One of the biggest questions on everyone’s minds right now is: when will mortgage rates come down? After several years of rising rates and a lot of bouncing around in 2024, we’re all eager for some relief.

While no one can project where rates will go with complete accuracy or the exact timing, experts offer some insight into what we might see going into next year. Here’s what the latest forecasts show.

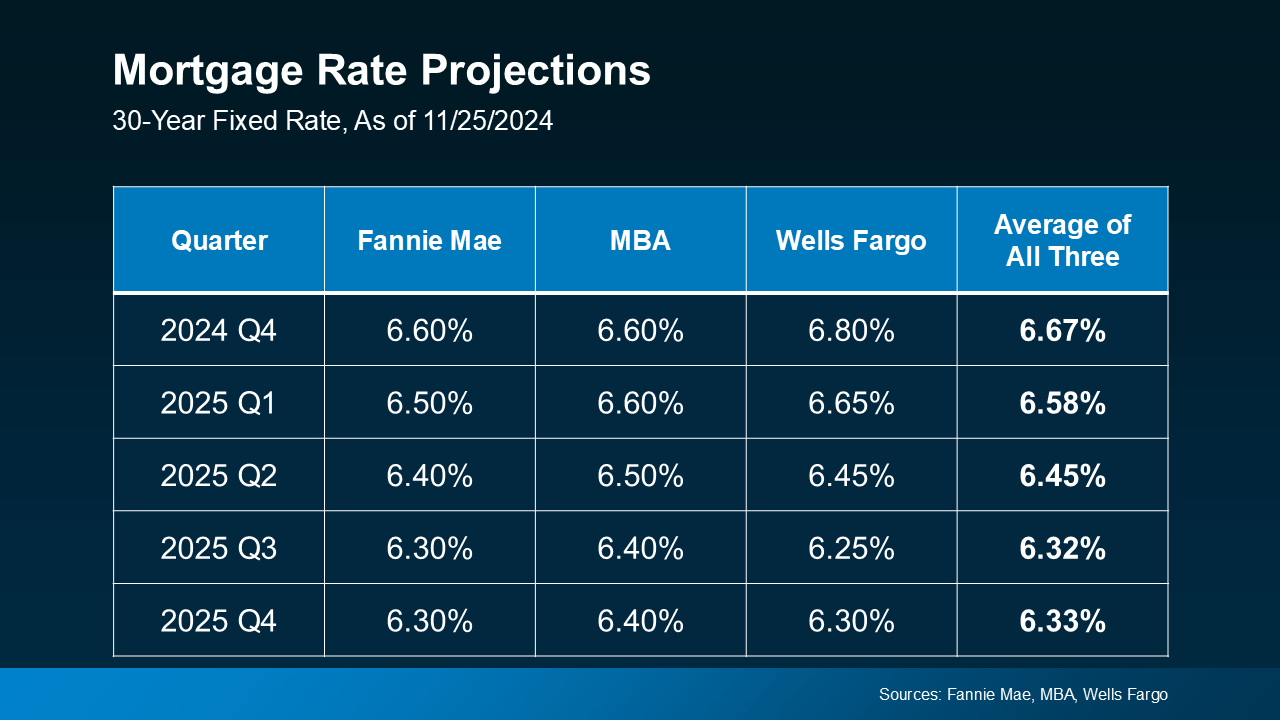

Mortgage Rates Are Expected To Ease and Stabilize in 2025

After a lot of volatility and uncertainty, the most updated forecasts suggest rates will start to stabilize over the next year, and should ease a bit compared to where they are right now (see graph below):

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“While mortgage rates remain elevated, they are expected to stabilize.”

Key Factors That’ll Impact the Future of Mortgage Rates

It’s important to note that the timing and the pace of what happens with mortgage rates is one of the most challenging forecasts to make in the housing market. That’s because these forecasts hinge on a few key factors all lining up. So don’t be fooled, because while rates are expected to come down slightly, they’re going to be a moving target. And the ups and downs of ongoing economic drivers will likely stick around. Here’s a look at just a few of the things that’ll influence where they go from here:

- Inflation: If inflation cools, rates could dip a bit more. On the flip side, if inflation rises or remains stubbornly high, rates may stay elevated longer.

- Unemployment Rate: The unemployment rate also plays a significant role in upcoming decisions by the Federal Reserve (the Fed). And while the Fed doesn’t set mortgage rates, their actions do reflect what’s happening in the greater economy, which can have an impact.

- Government Policies: With the next administration set to take office in January, fiscal and monetary policies could also affect how financial markets respond and where rates go from here.

Remember, these forecasts are based on the best information available right now. As new economic data comes out, experts will revise their projections accordingly. So, don’t try to time the market based on these forecasts alone.

Instead, the best thing you can do is focus on what you can control right now. Work on improving your credit score, put away any extra cash for your down payment, and automate your savings. All of these things will help you reach your homeownership goals even faster.

And be sure to connect with a trusted agent and a lender, so you always have the latest updates – and an expert opinion on what that means for your move.

Bottom Line

If you’re planning to move and want to stay informed about where mortgage rates are heading, connect with a trusted agent and lender.

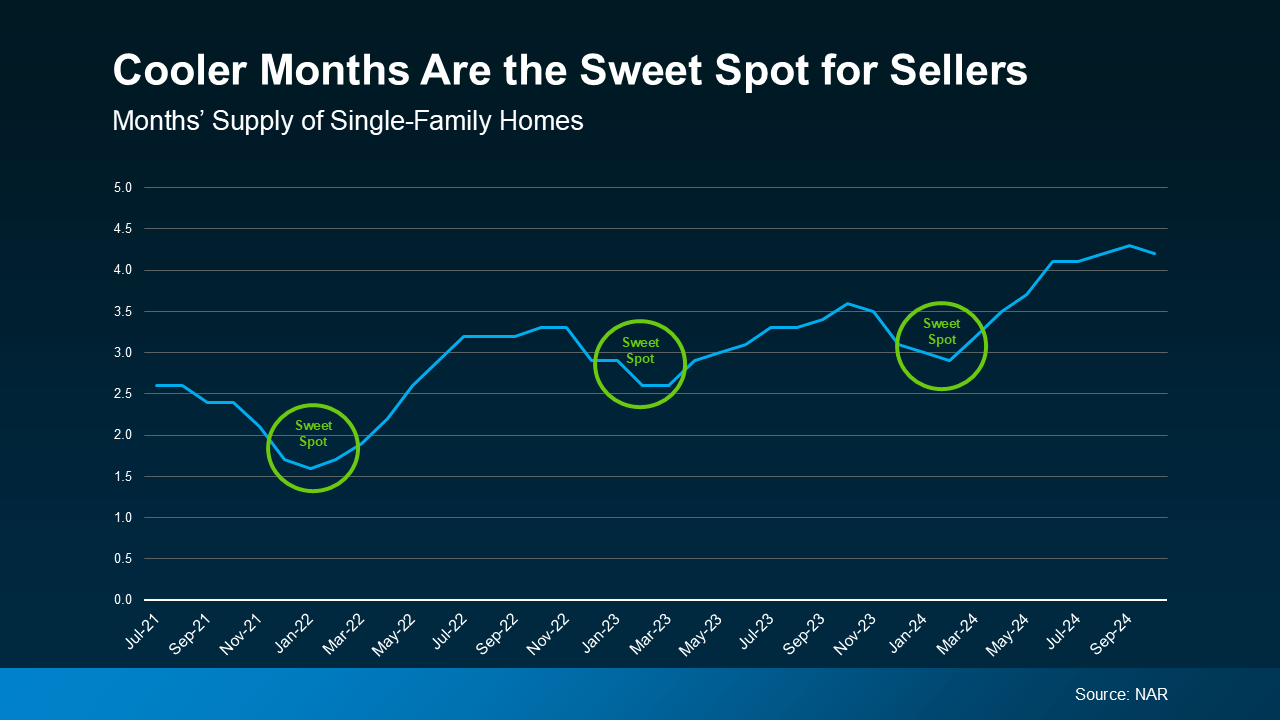

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

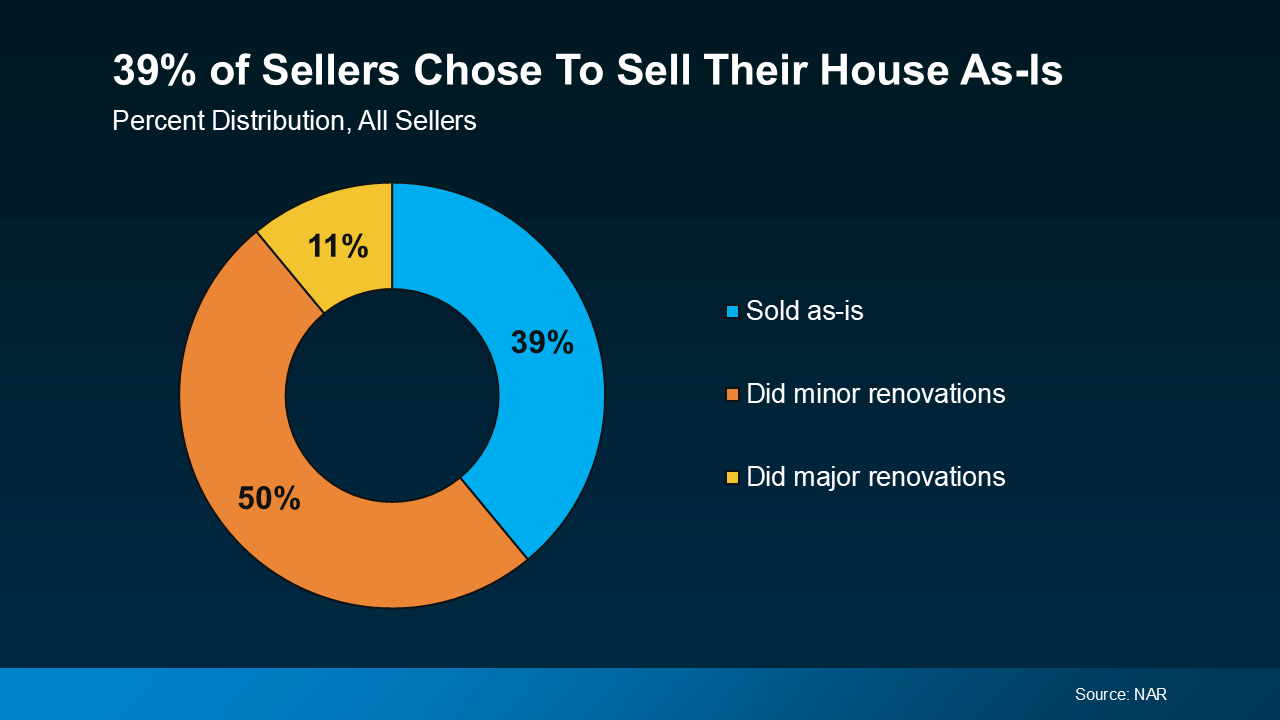

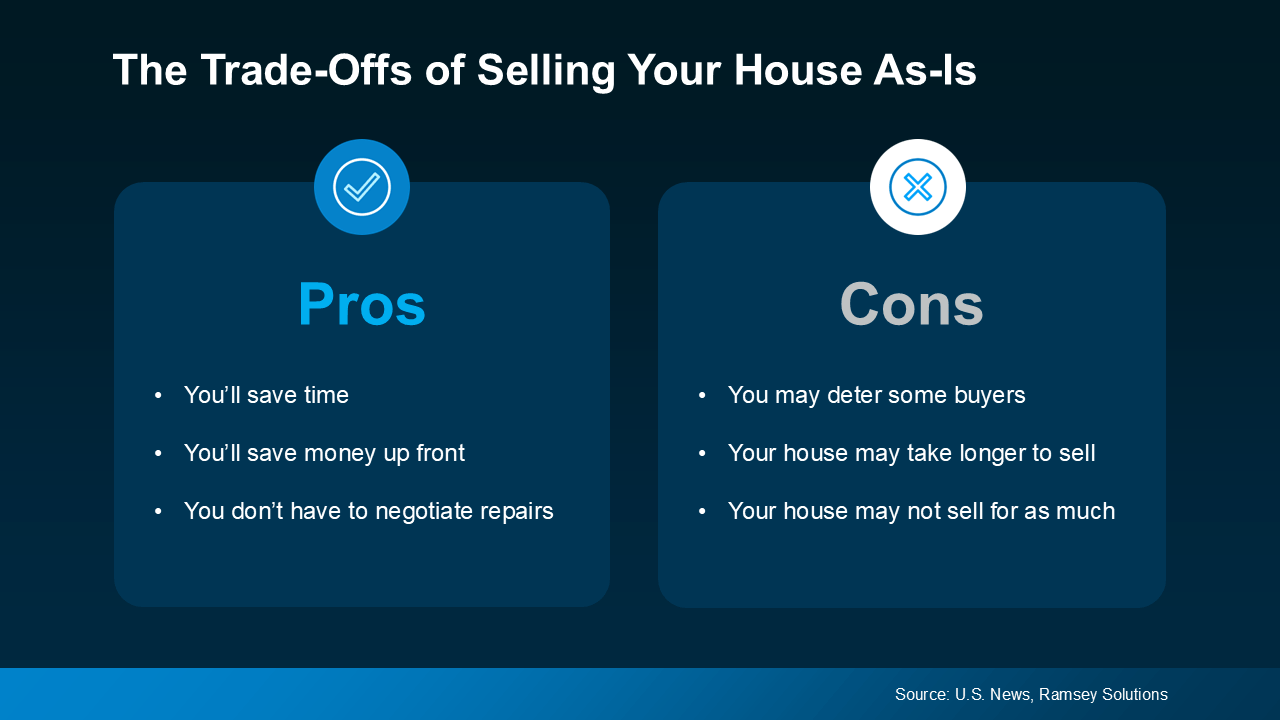

If you’re feeling stressed because you don’t have the time, budget, or resources to tackle any repairs or updates, you may be tempted to sell your house as-is, too. But before you decide to go this route, here’s what you need to know.

If you’re feeling stressed because you don’t have the time, budget, or resources to tackle any repairs or updates, you may be tempted to sell your house as-is, too. But before you decide to go this route, here’s what you need to know. Typically, a home that’s updated sells for more because buyers are often willing to pay a premium for something that’s move-in ready. That’s why you may find not as many buyers will look at your house if you sell it in its current condition. And less interest from buyers could mean fewer offers, taking longer to sell, and ultimately, a lower price. Basically, while it’s easier for you, the final sale price might be less than you’d get if you invested in repairs and upgrades.

Typically, a home that’s updated sells for more because buyers are often willing to pay a premium for something that’s move-in ready. That’s why you may find not as many buyers will look at your house if you sell it in its current condition. And less interest from buyers could mean fewer offers, taking longer to sell, and ultimately, a lower price. Basically, while it’s easier for you, the final sale price might be less than you’d get if you invested in repairs and upgrades.

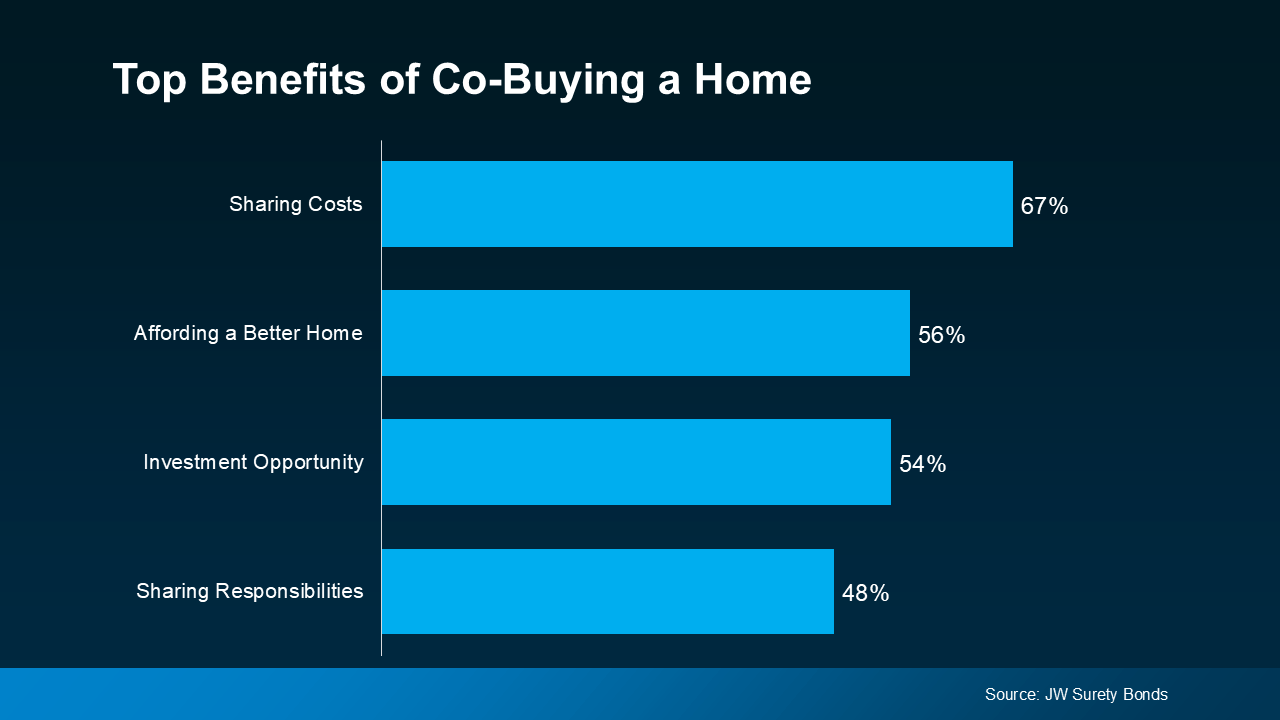

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

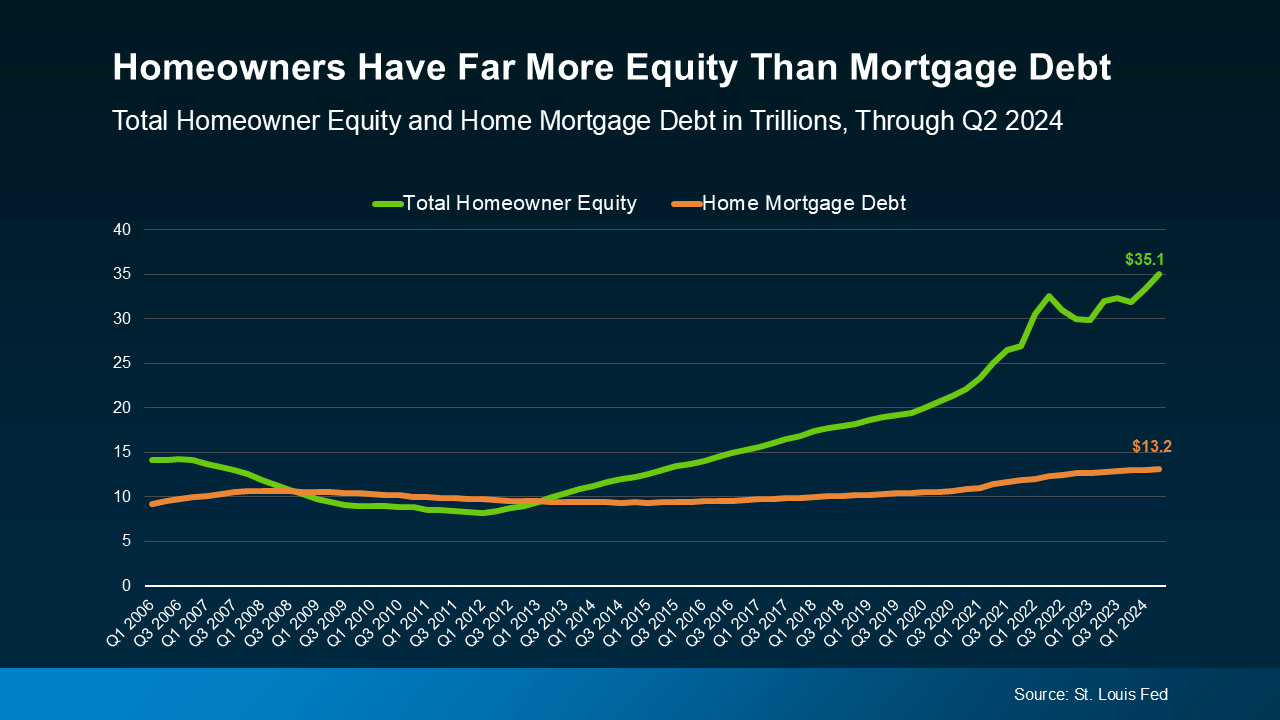

High equity makes it less likely for homeowners to face foreclosure because they have more options. If someone struggles to make their mortgage payments, they could potentially sell their house and still come out ahead thanks to their built-up equity.

High equity makes it less likely for homeowners to face foreclosure because they have more options. If someone struggles to make their mortgage payments, they could potentially sell their house and still come out ahead thanks to their built-up equity. This is partly due to a variety of programs designed to help homeowners through temporary hardships. As Marina Walsh, VP of Industry Analysis at the Mortgage Bankers Association (MBA), says:

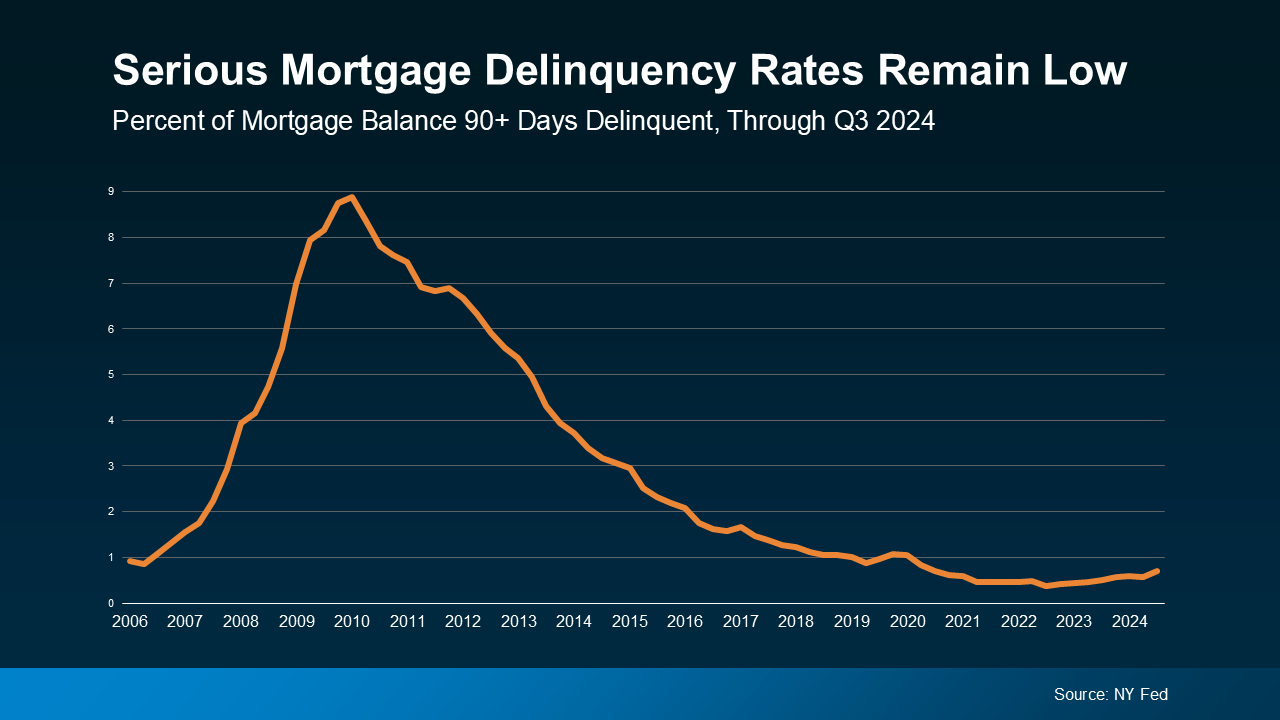

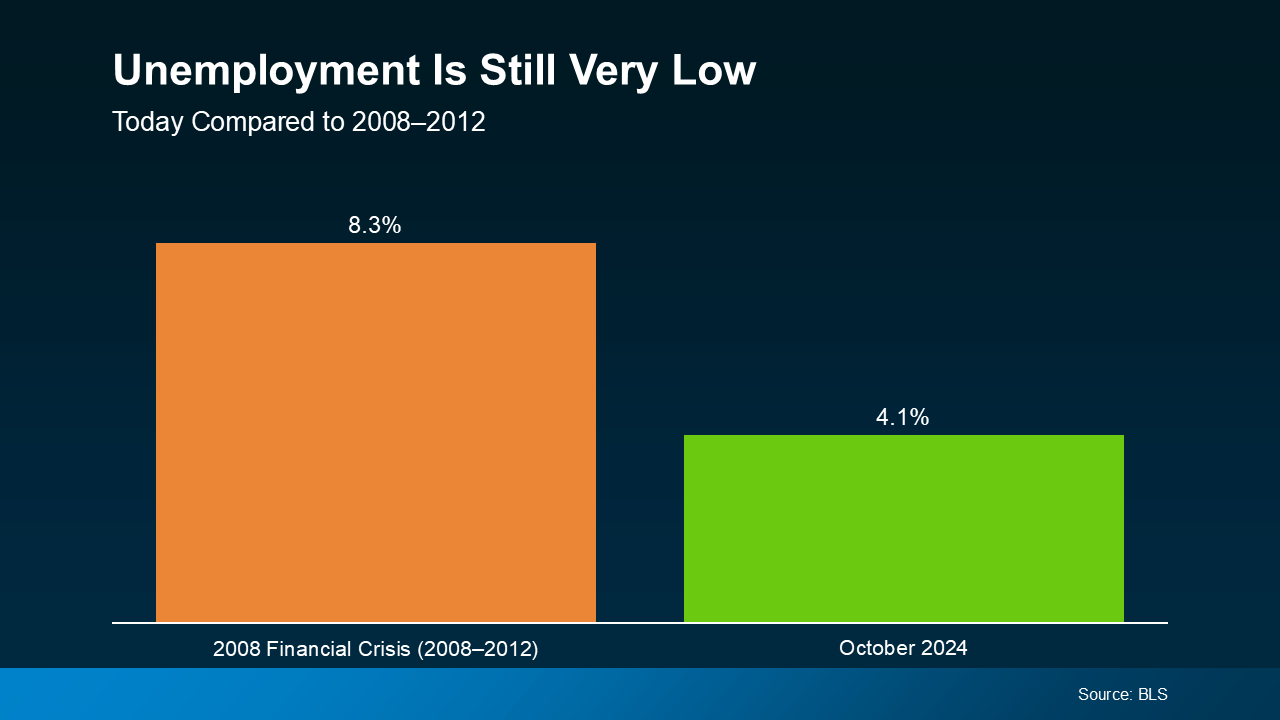

This is partly due to a variety of programs designed to help homeowners through temporary hardships. As Marina Walsh, VP of Industry Analysis at the Mortgage Bankers Association (MBA), says: That stability in how many people are employed is one of the reasons the market doesn’t have the same risks as it did the last time.

That stability in how many people are employed is one of the reasons the market doesn’t have the same risks as it did the last time.

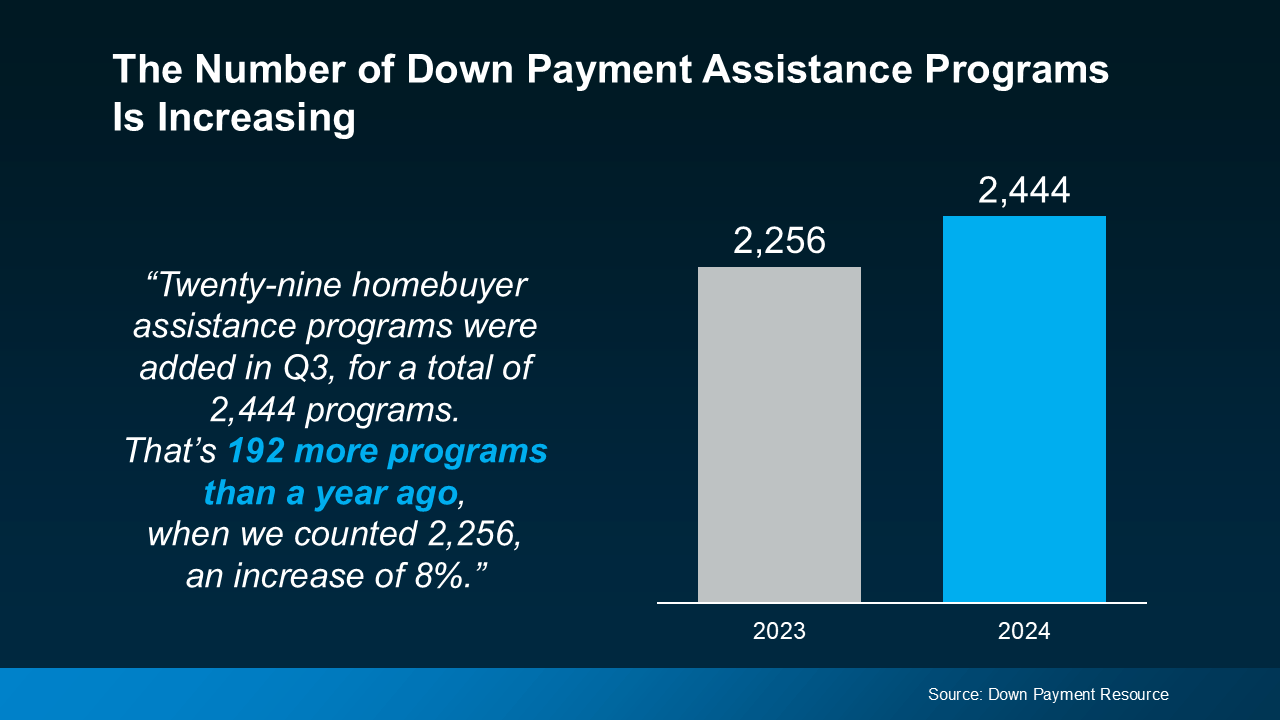

More Programs, More Opportunities for You

More Programs, More Opportunities for You