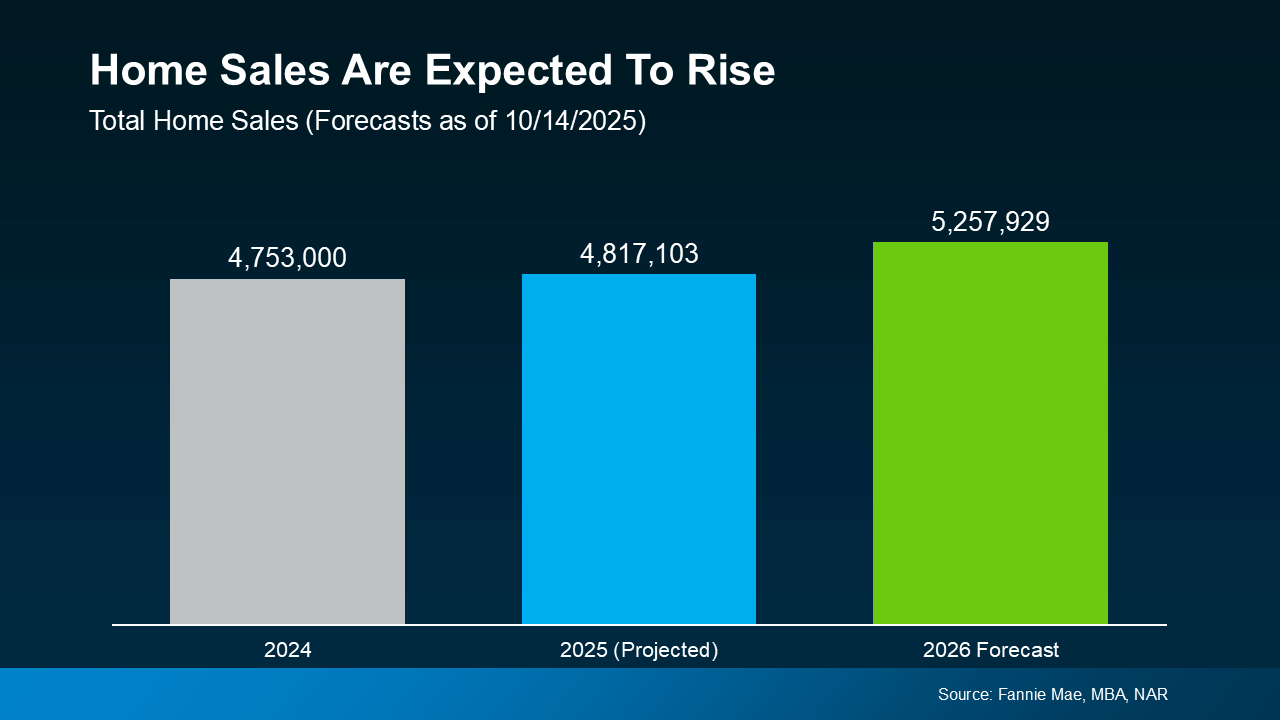

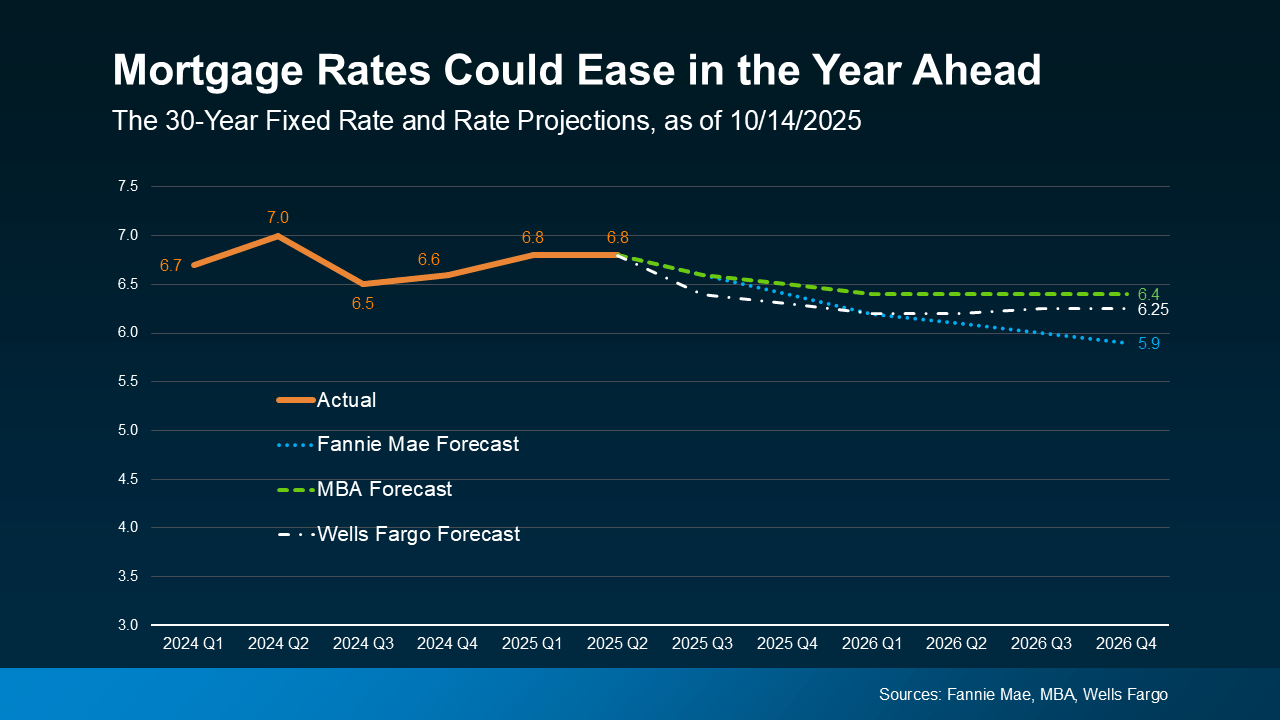

What’s behind the change? Two key factors: mortgage rates and home prices. Let’s dive into the latest expert forecasts for both, so you can see why more people are expected to move next year.

What’s behind the change? Two key factors: mortgage rates and home prices. Let’s dive into the latest expert forecasts for both, so you can see why more people are expected to move next year. There’s a saying: when rates go up, they take the escalator. But when they come down, they take the stairs. And that’s an important thing to remember. It’ll be a slow and bumpy process.

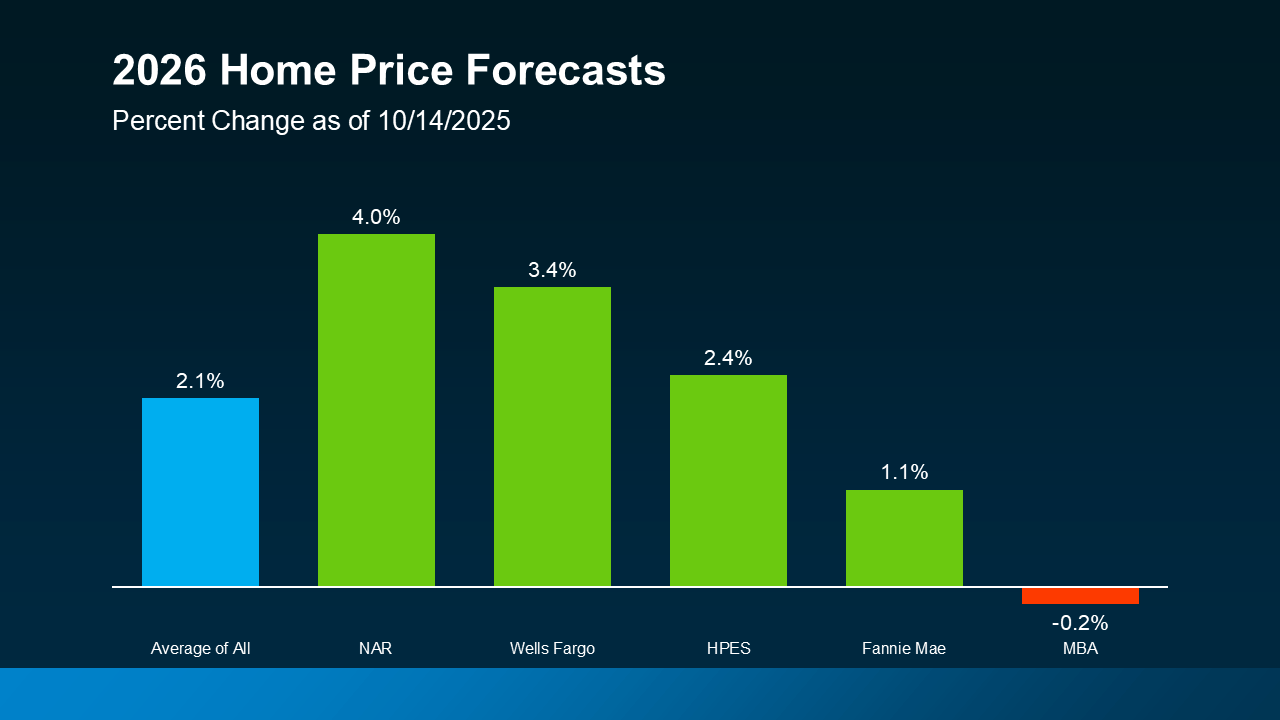

There’s a saying: when rates go up, they take the escalator. But when they come down, they take the stairs. And that’s an important thing to remember. It’ll be a slow and bumpy process. This is yet another good sign for buyers and overall affordability. While prices will still go up nationally, it’ll be at a much more sustainable pace. And that predictability makes it easier to plan your budget. It also gives you peace of mind that prices won’t suddenly skyrocket overnight.

This is yet another good sign for buyers and overall affordability. While prices will still go up nationally, it’ll be at a much more sustainable pace. And that predictability makes it easier to plan your budget. It also gives you peace of mind that prices won’t suddenly skyrocket overnight.

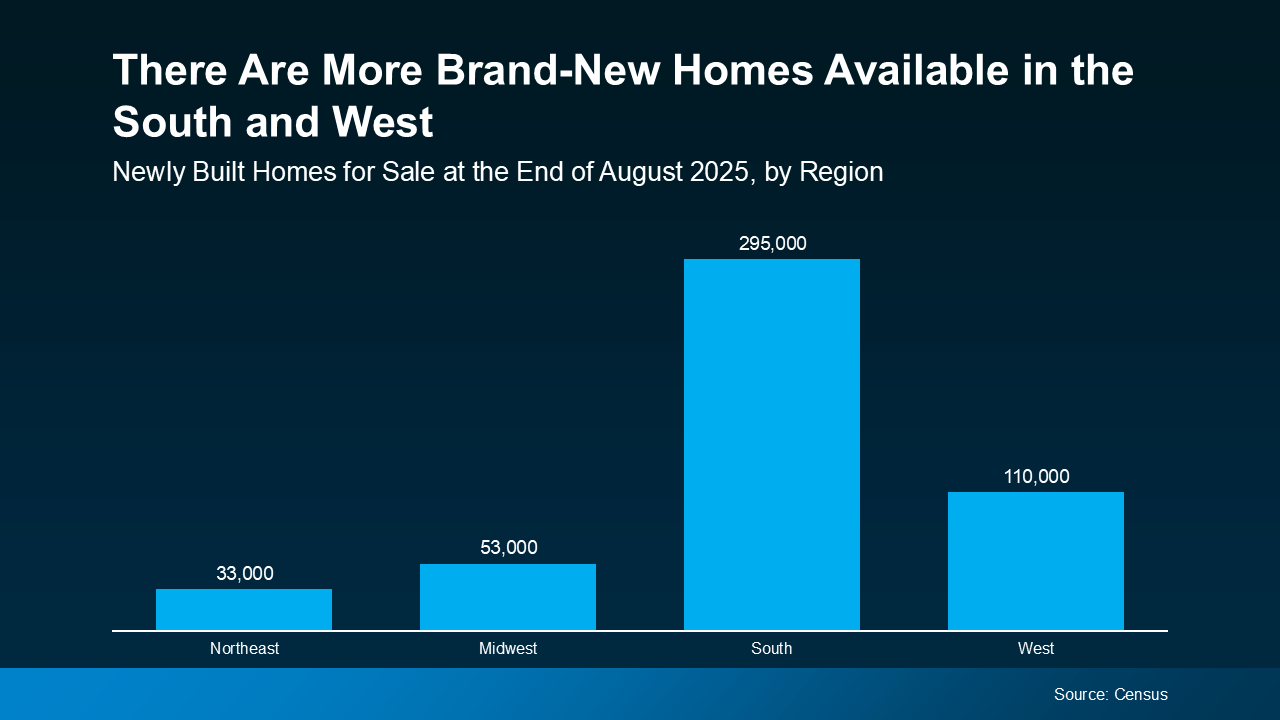

Why Builders Are Throwing in Perks

Why Builders Are Throwing in Perks Both the South and West have more new homes available, so you may find builders are even more willing to negotiate in these regions.

Both the South and West have more new homes available, so you may find builders are even more willing to negotiate in these regions.

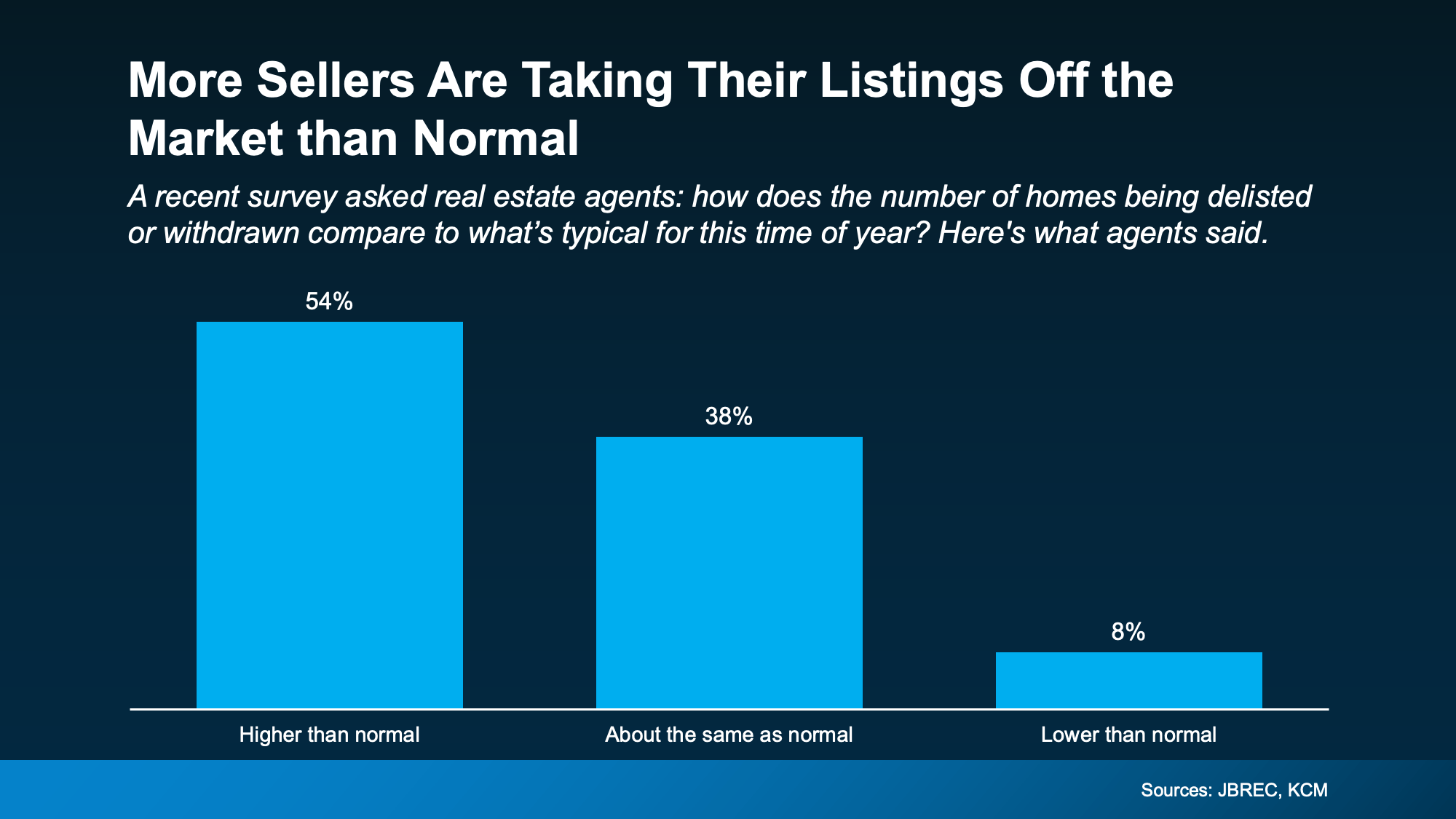

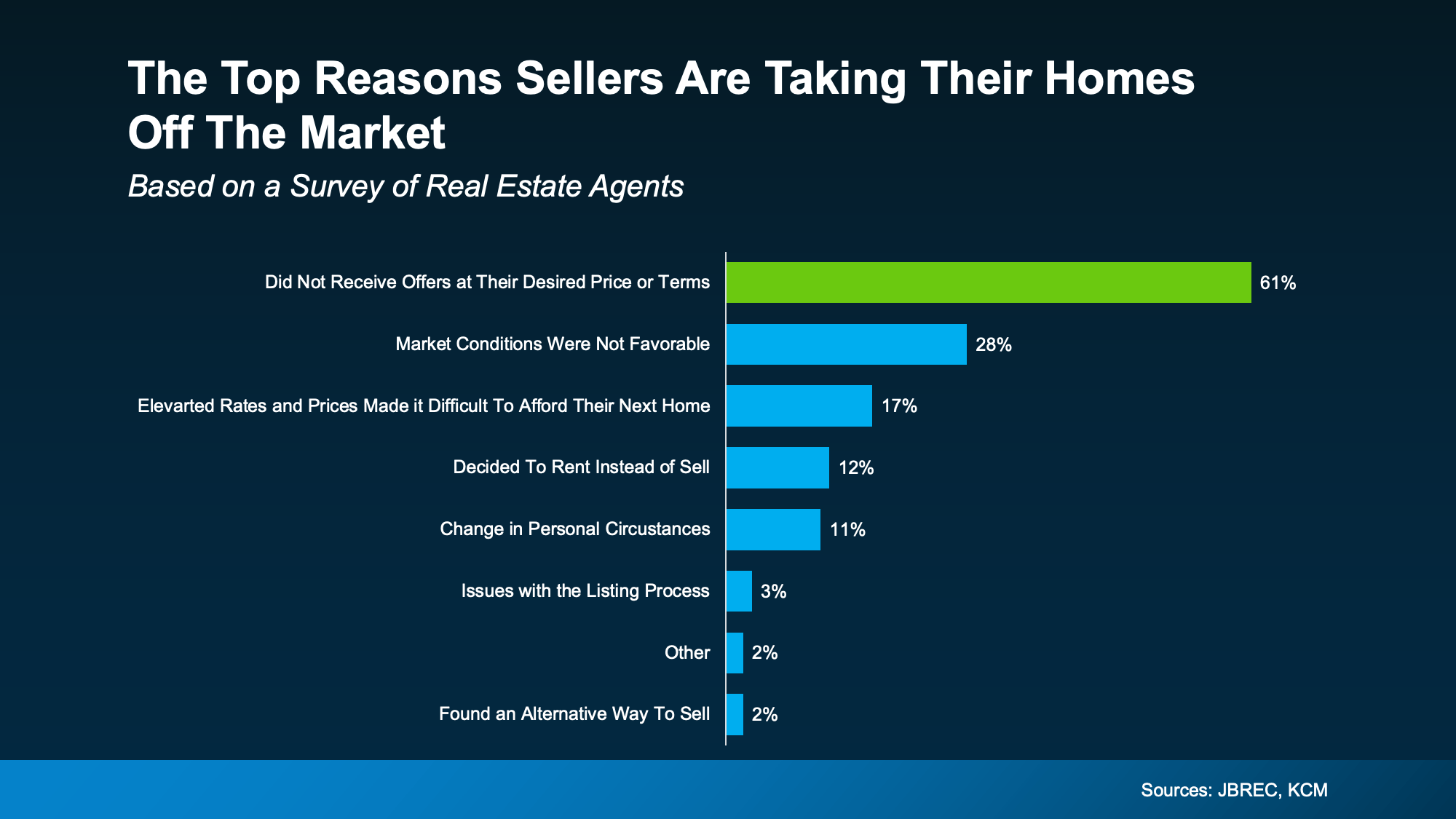

And the top reasons for that? According to the agents, homeowners didn’t get any offers they felt were fair. The survey from JBREC and KCM explains it like this:

And the top reasons for that? According to the agents, homeowners didn’t get any offers they felt were fair. The survey from JBREC and KCM explains it like this: BrightMLS data backs this up:

BrightMLS data backs this up:

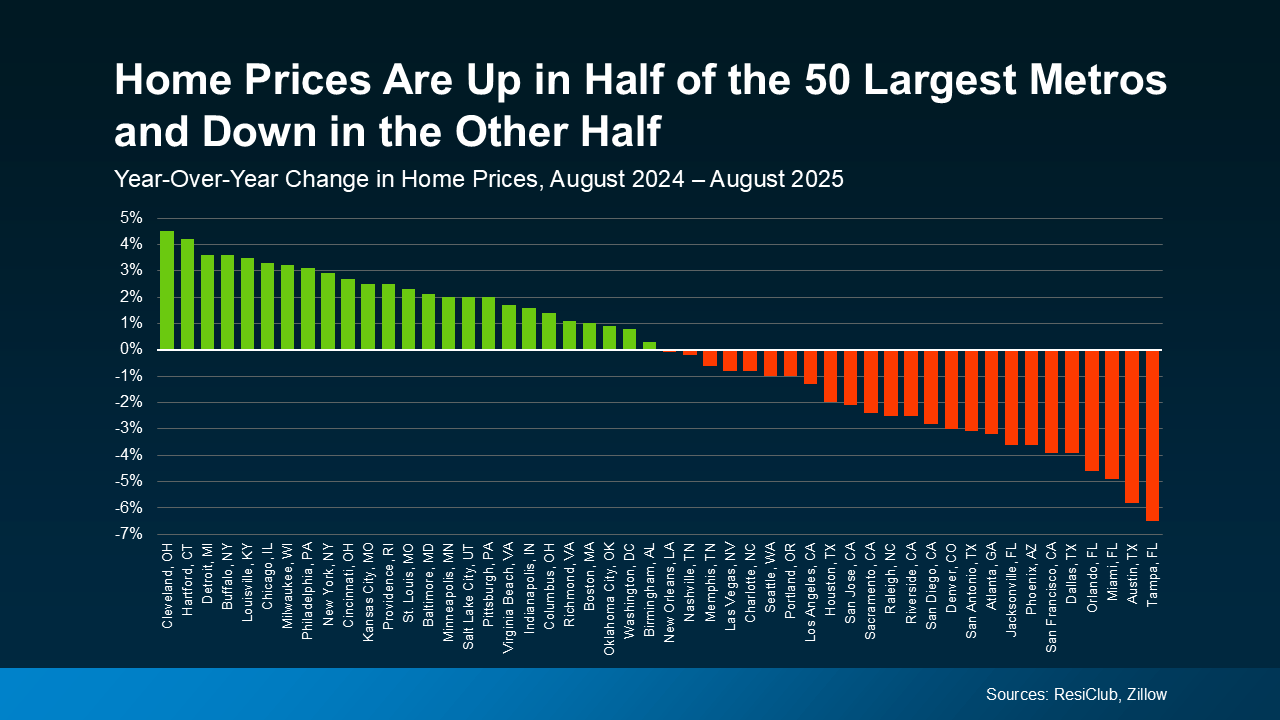

The big takeaway here is “flat” doesn’t mean prices are holding steady everywhere. What the numbers actually show is how much price trends are going to vary depending on where you are.

The big takeaway here is “flat” doesn’t mean prices are holding steady everywhere. What the numbers actually show is how much price trends are going to vary depending on where you are.

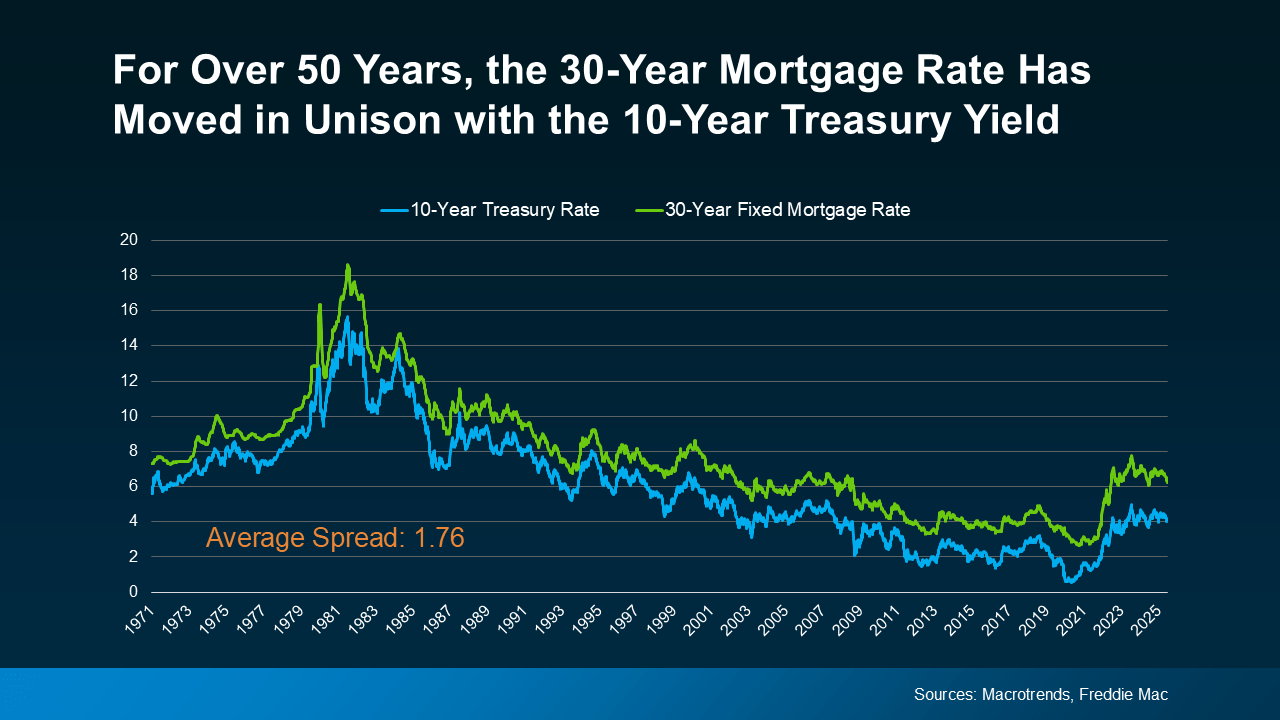

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down.

When the treasury yield climbs, mortgage rates tend to follow. And when the yield falls, mortgage rates typically come down. And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains:

And that opens the door for mortgage rates to come down even more. As a recent article from Redfin explains: But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

But remember, all of that can change as the economy shifts. And know for certain that there will be ups and downs along the way.

Here’s the good news. While the broader economy may still feel uncertain, there are signs the housing market is showing some changes in both of those areas. Let’s break it down so you know what you’re working with.

Here’s the good news. While the broader economy may still feel uncertain, there are signs the housing market is showing some changes in both of those areas. Let’s break it down so you know what you’re working with.

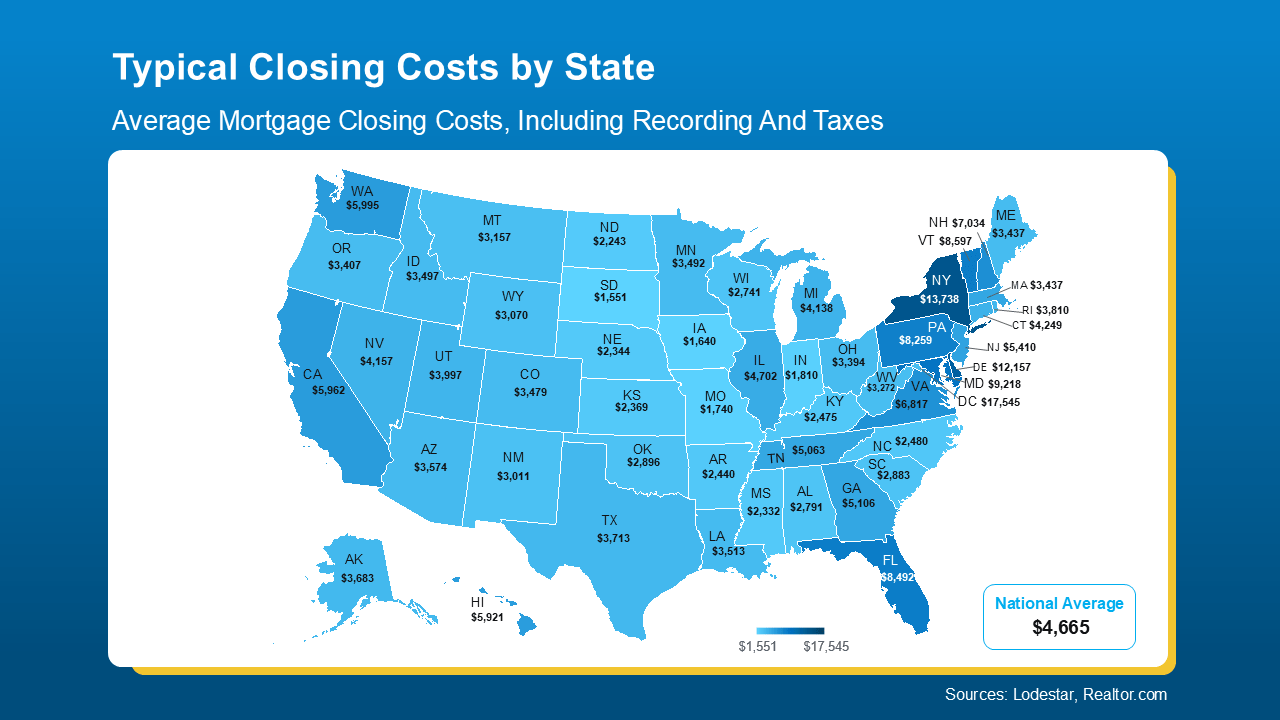

As the map shows, in some states, typical closing costs are just roughly $1-3K. In a few places, they can be closer to $10-15K. That’s a big swing, especially if you’re buying your first home. And that’s why knowing what to expect matters.

As the map shows, in some states, typical closing costs are just roughly $1-3K. In a few places, they can be closer to $10-15K. That’s a big swing, especially if you’re buying your first home. And that’s why knowing what to expect matters.

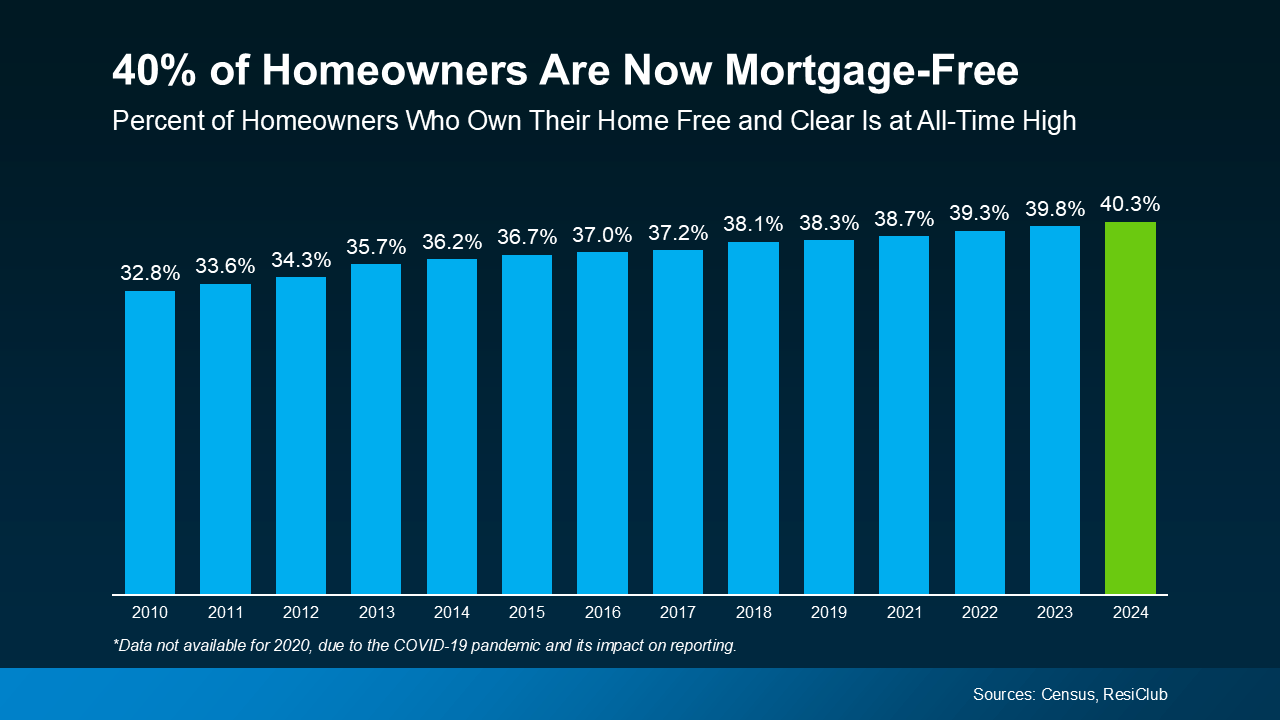

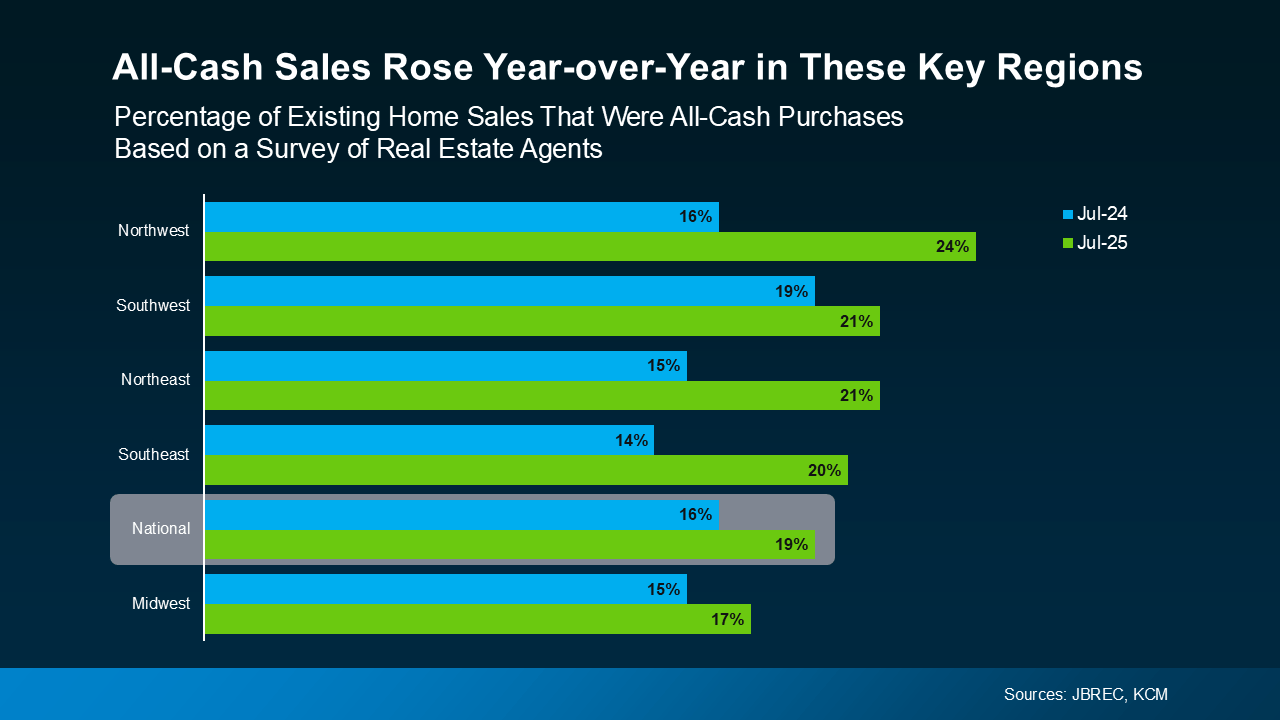

One big reason for this trend? Demographics. As Baby Boomers age and stay in their homes longer, many have had the time to fully pay off their mortgages. You might be in that group too and not even realize just how much buying power you now have. It’s time to change that.

One big reason for this trend? Demographics. As Baby Boomers age and stay in their homes longer, many have had the time to fully pay off their mortgages. You might be in that group too and not even realize just how much buying power you now have. It’s time to change that. For Baby Boomers especially, buying in cash gives you more control over your next chapter. You could buy a smaller, less expensive home and have lower costs, less upkeep, and more flexibility to enjoy what matters most. All while staying debt and stress free.

For Baby Boomers especially, buying in cash gives you more control over your next chapter. You could buy a smaller, less expensive home and have lower costs, less upkeep, and more flexibility to enjoy what matters most. All while staying debt and stress free.