If you’re a homeowner, chances are you’ve built up a lot of wealth – just by living in your house and watching its value grow over time. And that equity? It’s something that could help change your child’s life.

Since affordability is still a challenge, a lot of first-time buyers are struggling to buy a home in today’s market. Even if they have a stable job and a solid plan, buying can still feel out of reach. But that’s where your equity could make all the difference.

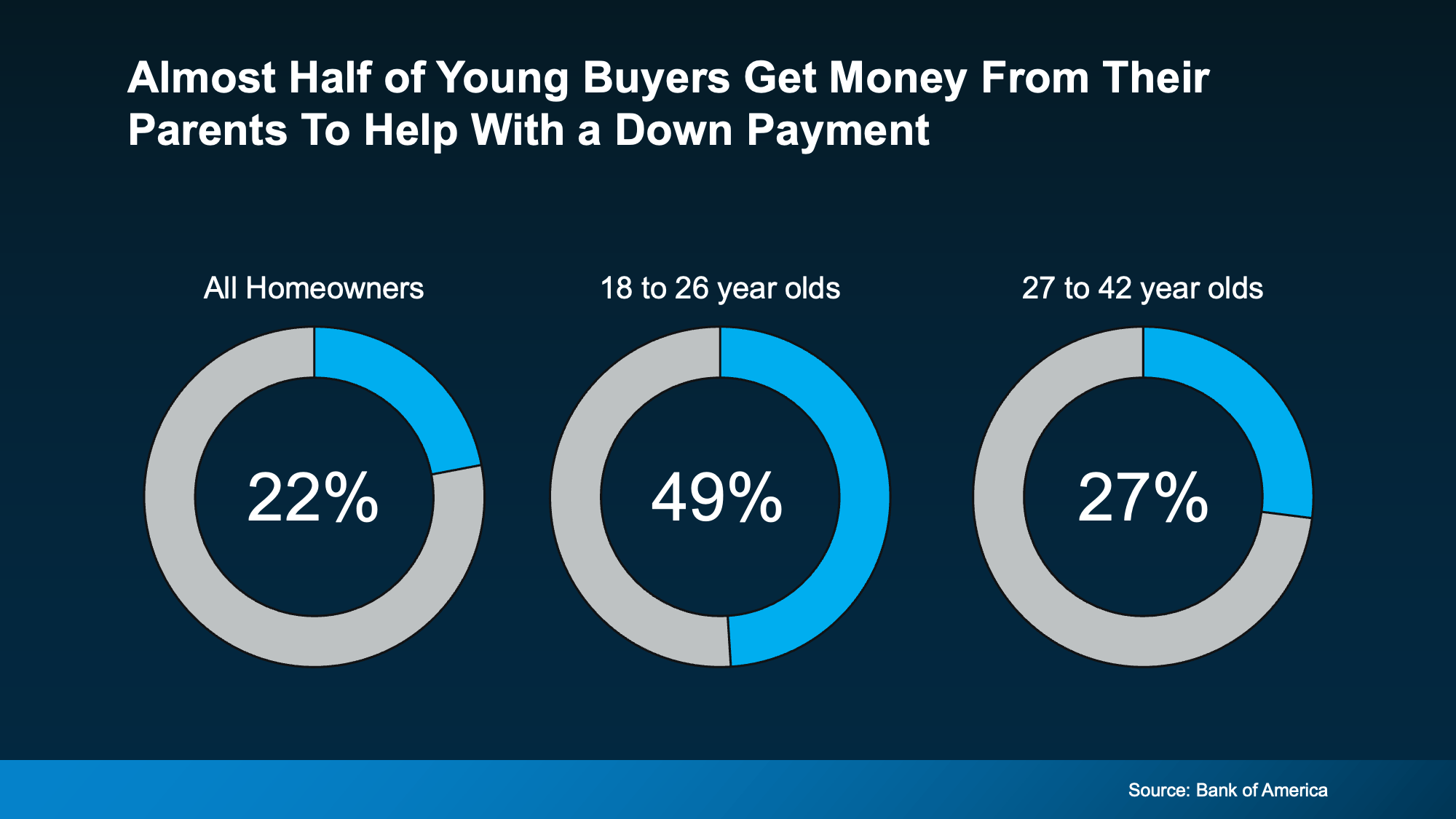

To give you an idea, the average homeowner with a mortgage has $311,000 worth of equity, according to Cotality (formerly CoreLogic). That’s significant. And some parents are using a portion of their equity to help their children become homeowners, too.

According to Bank of America, 49% of buyers between 18 and 26 got money from their parents to use toward their down payment (see chart below):

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

Even though the data doesn’t specify how many parents used their equity, the wealth they’ve built through homeownership may have helped make it possible – especially given how much equity the average homeowner has today.

While what’s right for each person’s specific situation will vary on a case-by-case basis, that’s a powerful legacy to pass on. It helps those younger people buy a home, build equity of their own, and begin the next chapter of their life with a little less financial stress and a lot more stability. And for those parents? It’s a way to turn what they've built into something deeply meaningful.

This isn’t just about money. For many homeowners, it’s about being the reason their child gets to say, “we got the house.” And giving them the kind of head start they might’ve only dreamed of at their age. And here’s the part that really sticks. Compare the Market says:

“Of those who did receive monetary aid from parents and grandparents to buy a house, 45% of Americans said they would not have been able to purchase a house without financial support from parents and grandparents.”

Bottom Line

Your equity could be the thing that makes homeownership possible for your children when they might not be able to do it on their own. So, here’s the question.

If helping your kids buy a home was more feasible than you thought, would you want to explore that option?

If you want to learn more or find out the best way to make it happen, talk to your lender and a financial advisor you trust.

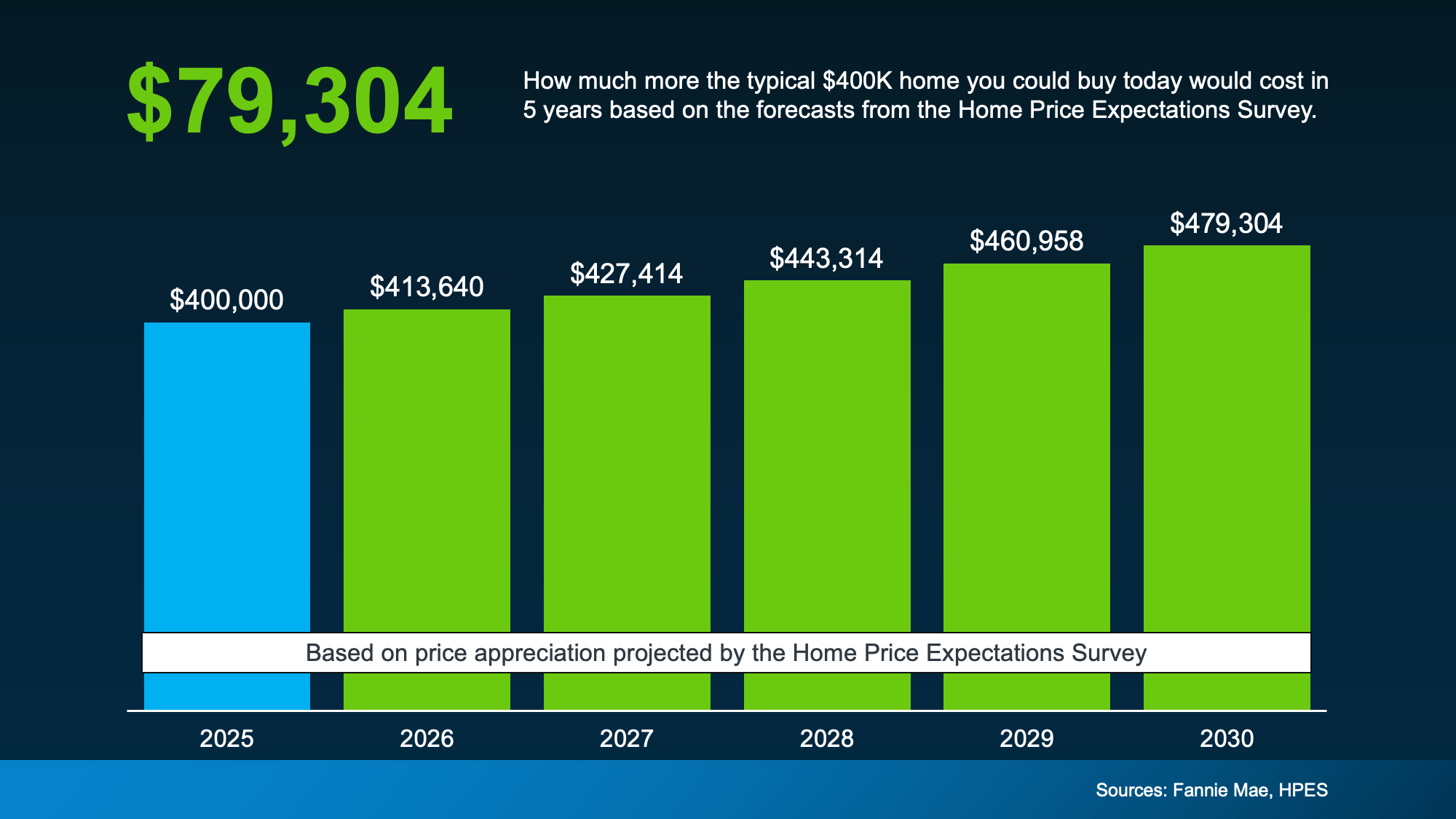

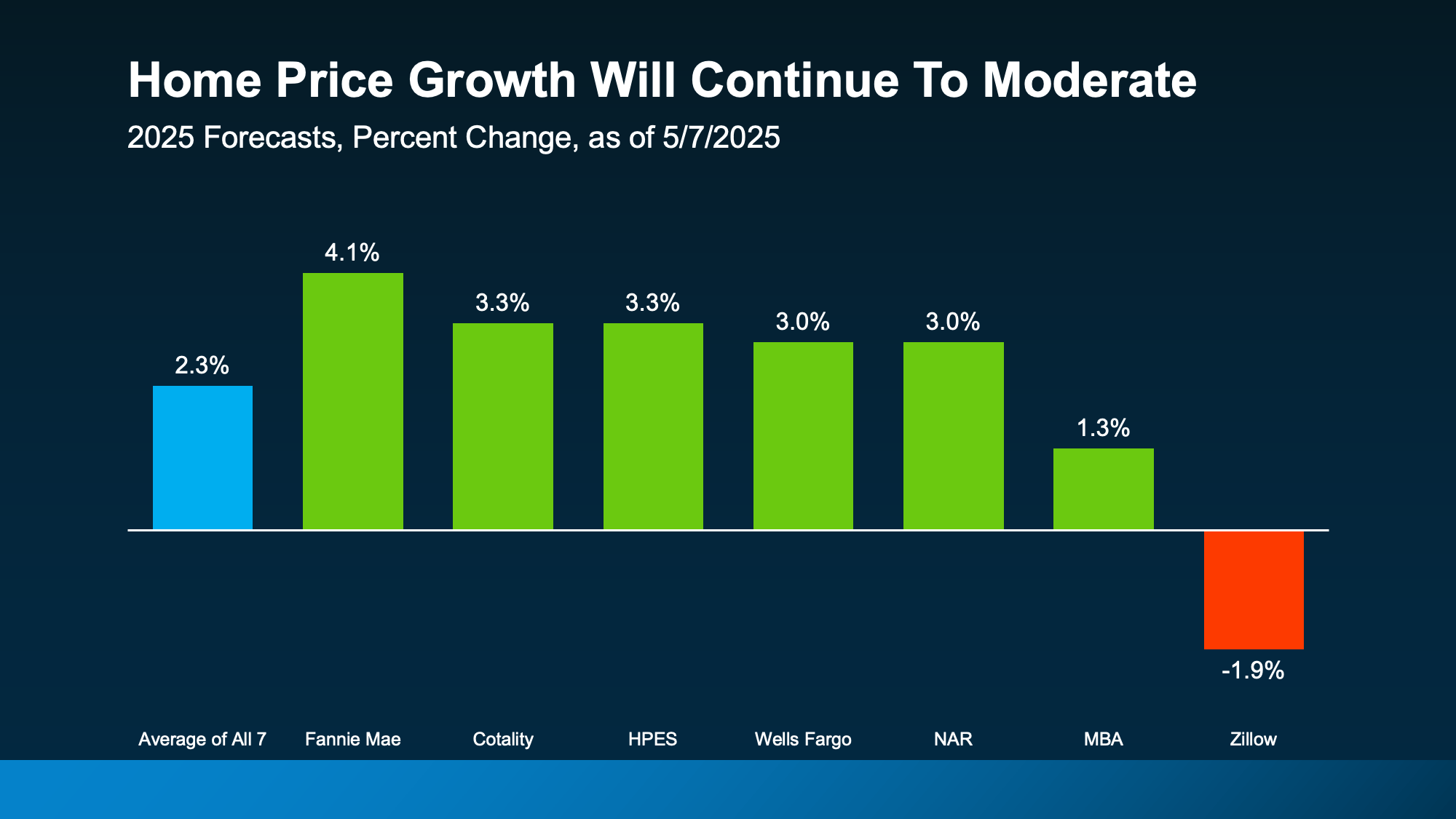

While those projections aren’t calling for big increases each year, it's still an increase. And sure, some markets may see flatter prices or slower growth, or even slight dips in the short term. But look further out. In the long run, prices almost always rise. And over the next 5 years, the anticipated increase – however slight – will add up fast.

While those projections aren’t calling for big increases each year, it's still an increase. And sure, some markets may see flatter prices or slower growth, or even slight dips in the short term. But look further out. In the long run, prices almost always rise. And over the next 5 years, the anticipated increase – however slight – will add up fast. That means the longer you wait, the more your future home will cost you.

That means the longer you wait, the more your future home will cost you.  So, the question really isn’t: “why would I move?” It’s: “when should I?” – because when you see the real numbers, waiting may not be the savings strategy you thought it was. And that’s the best conversation you can have with your trusted agent right now.

So, the question really isn’t: “why would I move?” It’s: “when should I?” – because when you see the real numbers, waiting may not be the savings strategy you thought it was. And that’s the best conversation you can have with your trusted agent right now.

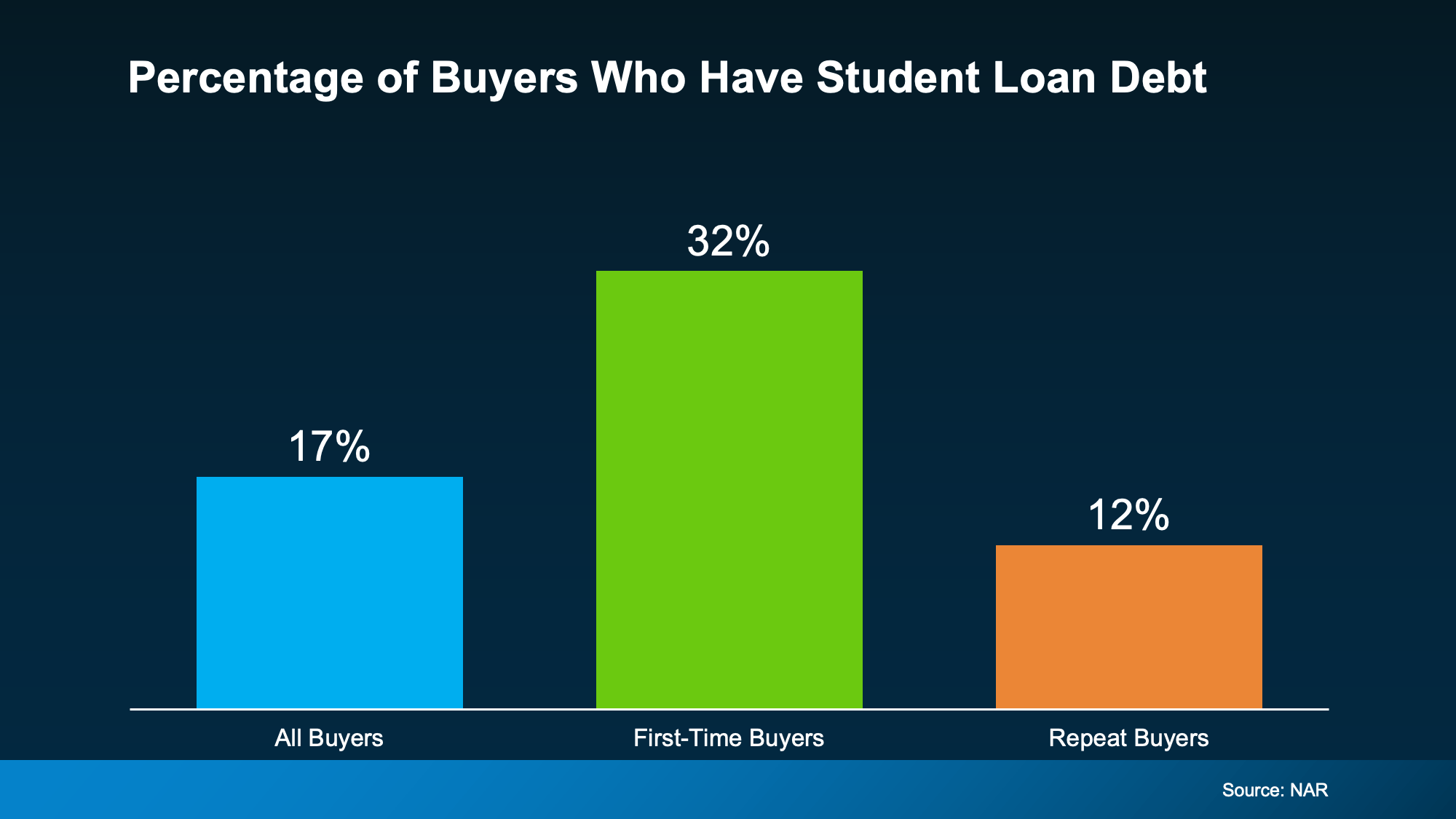

While everyone’s situation is unique, your goal may be more doable than you realize. Plenty of people with student loans have been able to qualify for and buy a home. Let that reassure you that it is still possible, even as a first-time buyer. And just in case it’s helpful to know, the median student loan debt was $30,000. As an article from Chase says:

While everyone’s situation is unique, your goal may be more doable than you realize. Plenty of people with student loans have been able to qualify for and buy a home. Let that reassure you that it is still possible, even as a first-time buyer. And just in case it’s helpful to know, the median student loan debt was $30,000. As an article from Chase says:

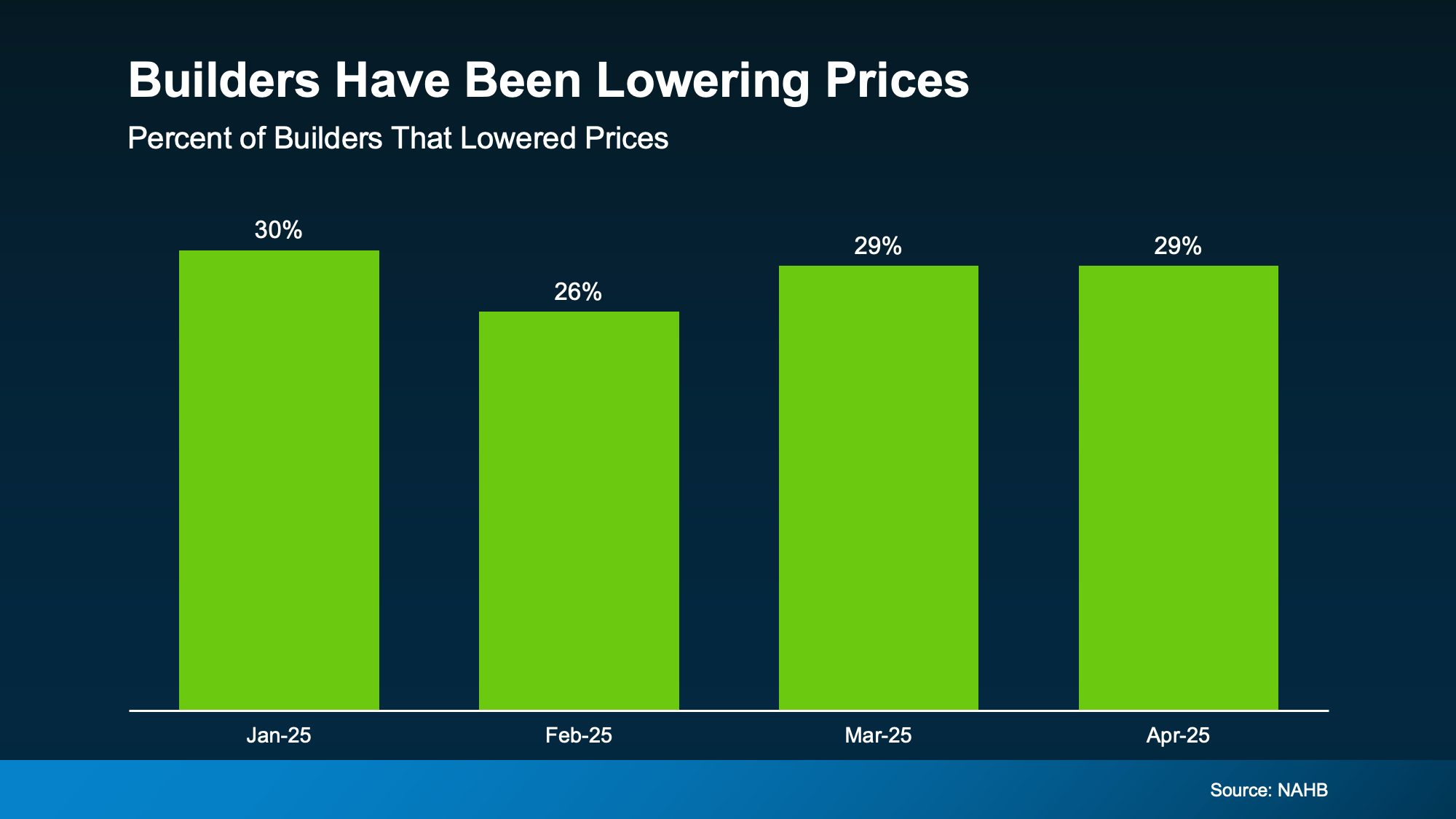

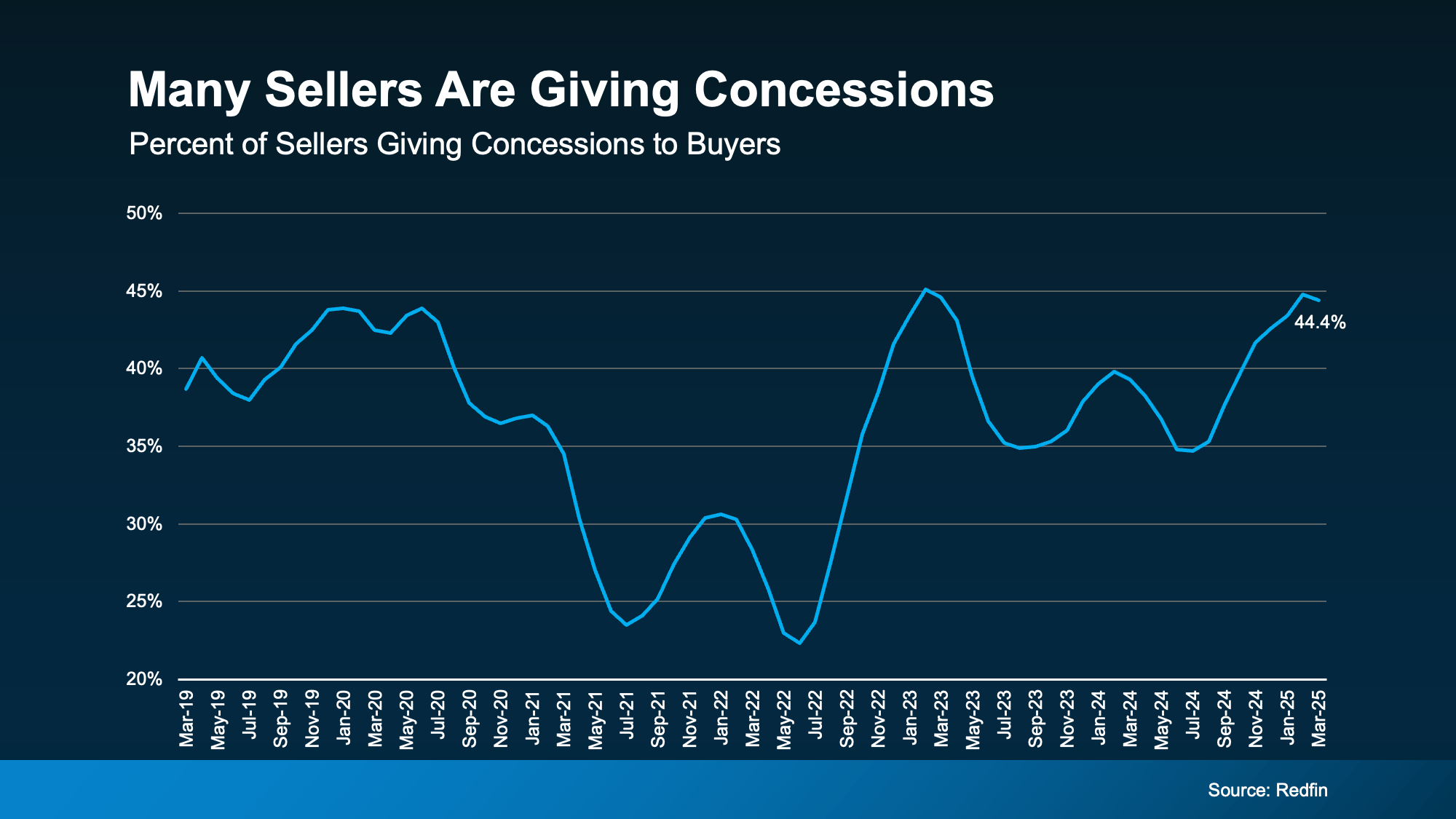

Around 30% of builders lowered prices in each of the first four months of the year. While that also means most builders aren’t lowering prices, it also shows some are willing to negotiate with buyers to get a deal done.

Around 30% of builders lowered prices in each of the first four months of the year. While that also means most builders aren’t lowering prices, it also shows some are willing to negotiate with buyers to get a deal done. And, if you look back at pre-pandemic years on this graph, you’ll see 44% is pretty much returning to normal. After years of sellers having all the power, the market is balancing again, which can work in your favor as a buyer.

And, if you look back at pre-pandemic years on this graph, you’ll see 44% is pretty much returning to normal. After years of sellers having all the power, the market is balancing again, which can work in your favor as a buyer.

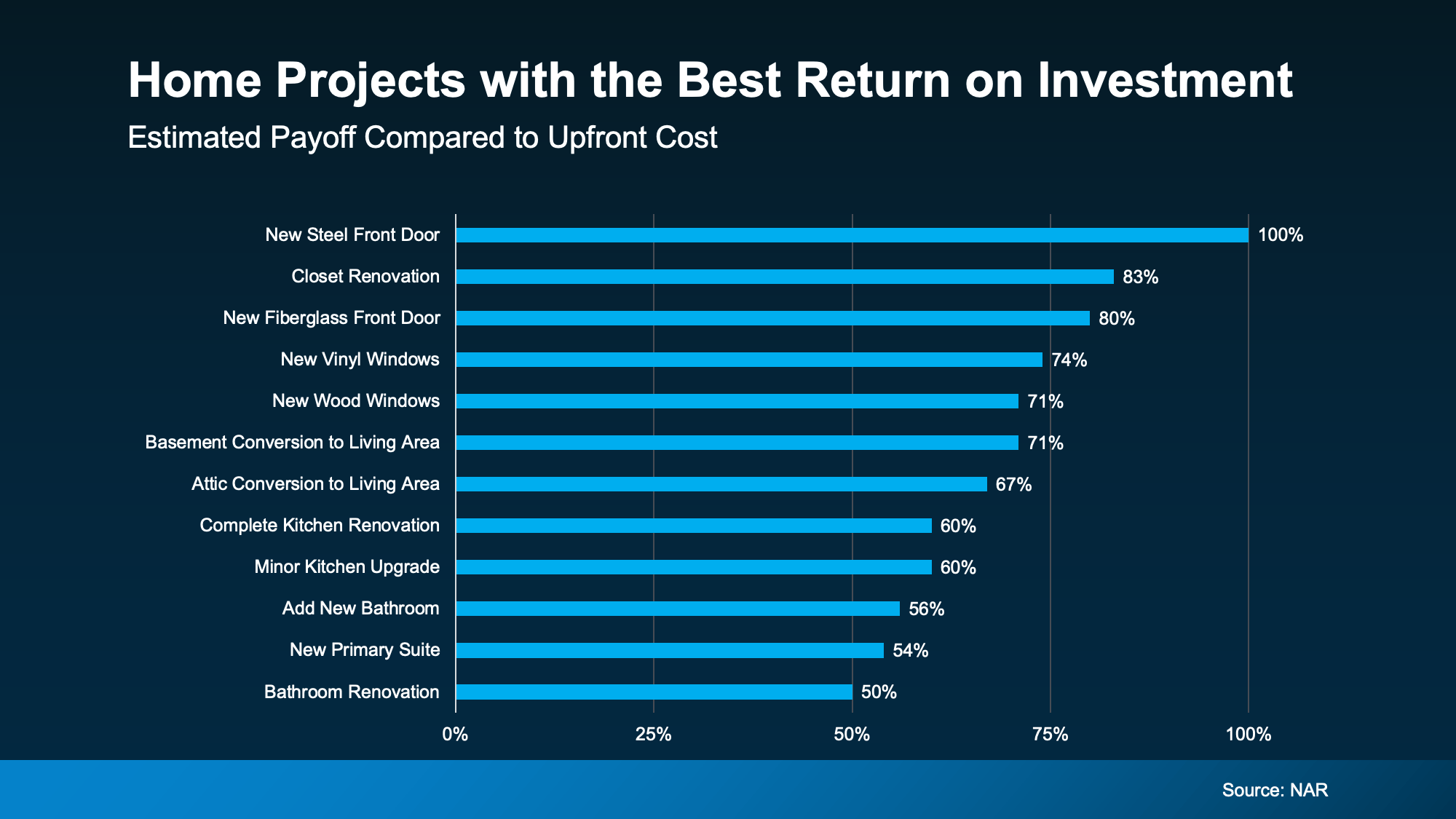

If an update you're already thinking about overlaps with those high-ROI upgrades, great. Odds are it'll improve your quality of life now and your home’s value later.

If an update you're already thinking about overlaps with those high-ROI upgrades, great. Odds are it'll improve your quality of life now and your home’s value later.

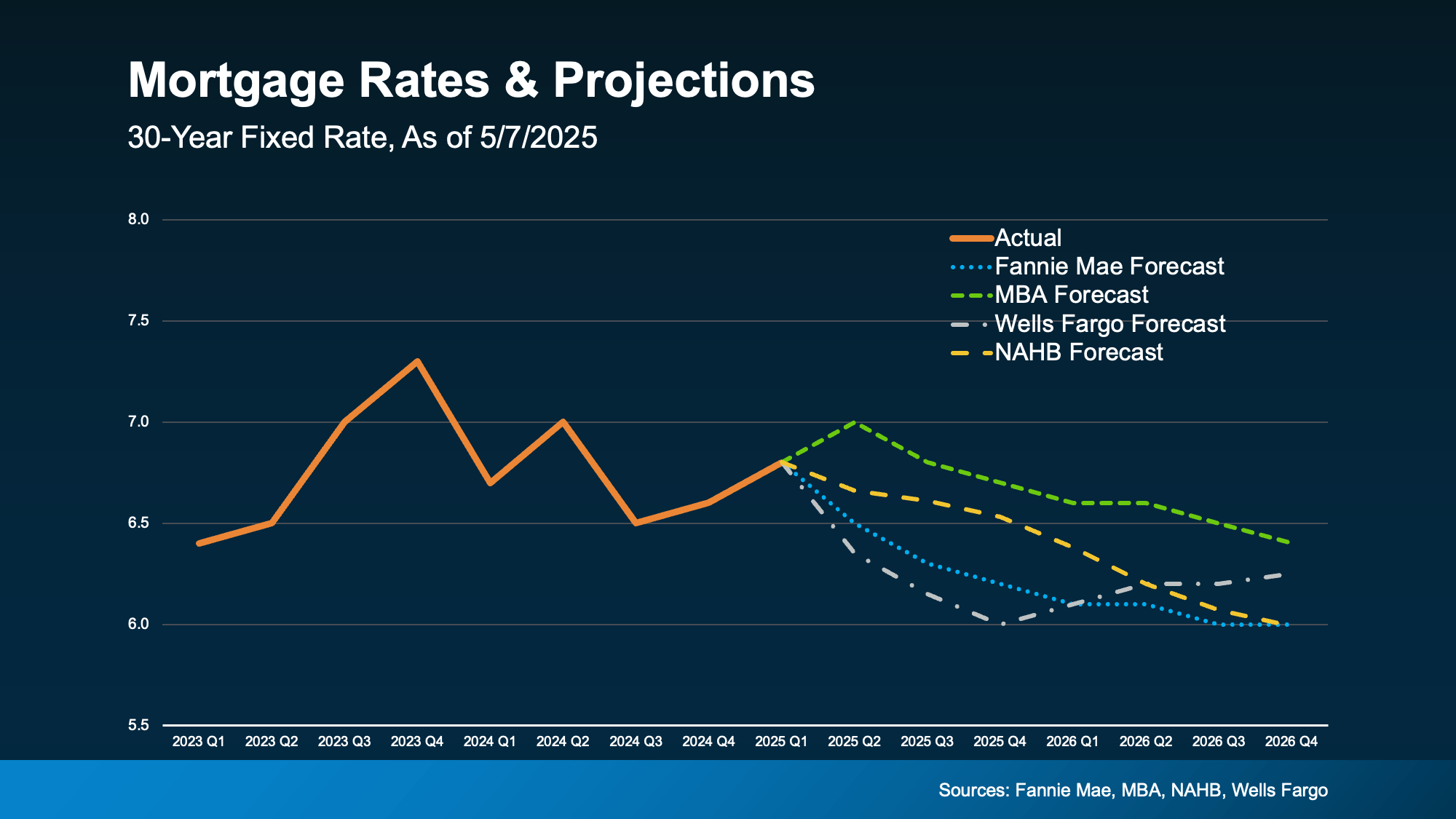

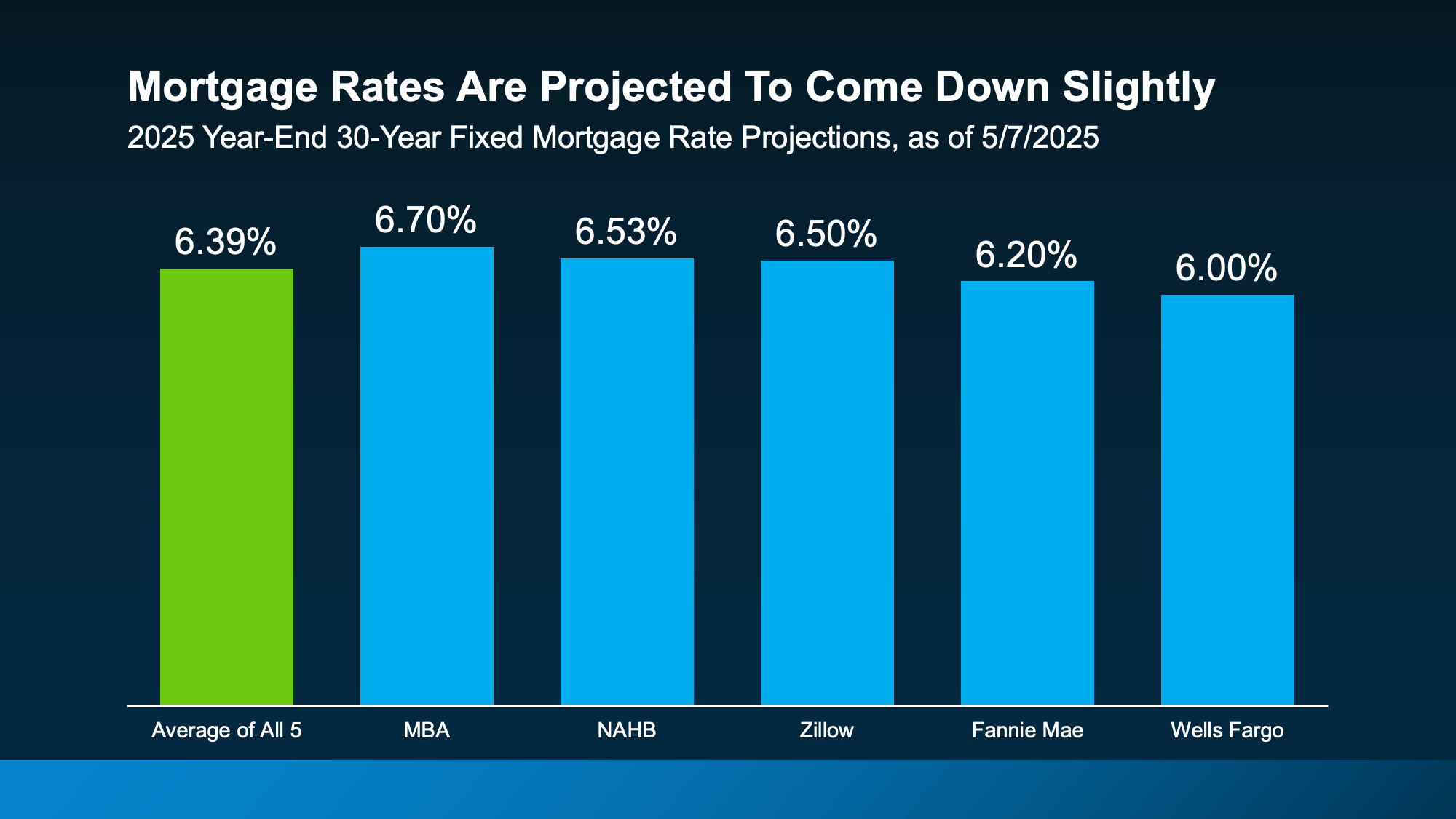

Even this slight decrease is a welcome change. A seemingly small decline can still help bring down your future mortgage payment and give you a bit more breathing room in your budget.

Even this slight decrease is a welcome change. A seemingly small decline can still help bring down your future mortgage payment and give you a bit more breathing room in your budget. That means you could finally get a little bit of relief from rapidly rising home prices. When you combine the forecast for healthier price growth with projections for slightly lower mortgage rates, that could mean more buying power in the months ahead.

That means you could finally get a little bit of relief from rapidly rising home prices. When you combine the forecast for healthier price growth with projections for slightly lower mortgage rates, that could mean more buying power in the months ahead.

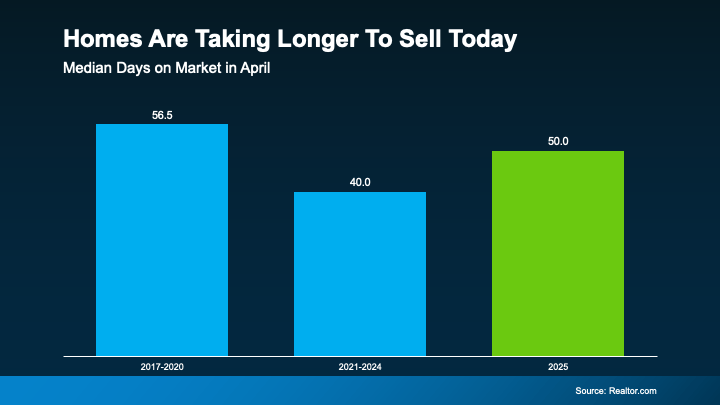

But before you get hung up on the ten-day difference compared to the past few years, Realtor.com will help put this into perspective:

But before you get hung up on the ten-day difference compared to the past few years, Realtor.com will help put this into perspective:

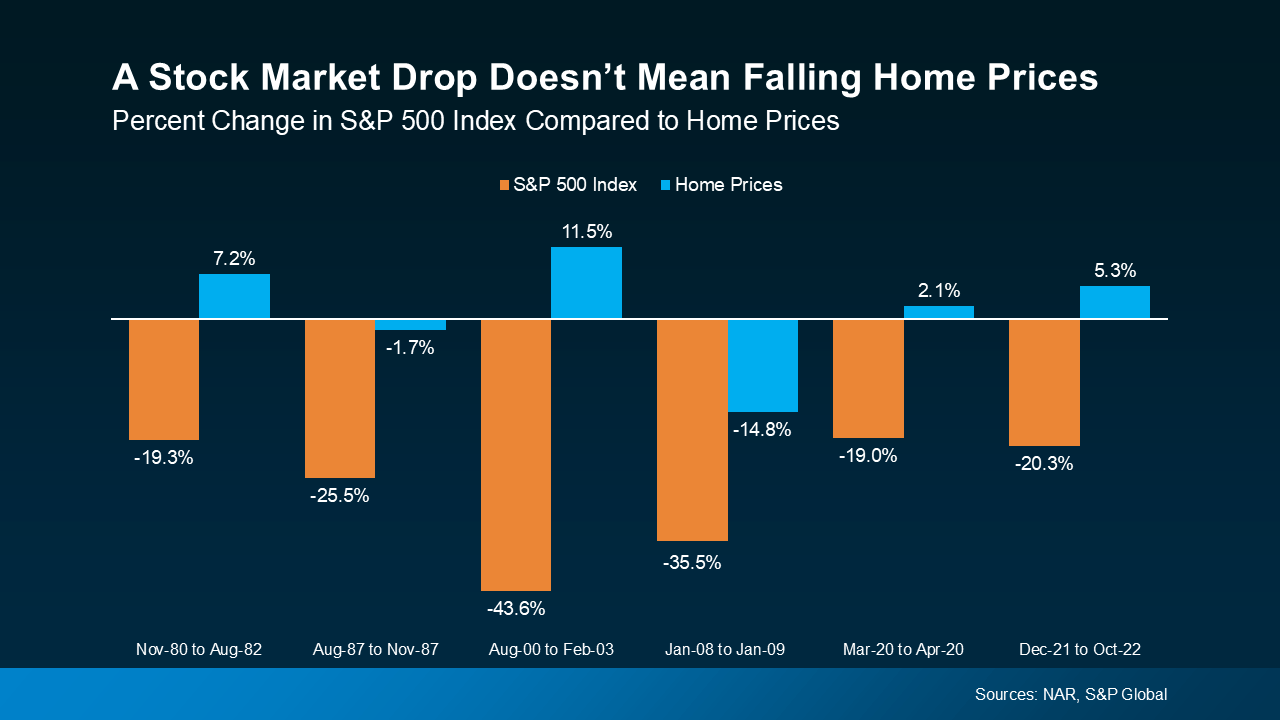

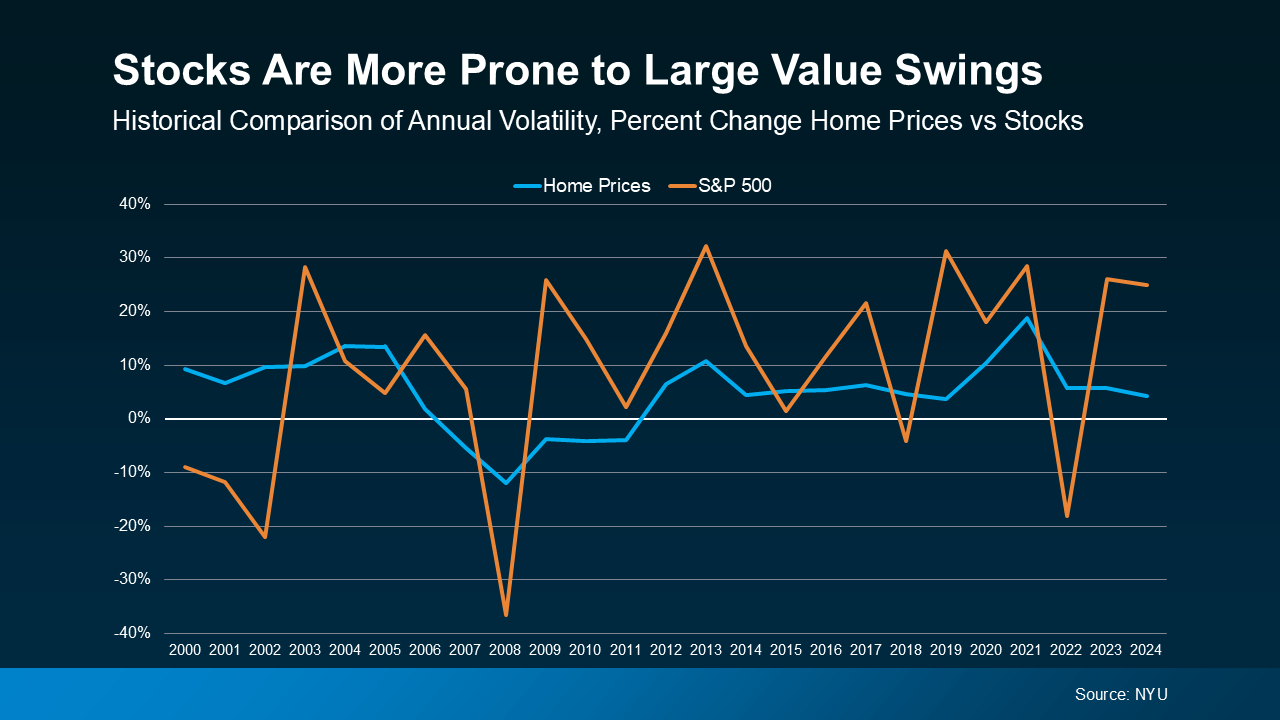

Even when the stock market falls more substantially, home prices don’t always come down with it.

Even when the stock market falls more substantially, home prices don’t always come down with it.  Basically, stock values jump around a lot more than home prices do. You can be way up one day and way down the next. Real estate, on the other hand, isn’t usually something that experiences such dramatic swings.

Basically, stock values jump around a lot more than home prices do. You can be way up one day and way down the next. Real estate, on the other hand, isn’t usually something that experiences such dramatic swings.