![Home Price Forecasts Revised for 2023 [INFOGRAPHIC] Simplifying The Market](https://terceroagency.com/wp-content/uploads/2023/09/Home-Price-Forecasts-Revised-for-2023-KCM-Share.png)

Some Highlights

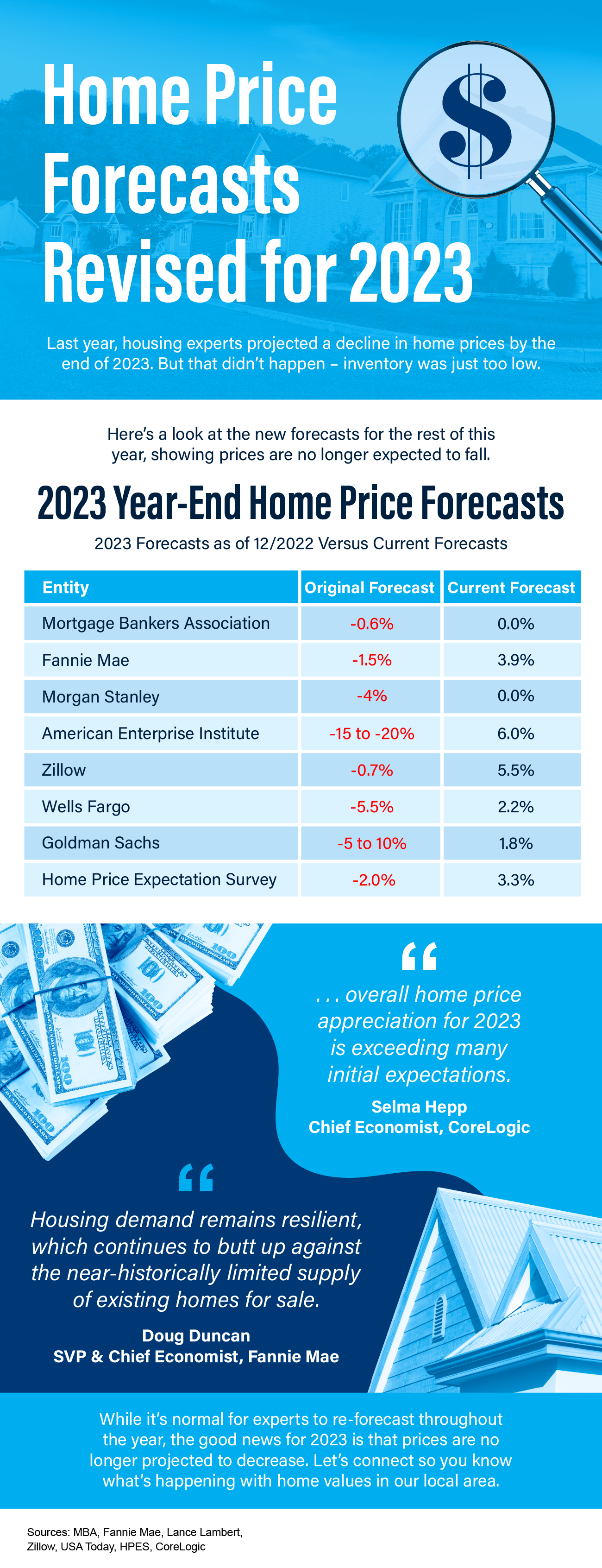

- Last year, some housing experts projected a decline in home prices by the end of 2023. But that didn’t happen – inventory was just too low.

- While it’s normal for experts to re-forecast throughout the year, the good news for 2023 is that prices are no longer projected to decrease.

- Connect with your trusted real estate agent to find out what’s happening with home values in your local area.

Sources

- https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/mortgage-finance-forecast-dec-2022.pdf

- https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/2023/mortgage-finance-forecast-aug-2023.pdf

- https://www.fanniemae.com/media/45801/display

- https://www.fanniemae.com/media/48726/display

- https://twitter.com/NewsLambert/status/1671900591113609216 (Morgan Stanley)

- https://twitter.com/NewsLambert/status/1671556169712672768 (AEI)

- https://www.zillow.com/research/data/

- https://www.zillow.com/research/housing-market-challenges-32923/

- https://ustoday.news/a-20-drop-in-house-prices-7-forecast-models-tend-to-crash-here-the-other-13-models-show-the-housing-market-in-2023/ (Wells Fargo)

- https://twitter.com/NewsLambert/status/1686959362563092480 (Wells Fargo)

- https://twitter.com/NewsLambert/status/1691799764466008217 (Goldman Sachs)

- https://pulsenomics.com/surveys/#home-price-expectations

- https://www.corelogic.com/intelligence/us-corelogic-sp-case-shiller-index-down-by-0-5-year-over-year-in-may-but-a-turning-point-may-be-ahead/

- https://view.e.fanniemae.com/?qs=dd7a875aaf273bf9cc0d451ff7cd4bec791f29b000f7916b3935d94770ed1f009af1072ee8400b8d3d40310113be33e6106c9aea71d7b22fbb87ad26bbcfe90630f1ef8f04bd2f7b7576e1b494263bf85f1ae4e4ba224216

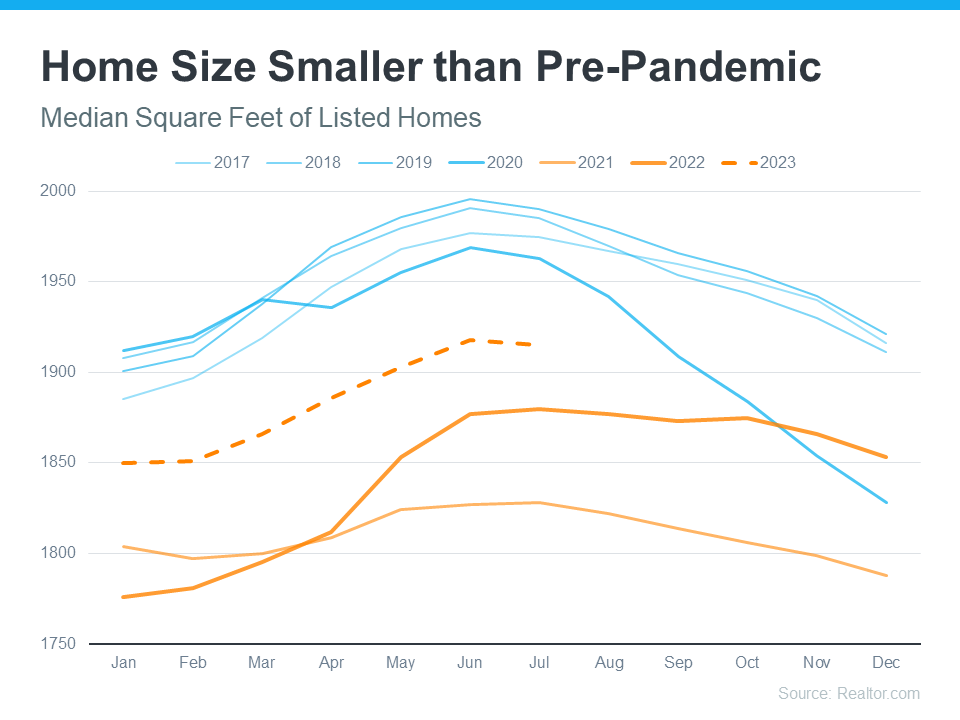

This graph also shows how the size of homes on the market changes seasonally. Larger homes tend to come on the market during the summer months when households with children who are out of school are looking to move.

This graph also shows how the size of homes on the market changes seasonally. Larger homes tend to come on the market during the summer months when households with children who are out of school are looking to move.

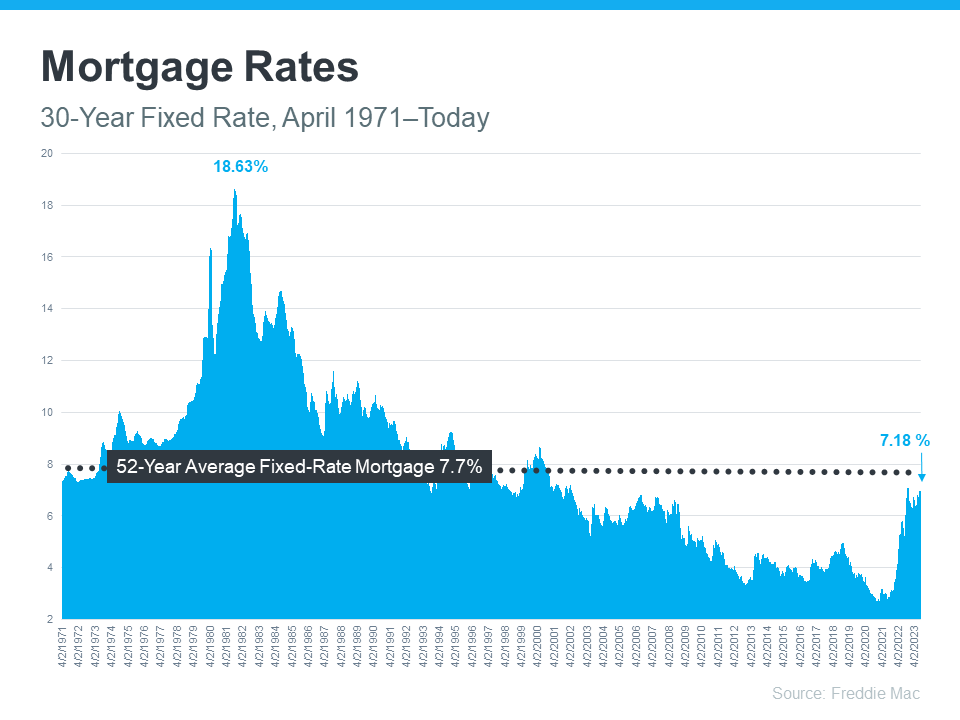

Looking at the right side of the graph, mortgage rates have increased significantly since the start of last year. But even with that rise, today’s rates are still below the 52-year average. While that historical perspective is good context, buyers have gotten used to mortgage rates between 3% and 5%, which is where they’ve been over the past 15 years.

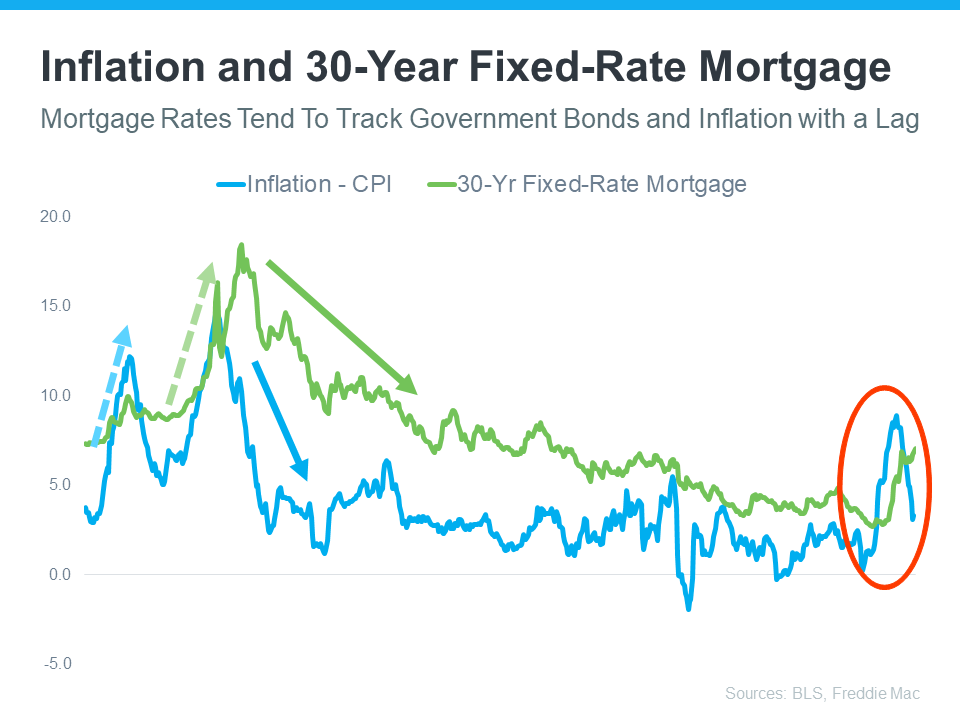

Looking at the right side of the graph, mortgage rates have increased significantly since the start of last year. But even with that rise, today’s rates are still below the 52-year average. While that historical perspective is good context, buyers have gotten used to mortgage rates between 3% and 5%, which is where they’ve been over the past 15 years. This graph shows a pretty reliable relationship between inflation and mortgage rates. Looking at the left side of the graph, each time inflation moves significantly (shown in blue), mortgage rates follow suit shortly after (shown in green).

This graph shows a pretty reliable relationship between inflation and mortgage rates. Looking at the left side of the graph, each time inflation moves significantly (shown in blue), mortgage rates follow suit shortly after (shown in green).

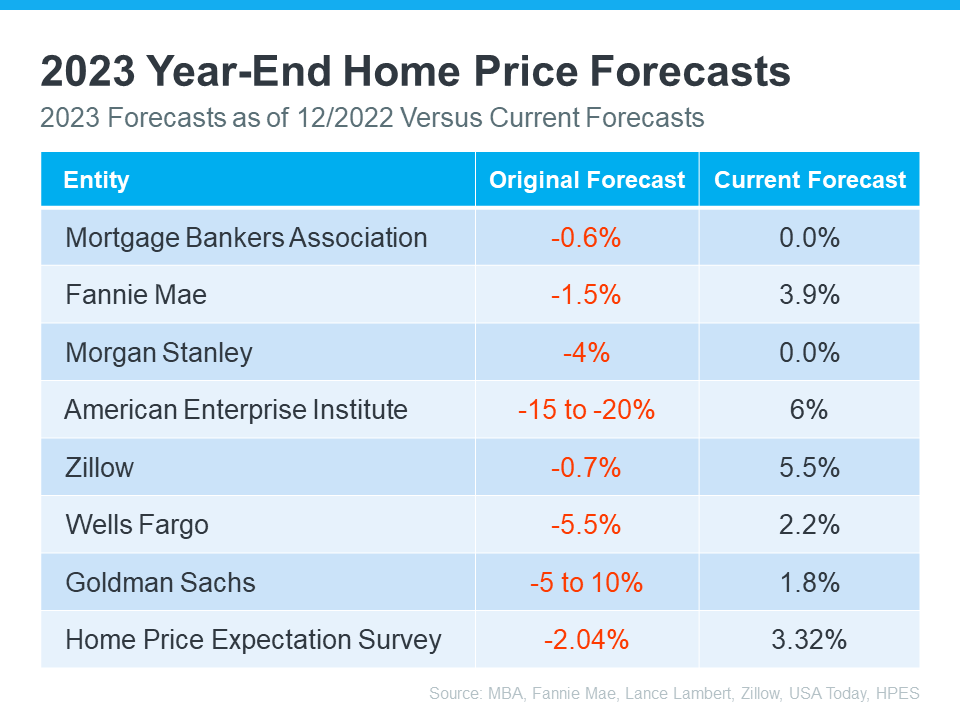

As the red in the middle column shows, in all instances, their original forecast called for home prices to fall. But, if you look at the right column, you’ll see all experts have updated their projections for the year-end to show they expect prices to either be flat or have positive growth. That’s a significant change from the original negative numbers.

As the red in the middle column shows, in all instances, their original forecast called for home prices to fall. But, if you look at the right column, you’ll see all experts have updated their projections for the year-end to show they expect prices to either be flat or have positive growth. That’s a significant change from the original negative numbers.

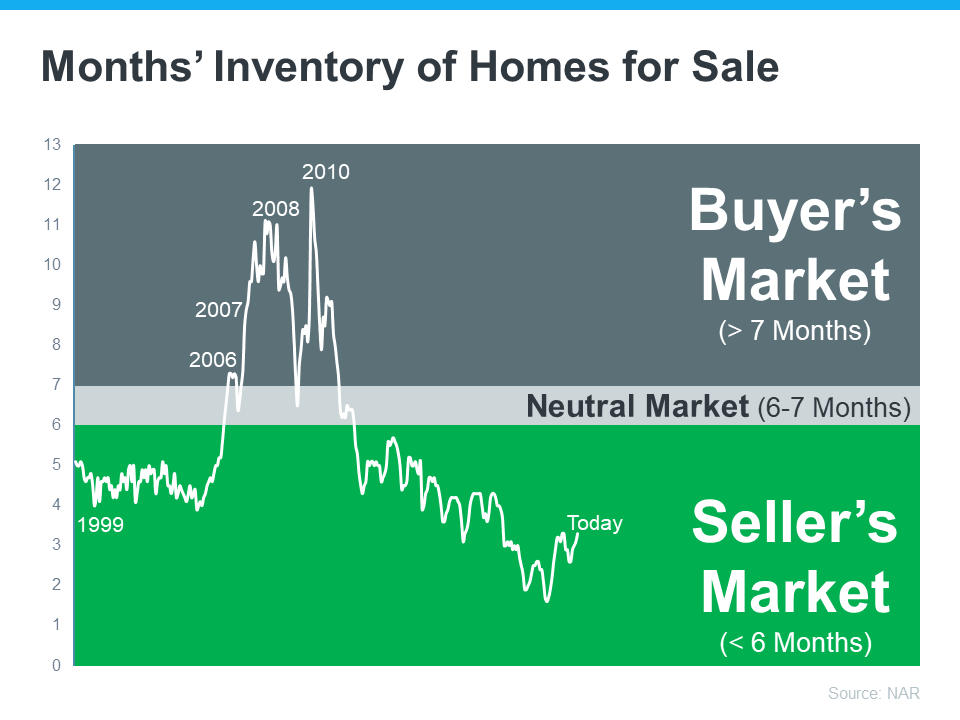

As the visual shows, given the current inventory of homes, it’s still a seller's market.

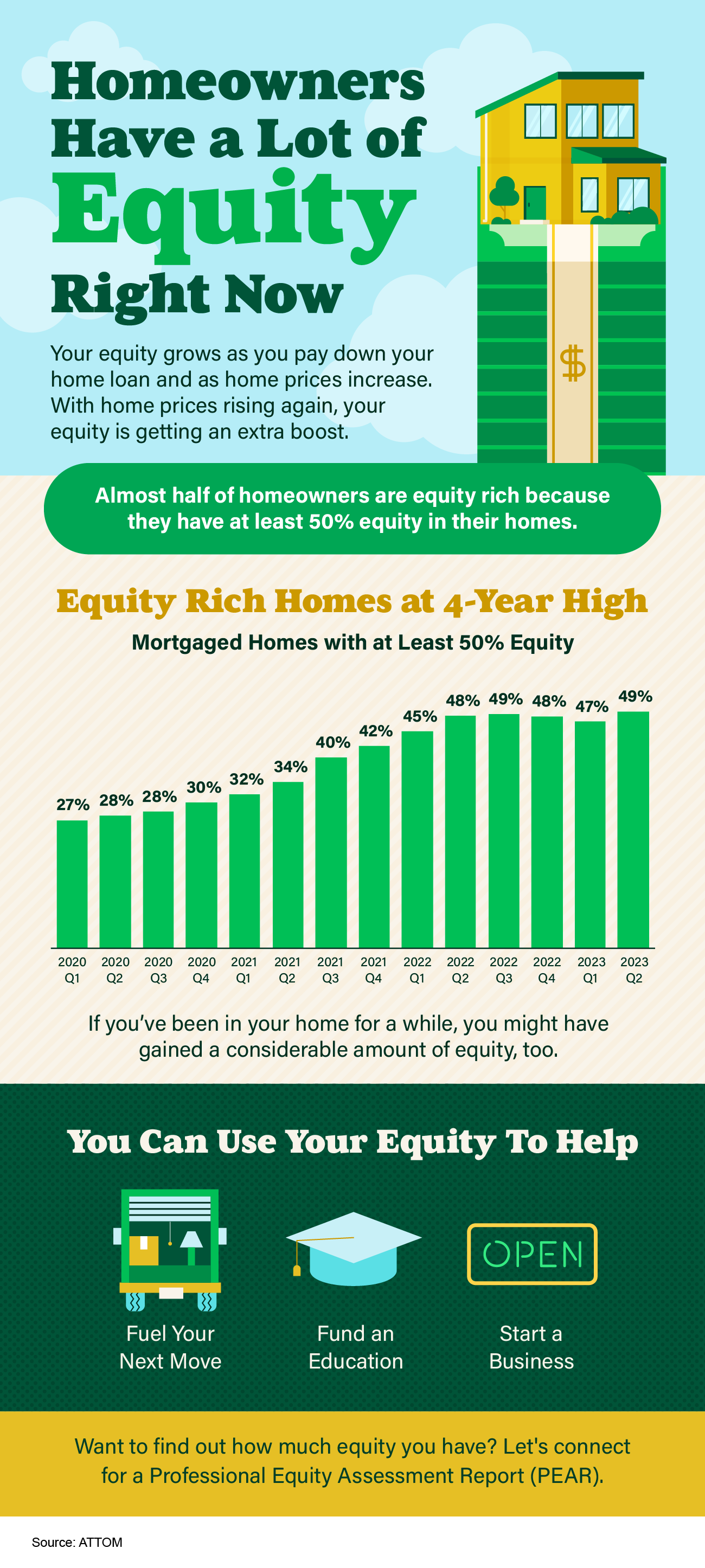

As the visual shows, given the current inventory of homes, it’s still a seller's market.![Homeowners Have a Lot of Equity Right Now [INFOGRAPHIC] Simplifying The Market](https://terceroagency.com/wp-content/uploads/2023/09/20230901-Homeowners-Have-a-Lot-of-Equity-Right-Now-KCM-Share.png)

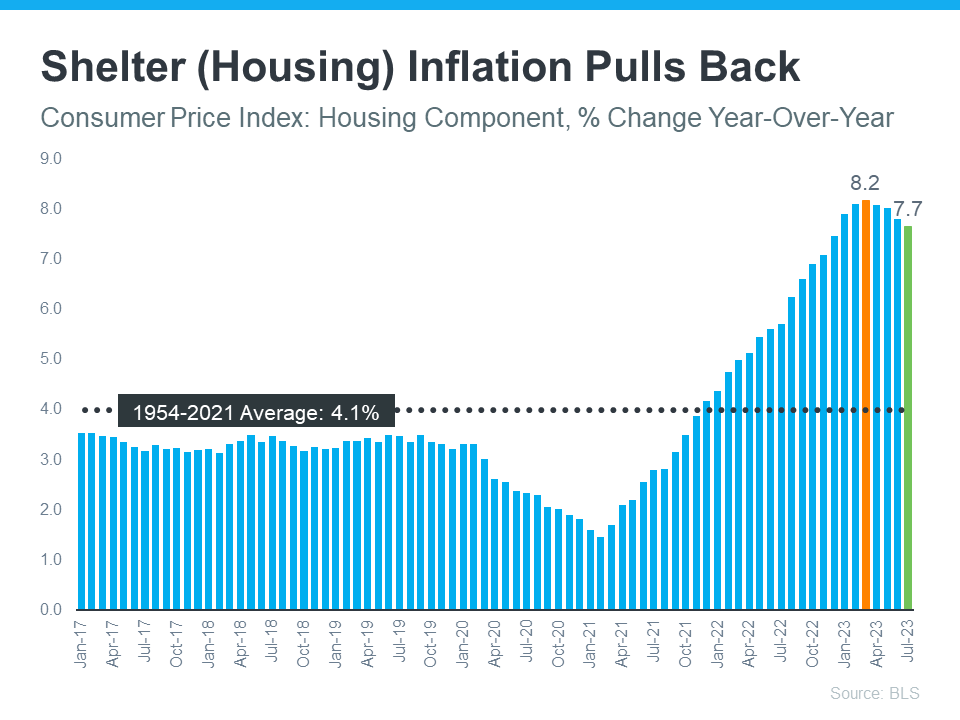

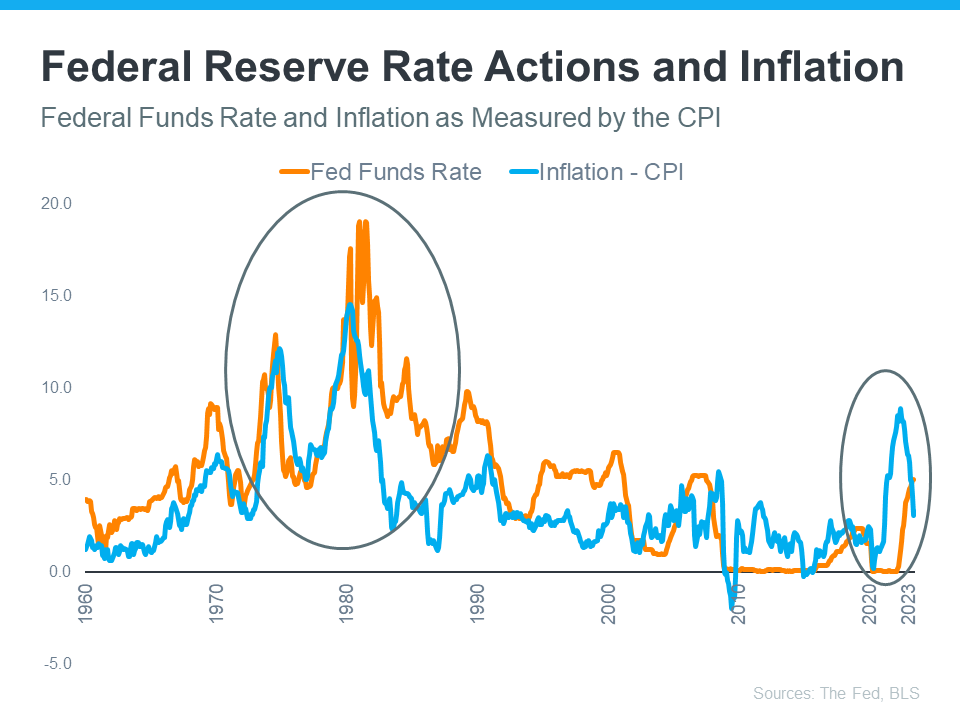

Why does this matter? Well, shelter inflation makes up about one-third of overall inflation, as measured by the Consumer Price Index (CPI). So, when shelter inflation moves, it leads to noticeable moves in overall inflation. That means the recent dip in shelter inflation might be a sign that overall inflation could fall in the months ahead.

Why does this matter? Well, shelter inflation makes up about one-third of overall inflation, as measured by the Consumer Price Index (CPI). So, when shelter inflation moves, it leads to noticeable moves in overall inflation. That means the recent dip in shelter inflation might be a sign that overall inflation could fall in the months ahead. The circled portion of the graph shows the most recent spike in inflation, the Fed’s actions to raise the Federal Funds Rate to fight that, and the moderation of inflation that happened in response to that hike. As inflation gets closer to the Fed’s current 2% goal, they may not need to raise the Federal Funds Rate much further.

The circled portion of the graph shows the most recent spike in inflation, the Fed’s actions to raise the Federal Funds Rate to fight that, and the moderation of inflation that happened in response to that hike. As inflation gets closer to the Fed’s current 2% goal, they may not need to raise the Federal Funds Rate much further.

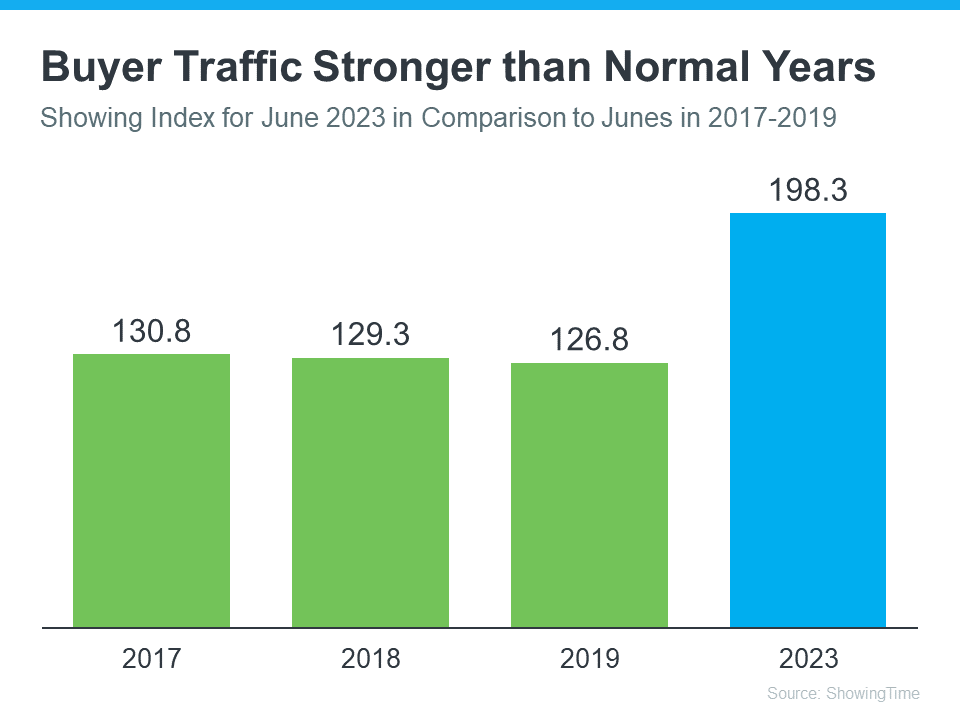

As you can see, when June 2023 numbers are stacked alongside what’s typical for the housing market at this time of year, it's clear buyers are still active. And, they’re actually a lot more active than the norm.

As you can see, when June 2023 numbers are stacked alongside what’s typical for the housing market at this time of year, it's clear buyers are still active. And, they’re actually a lot more active than the norm.