If you’re a first-time homebuyer, you might feel like the odds are stacked against you in today’s market. But there are resources and programs out there that can help – if you know where to look. And one thing that can make homeownership easier to achieve? An FHA home loan.

They’re designed to help you overcome some of the biggest financial hurdles in the homebuying process – and that’s why so many first-timers are using them to make their purchase.

Whether you’re dreaming of ditching rent, planting roots, or just wanting a place that’s truly yours, an FHA home loan could be the path that gets you there sooner than you think.

Buying Your First Home Probably Doesn’t Feel Easy Right Now

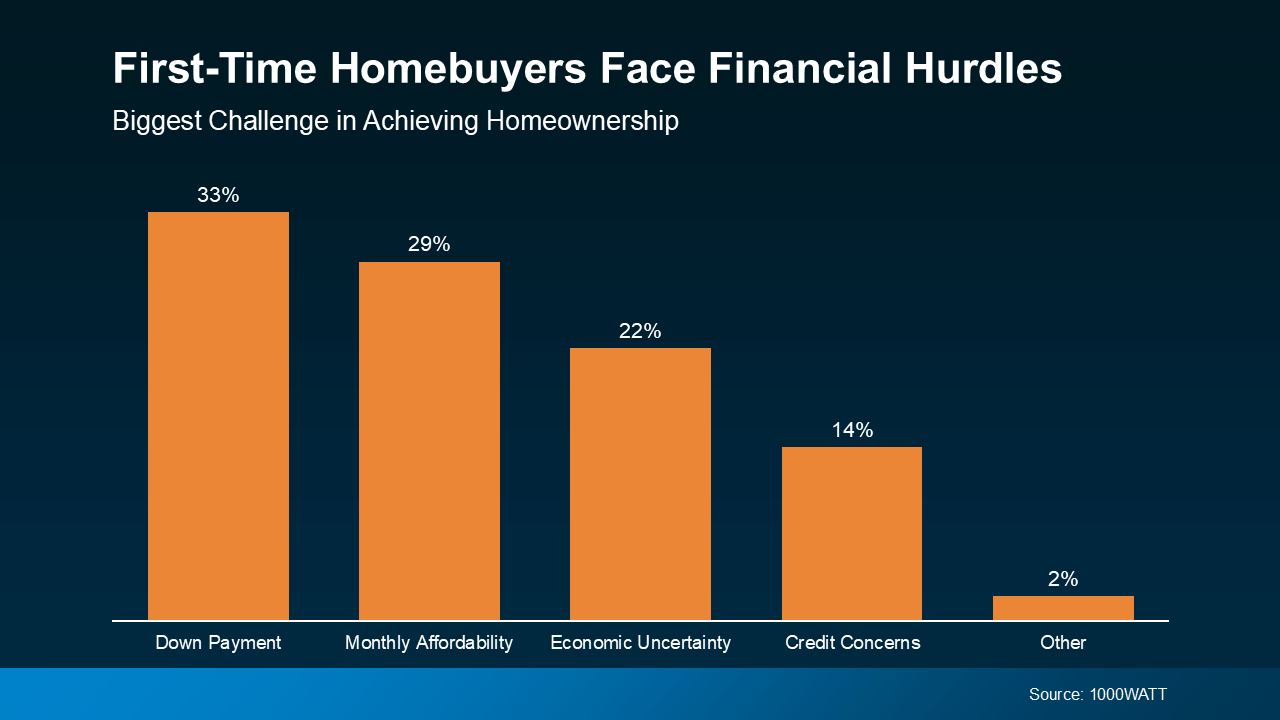

While the motivation to buy a home is still there for many people, affordability is a real challenge today. According to a survey from 1000WATT, potential first-time buyers say their top two concerns are saving enough for their down payment and making the monthly mortgage payments work at today’s home prices and mortgage rates (see graph below):

That’s Where FHA Loans Come In

That’s Where FHA Loans Come In

FHA loans help many first-time buyers overcome these challenges.

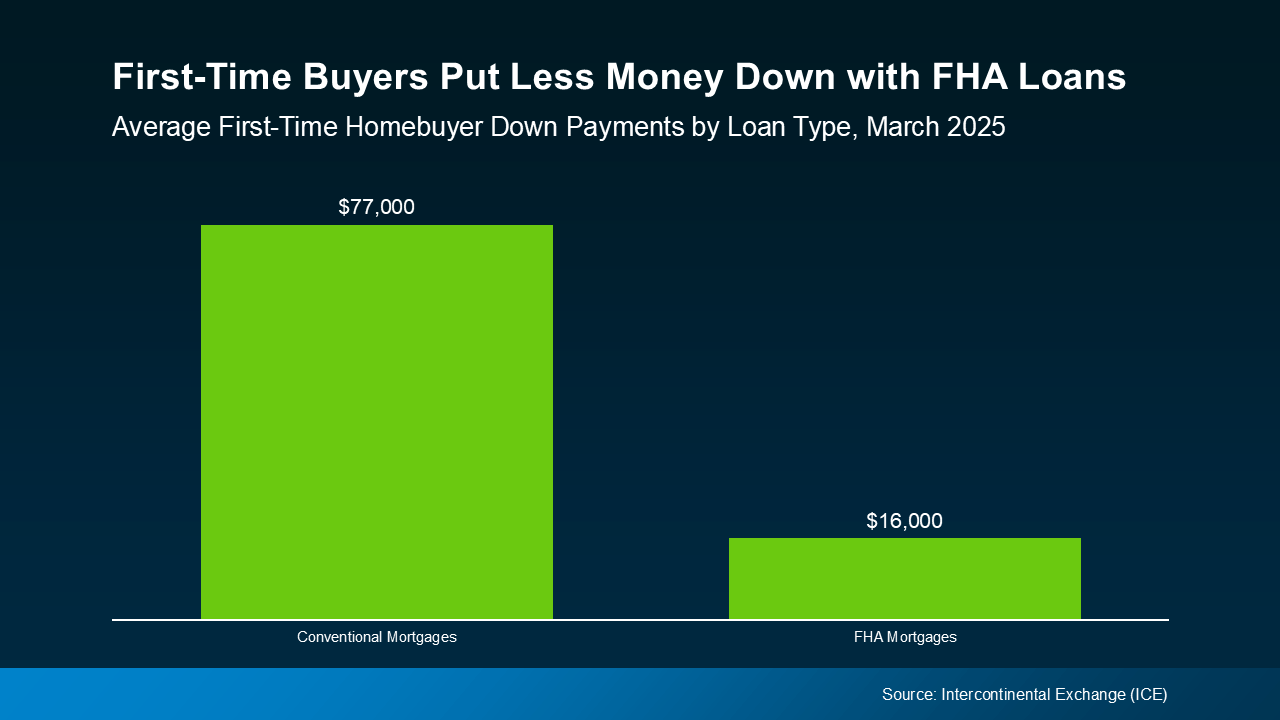

In fact, according to Intercontinental Exchange (ICE), the average first-time buyer using an FHA loan puts down just $16,000. That’s a big difference from the $77,000 they’re putting down with the typical conventional mortgage (see graph below):

Essentially, buyers who use an FHA loan may not have to come up with as much cash up front. But the perks don’t stop there. You may also be able to pay less monthly, too.

Essentially, buyers who use an FHA loan may not have to come up with as much cash up front. But the perks don’t stop there. You may also be able to pay less monthly, too.

That’s because, a lot of the time, the mortgage rate on FHA loans can be lower. Bankrate says:

“FHA loan rates are competitive with, and often slightly lower than, rates for conventional loans.”

So, if you’re thinking about buying your first place, an FHA loan may be worth exploring.

Because of the potential for lower down payment requirements and maybe even a lower mortgage rate, it could help with the two most common hurdles first-time buyers face today – saving enough money upfront and affording the monthly payment.

A trusted lender can walk you through the details, compare your options, and help you figure out what loan type makes the most sense for your situation.

Bottom Line

With the right loan and the right guidance, homeownership may be more achievable than you think.

Do you want to talk more about your options? A trusted lender is there to help.

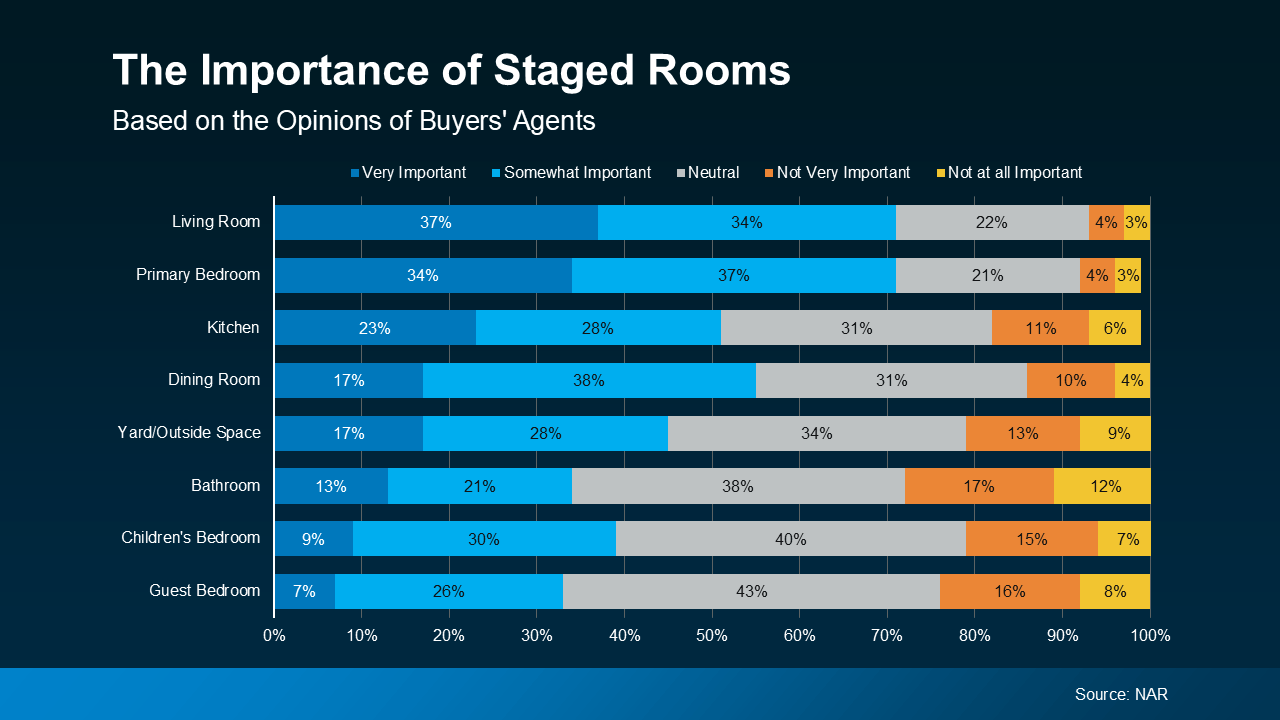

As you can see, agents who talk to buyers regularly agree, the most important spaces to stage are the rooms where buyers will spend the most time, like the living room, primary bedroom, and kitchen.

As you can see, agents who talk to buyers regularly agree, the most important spaces to stage are the rooms where buyers will spend the most time, like the living room, primary bedroom, and kitchen.

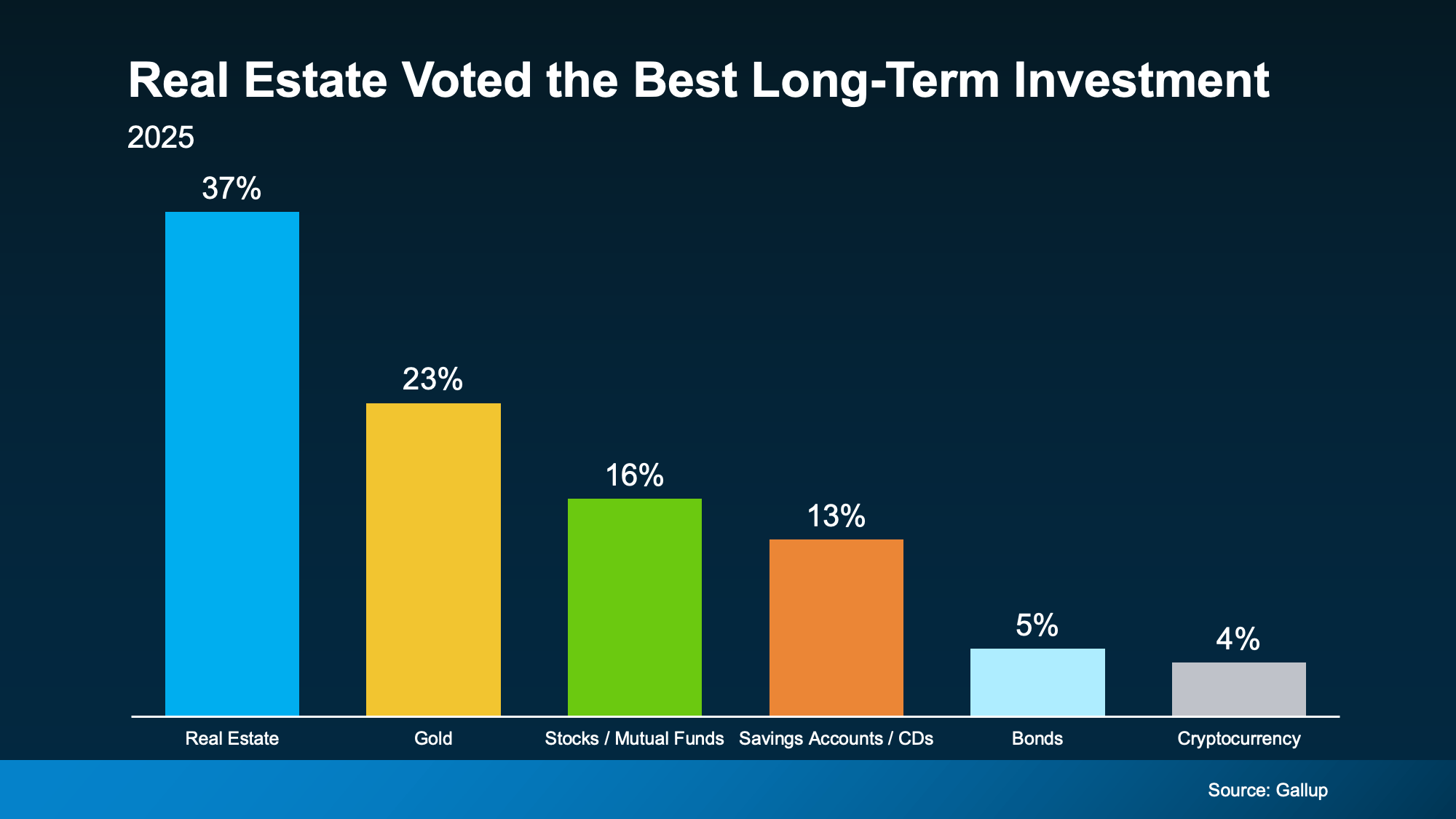

And this isn’t new. Real estate usually claims the #1 title. But here’s what’s really interesting. This year’s results came in just after a rocky April for the stock and bond markets. It shows that, even as other investments had wild swings, real estate has held its ground. That’s likely because it gains value in a steadier, more predictable way. As Gallup explains:

And this isn’t new. Real estate usually claims the #1 title. But here’s what’s really interesting. This year’s results came in just after a rocky April for the stock and bond markets. It shows that, even as other investments had wild swings, real estate has held its ground. That’s likely because it gains value in a steadier, more predictable way. As Gallup explains:

You read that right. That brand new, never-been-lived-in house may cost less than the one built 20 years ago in a neighborhood just down the street. So, if you wrote off a new build because you assumed they’d be financially out of reach, here’s what you should know. You could be missing out on some of the best options in today’s housing market.

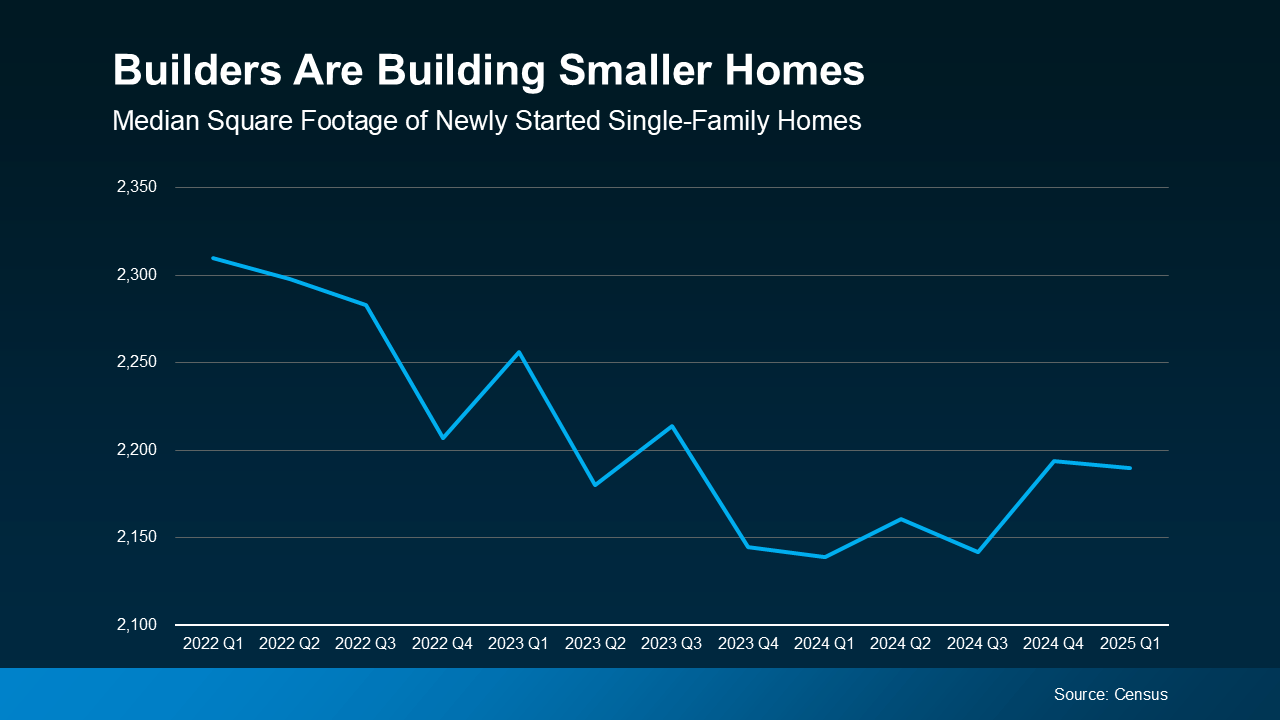

You read that right. That brand new, never-been-lived-in house may cost less than the one built 20 years ago in a neighborhood just down the street. So, if you wrote off a new build because you assumed they’d be financially out of reach, here’s what you should know. You could be missing out on some of the best options in today’s housing market. And as size goes down, the price often does too. Smaller homes use fewer materials, which makes them less expensive to build. That helps builders keep prices lower so more people can afford them.

And as size goes down, the price often does too. Smaller homes use fewer materials, which makes them less expensive to build. That helps builders keep prices lower so more people can afford them.

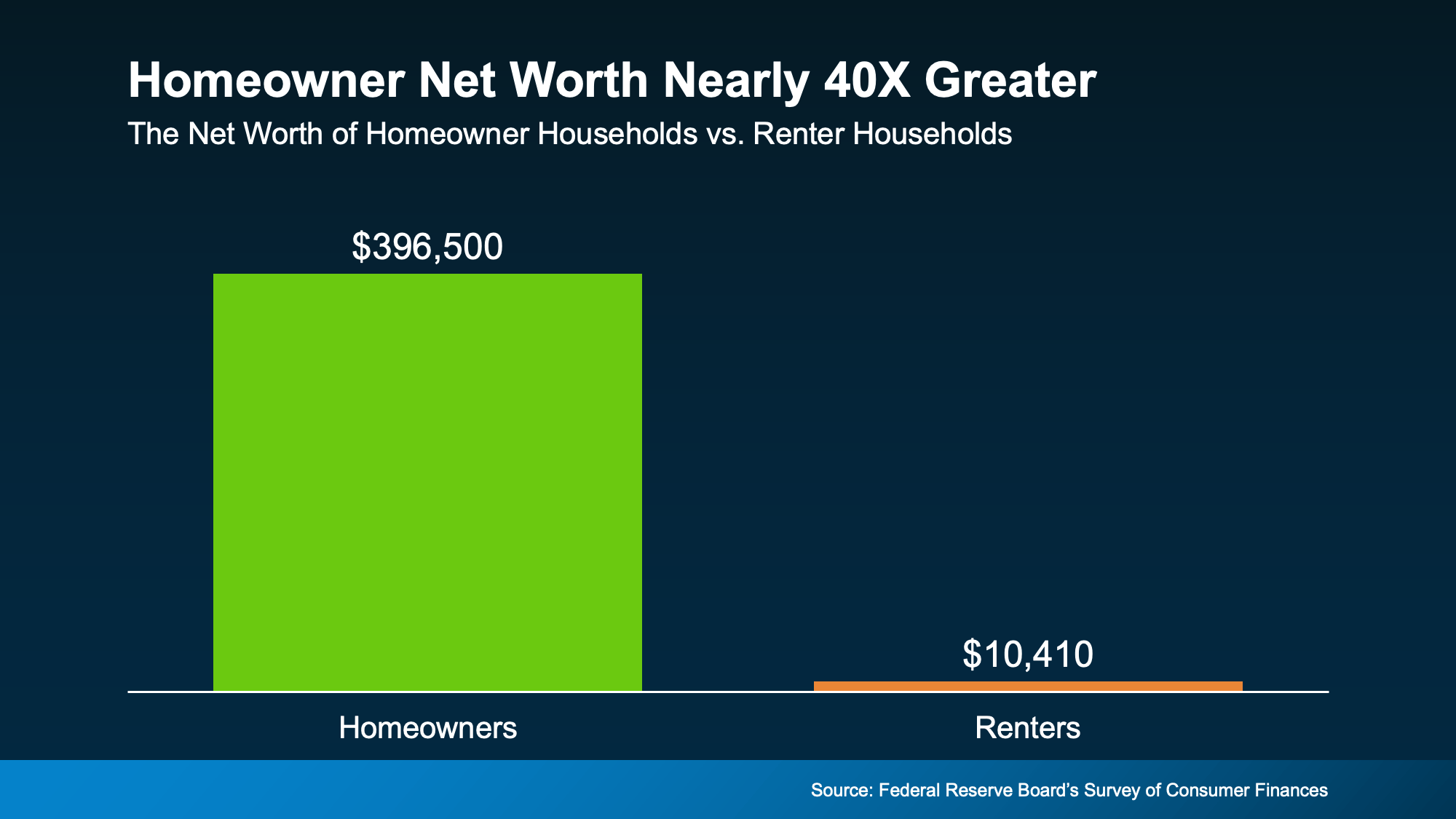

And as home values rise, so does your equity when you’re a homeowner. That’s the difference between what your home is worth and what you owe. So, with every mortgage payment, that equity grows. Over time, that becomes part of your net worth.

And as home values rise, so does your equity when you’re a homeowner. That’s the difference between what your home is worth and what you owe. So, with every mortgage payment, that equity grows. Over time, that becomes part of your net worth. And it’s one of the big reasons why Forbes says:

And it’s one of the big reasons why Forbes says: That kind of financial uncertainty has a real impact. In the same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances.

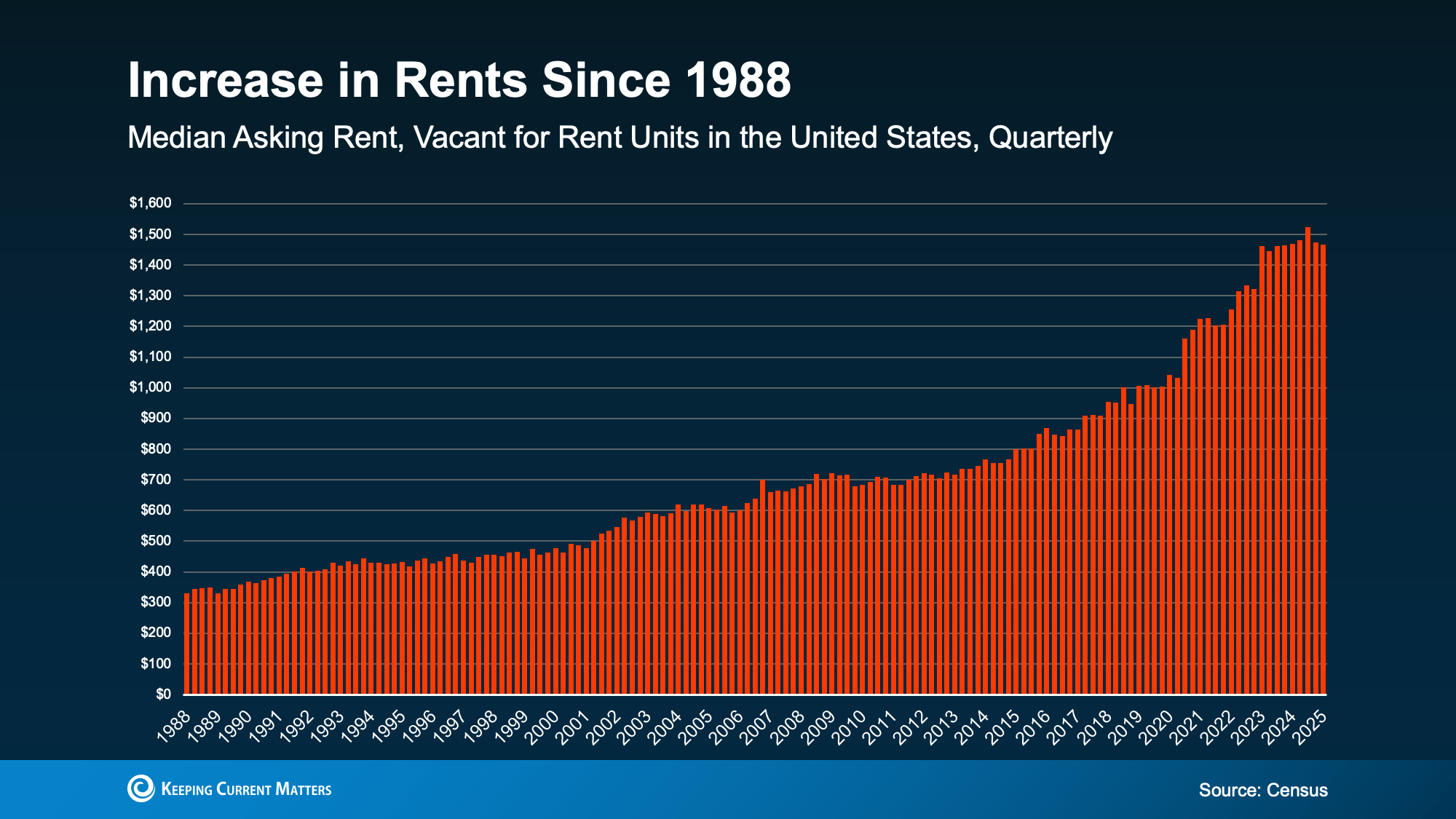

That kind of financial uncertainty has a real impact. In the same Bank of America survey, 72% of potential buyers said they worry rising rent could affect their current and long-term finances.

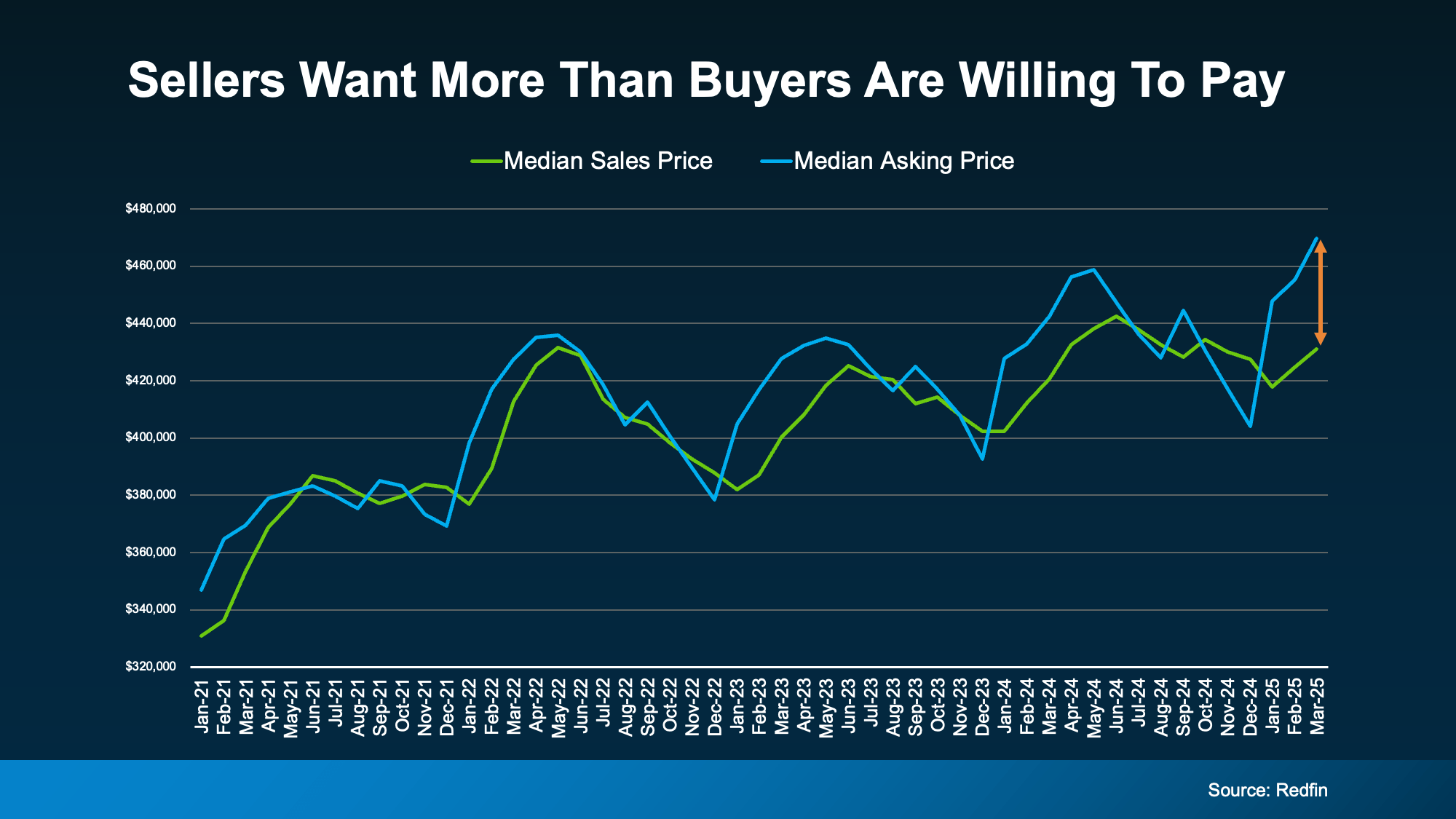

This tells you something important: not all buyers are willing to pay what many sellers are asking. That doesn’t mean you can’t sell for a great price – but it does mean you need to start with a price that reflects what people are willing to pay in today’s market.

This tells you something important: not all buyers are willing to pay what many sellers are asking. That doesn’t mean you can’t sell for a great price – but it does mean you need to start with a price that reflects what people are willing to pay in today’s market.

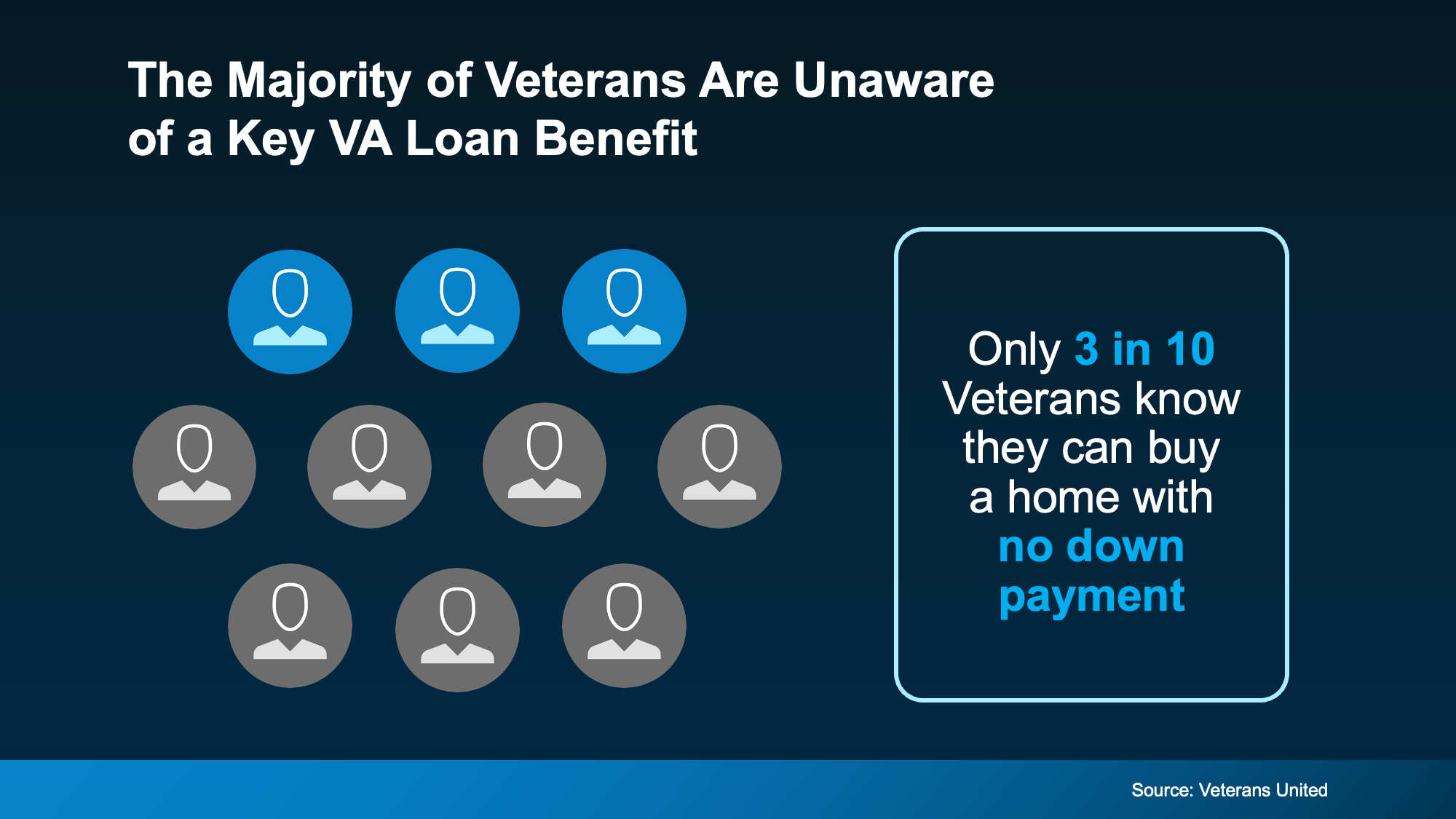

That means 7 out of every 10 Veterans could be missing out on a key homebuying advantage.

That means 7 out of every 10 Veterans could be missing out on a key homebuying advantage.