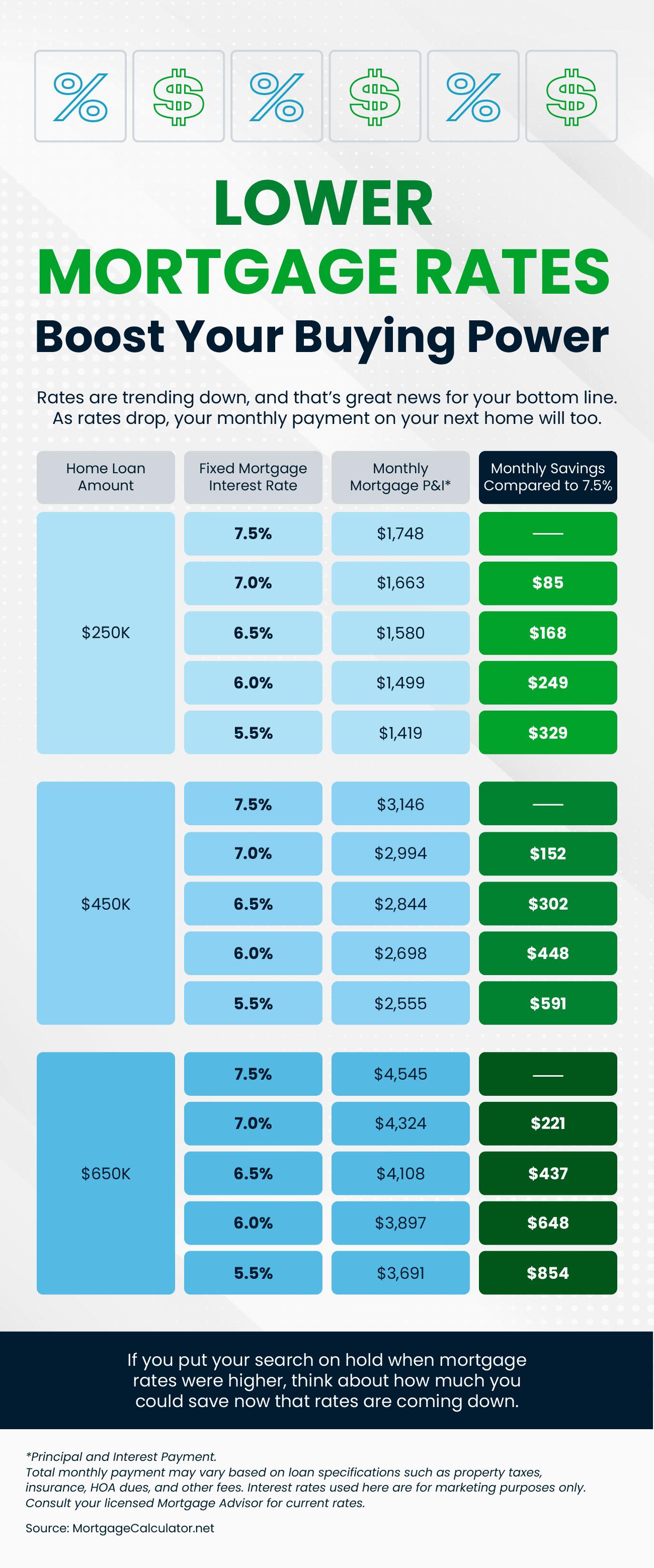

Some Highlights

- Mortgage rates are trending down and that’s great news for your bottom line.

- As rates drop, your monthly payment on your next home does too. Even a small change in mortgage rates can have a big impact on your purchasing power.

- If you put your search on hold when mortgage rates were higher, think about how much you could save now that rates are coming down.

What This Means for You

What This Means for You

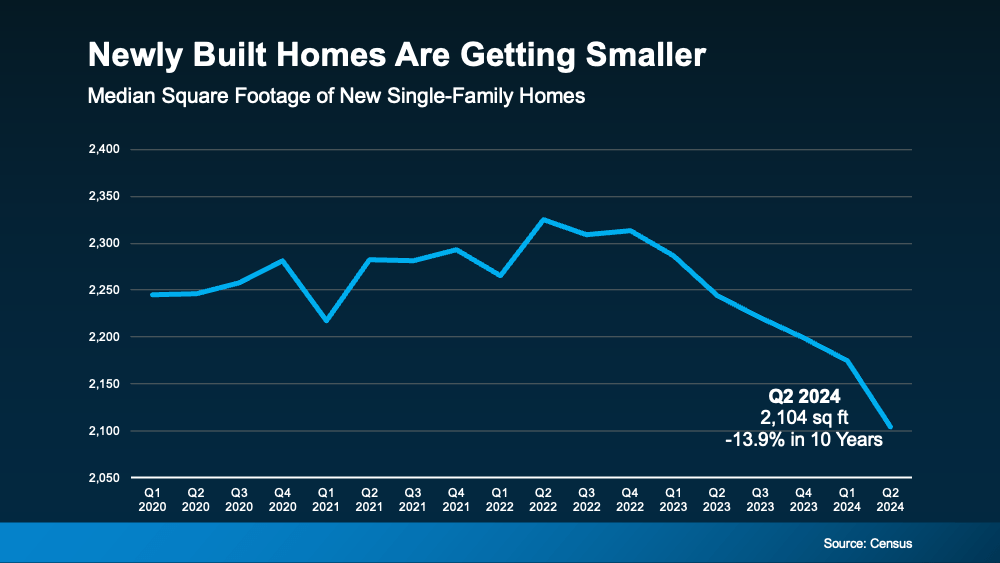

But why would builders want to build smaller homes right now? At the end of the day, builders are going to focus on building homes that meet current market demand – because they want to build what they know will sell. And the number one thing homebuyers are looking for right now is better affordability. Since smaller homes typically come with smaller price tags, both buyers and builders have shifted their focus to homes with less square footage. The National Association of Home Builders (NAHB) reports:

But why would builders want to build smaller homes right now? At the end of the day, builders are going to focus on building homes that meet current market demand – because they want to build what they know will sell. And the number one thing homebuyers are looking for right now is better affordability. Since smaller homes typically come with smaller price tags, both buyers and builders have shifted their focus to homes with less square footage. The National Association of Home Builders (NAHB) reports:

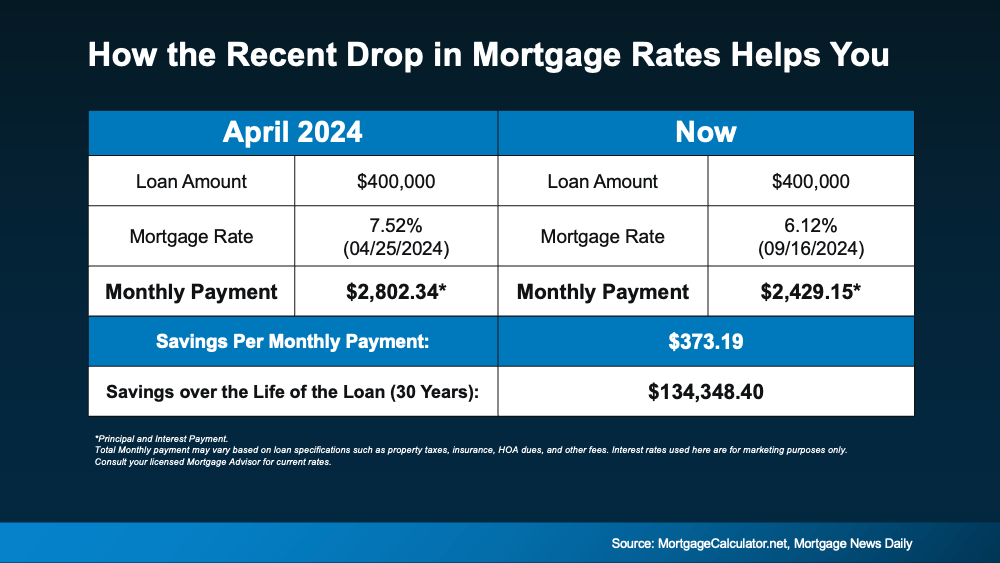

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

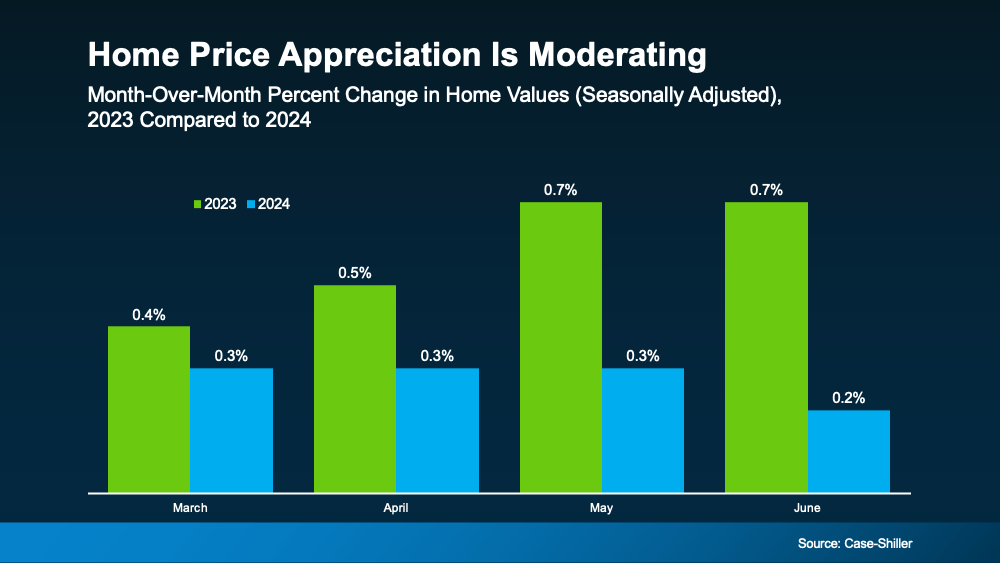

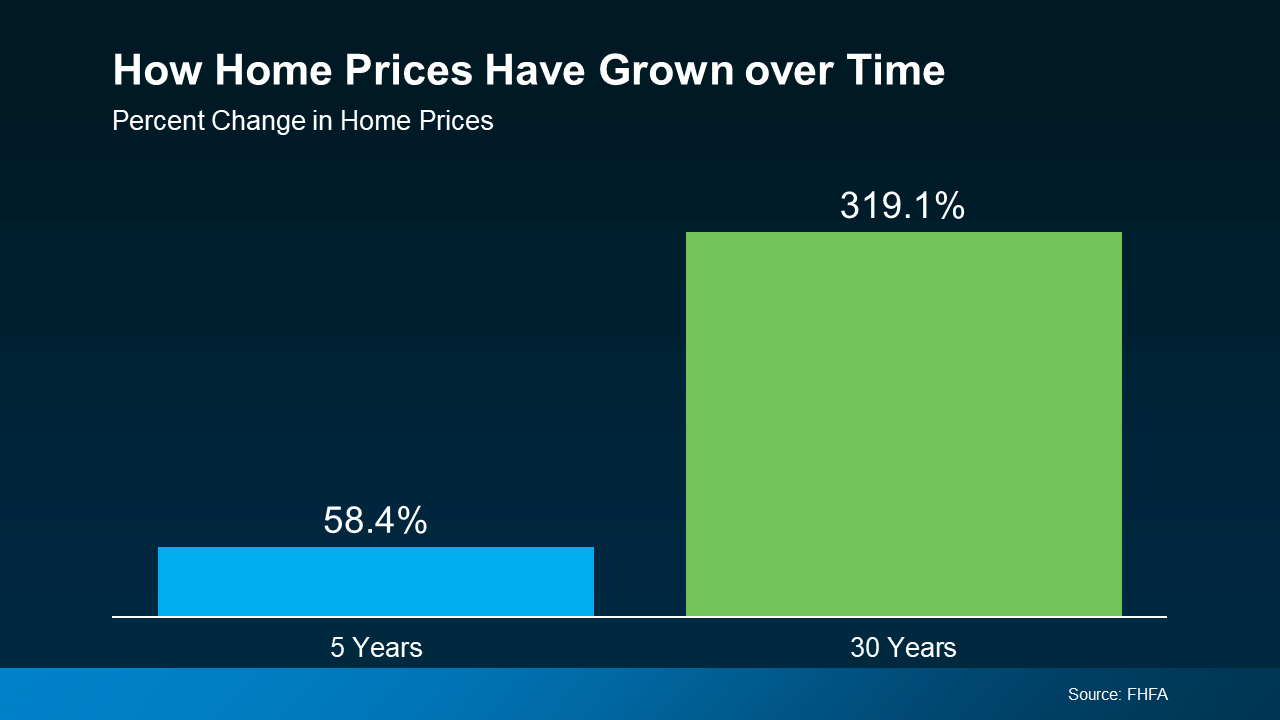

But rest assured, this doesn't mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they're not climbing as fast as they were when they skyrocketed just a few years ago.

But rest assured, this doesn't mean home prices are falling. In fact, all the bars in this graph show price growth. So, while you might hear talk of prices cooling, what that really means is they're not climbing as fast as they were when they skyrocketed just a few years ago.

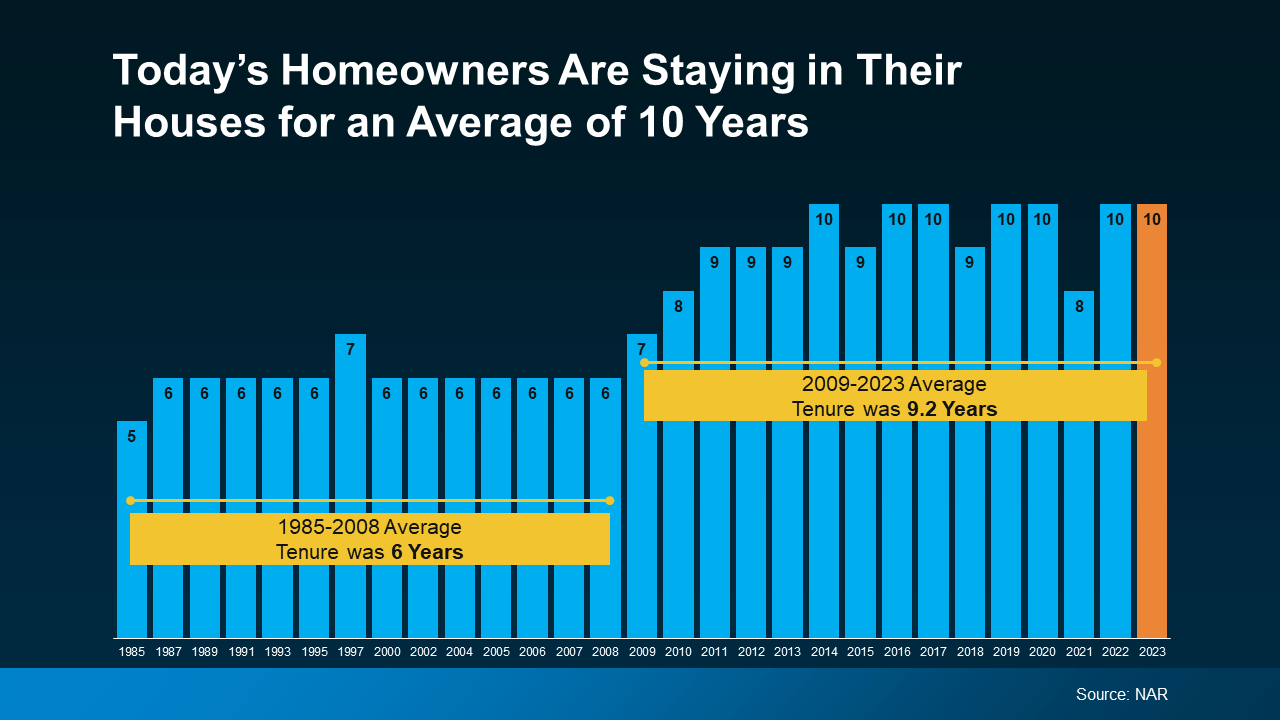

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity.

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity. Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.

Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.